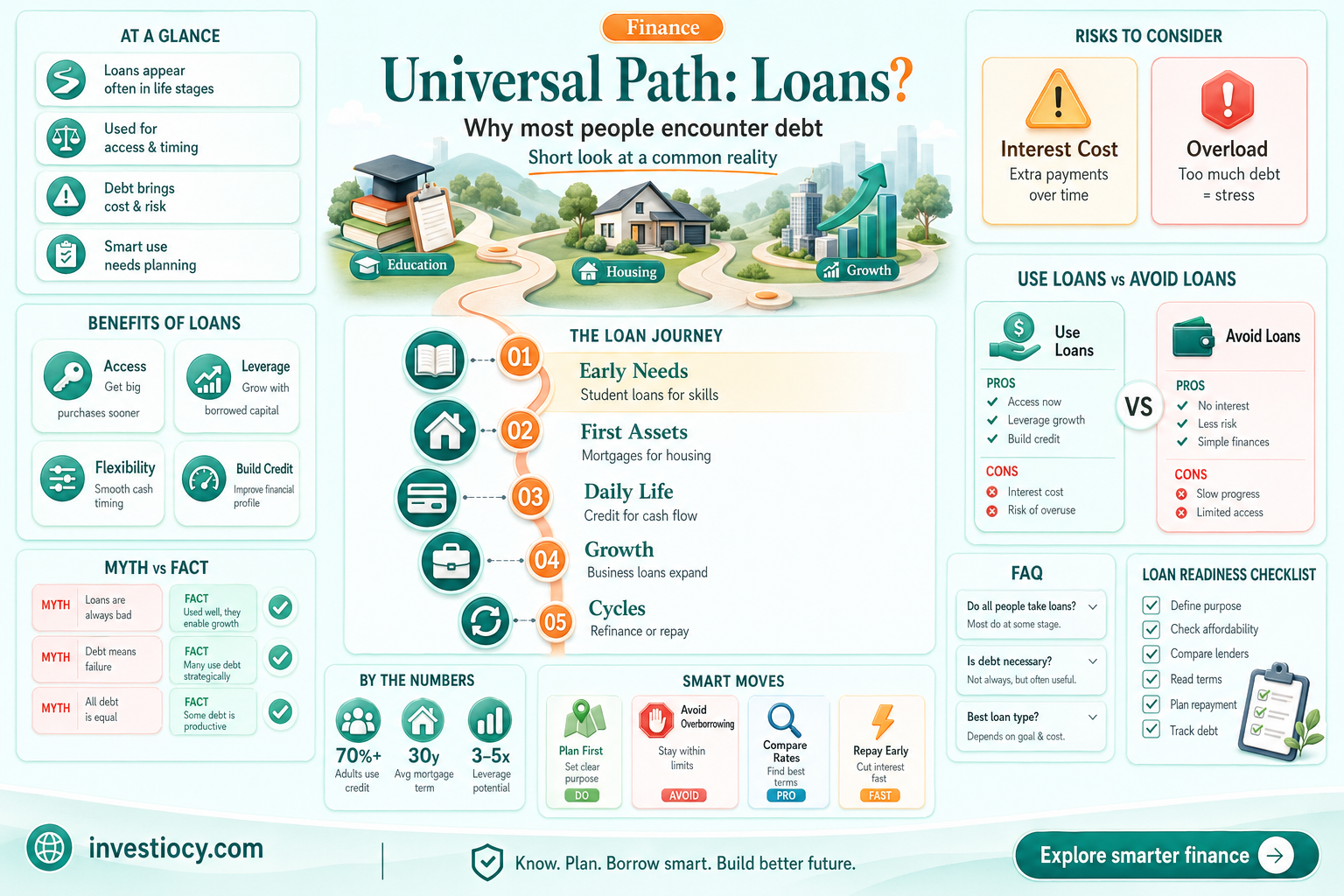

The question Does everyone go on one loan in the journey? seems to be exploring the concept of financial assistance in the form of loans and whether it is a universal experience. To address this, it's important to consider the various contexts in which loans might be relevant, such as education, home ownership, or personal finance. Loans can be a significant part of many people's financial journeys, providing necessary support to achieve goals that might otherwise be out of reach. However, the necessity and prevalence of loans can vary greatly depending on individual circumstances, cultural norms, and economic conditions. Therefore, while loans are a common tool used by many, they are not a one-size-fits-all solution, and not everyone may need or choose to use them in their financial journey.

What You'll Learn

- Loan Options: Exploring various loan types available for different stages of life and financial needs

- Eligibility Criteria: Understanding the requirements and qualifications needed to secure loans from financial institutions

- Interest Rates: Comparing fixed and variable interest rates, and their impact on loan repayments and financial planning

- Repayment Strategies: Developing effective plans to manage and repay loans, including budgeting and refinancing options

- Financial Literacy: Educating individuals on the importance of credit scores, debt management, and responsible borrowing practices

![]()

Loan Options: Exploring various loan types available for different stages of life and financial needs

Navigating the complex landscape of loan options can be daunting, especially when considering the various stages of life and the unique financial needs that accompany each phase. From the early days of student loans to the later stages of life where one might consider a reverse mortgage, understanding the different types of loans available is crucial for making informed financial decisions.

One of the most common loan types is the personal loan, which can be used for a variety of purposes, such as consolidating debt, financing a large purchase, or covering unexpected expenses. Personal loans are typically unsecured, meaning they don't require collateral, and are repaid in fixed monthly installments. Another popular option is the home equity loan, which allows homeowners to borrow against the equity in their property. This type of loan can be advantageous for those looking to finance home improvements or consolidate high-interest debt.

For those in the early stages of their careers, student loans are often a necessary evil. These loans can be federal or private and are designed to help cover the cost of tuition, fees, and living expenses while attending college or university. Understanding the terms and conditions of these loans, as well as the repayment options, is essential for avoiding financial pitfalls later in life.

As individuals approach retirement, they may consider a reverse mortgage, which allows homeowners aged 62 and older to convert part of their home equity into cash. This type of loan can provide a supplemental income stream during retirement, but it's important to carefully weigh the pros and cons before making a decision.

In addition to these common loan types, there are also specialized loans tailored to specific needs, such as business loans for entrepreneurs, auto loans for vehicle purchases, and payday loans for short-term cash flow issues. Each loan type has its own set of terms, interest rates, and repayment schedules, making it essential to shop around and compare options before committing to a loan.

Ultimately, the key to successfully navigating the world of loans is to be informed and proactive. By understanding the different loan options available and carefully considering the terms and conditions, individuals can make smart financial decisions that align with their unique needs and goals.

Decoding the Myth: Do All Students Complete Their MPN Student Loans?

You may want to see also

![]()

Eligibility Criteria: Understanding the requirements and qualifications needed to secure loans from financial institutions

Securing a loan from a financial institution is not a universal experience; it hinges significantly on meeting specific eligibility criteria. These criteria are essentially a set of requirements and qualifications that lenders use to assess the creditworthiness and repayment capacity of potential borrowers. Understanding these criteria is crucial for anyone considering taking out a loan, as it can mean the difference between approval and rejection.

Eligibility criteria can vary widely depending on the type of loan, the lender, and the country. However, there are some common factors that most lenders consider. These typically include the borrower's age, income, employment status, credit history, and debt-to-income ratio. For instance, many lenders require borrowers to be at least 18 years old and to have a steady source of income. A good credit history is also often essential, as it demonstrates the borrower's ability to repay debts on time.

In addition to these basic criteria, lenders may also consider other factors such as the borrower's education level, the purpose of the loan, and the amount of collateral available. For example, a borrower seeking a student loan may need to provide proof of enrollment in an educational institution, while someone applying for a mortgage will need to demonstrate that they have a sufficient down payment.

Meeting the eligibility criteria is just the first step in the loan application process. Borrowers must also provide necessary documentation, such as proof of identity, income statements, and bank account information. Once the application is submitted, the lender will review it and make a decision based on the borrower's overall financial situation and creditworthiness.

It's important to note that eligibility criteria are not set in stone and can change over time. Economic conditions, regulatory changes, and shifts in lending practices can all impact the requirements for securing a loan. As such, potential borrowers should always check with lenders directly to get the most up-to-date information on eligibility criteria before applying for a loan.

Exploring Loan Recasting Options: A Comprehensive Lender Comparison

You may want to see also

![]()

Interest Rates: Comparing fixed and variable interest rates, and their impact on loan repayments and financial planning

Understanding the difference between fixed and variable interest rates is crucial for anyone considering taking out a loan. Fixed interest rates remain constant throughout the loan term, providing predictability and stability in repayment amounts. This can be particularly beneficial for budgeting purposes, as borrowers know exactly how much they will need to pay each month. On the other hand, variable interest rates fluctuate based on market conditions, which can lead to changes in the monthly repayment amount. While this may offer the potential for lower interest costs if rates decrease, it also carries the risk of higher repayments if rates rise.

When comparing fixed and variable interest rates, it's essential to consider the overall economic climate and personal financial goals. In a low-interest-rate environment, variable rates may be more attractive, as they could potentially decrease further. However, in a rising interest rate environment, fixed rates provide a safeguard against increasing costs. Additionally, fixed rates are often preferred by those who value consistency and are less comfortable with the uncertainty of variable rates.

The impact of interest rates on loan repayments can be significant. For example, a 1% increase in interest rates on a $200,000 mortgage could result in an additional $2,000 in annual repayments. This underscores the importance of carefully considering the type of interest rate when taking out a loan, as it can have a substantial effect on long-term financial planning. Borrowers should also be aware of any caps or floors on variable interest rates, which can limit the extent of rate changes.

Financial planning is another critical aspect to consider when choosing between fixed and variable interest rates. Fixed rates can be more suitable for those with a fixed income or those who are risk-averse, as they provide a clear picture of future expenses. Variable rates, on the other hand, may be more appropriate for individuals with a higher risk tolerance or those who expect their income to increase over time, potentially offsetting higher interest costs.

In conclusion, the choice between fixed and variable interest rates depends on a variety of factors, including economic conditions, personal financial goals, and risk tolerance. By carefully weighing these considerations, borrowers can make an informed decision that aligns with their long-term financial objectives.

Exploring the Role of Financial Intermediaries in Every Loan

You may want to see also

![]()

Repayment Strategies: Developing effective plans to manage and repay loans, including budgeting and refinancing options

Creating an effective repayment strategy is crucial for managing and repaying loans. A well-structured plan can help borrowers save money on interest, avoid late fees, and improve their credit scores. The first step in developing a repayment strategy is to assess the current financial situation. This involves listing all debts, including the loan in question, along with their interest rates, monthly payments, and outstanding balances. Understanding the total debt burden and the cost of each loan is essential for prioritizing repayment efforts.

Once the financial assessment is complete, borrowers can explore various repayment strategies. One popular approach is the snowball method, which involves paying off the smallest debt first while making minimum payments on the others. As each debt is paid off, the borrower can apply the freed-up funds to the next smallest debt, creating a snowball effect that accelerates repayment. Another strategy is the avalanche method, which targets debts with the highest interest rates first. This approach can save more money on interest over time but may require more discipline and patience.

Budgeting plays a critical role in successful loan repayment. By creating a detailed budget that accounts for all income and expenses, borrowers can identify areas where they can cut costs and allocate more funds toward debt repayment. This may involve reducing discretionary spending, such as dining out or entertainment, and focusing on essential expenses like housing, food, and utilities. Additionally, borrowers can consider increasing their income through side jobs, freelance work, or selling unwanted items to boost their repayment efforts.

Refinancing is another option that can help borrowers manage their loans more effectively. By refinancing a loan, borrowers can potentially secure a lower interest rate or extend the repayment term, which can reduce their monthly payments and make the debt more manageable. However, refinancing may not always be the best choice, as it can result in additional fees and may extend the overall repayment period. Borrowers should carefully weigh the pros and cons of refinancing before making a decision.

In conclusion, developing an effective repayment strategy requires a thorough understanding of one's financial situation, careful consideration of various repayment methods, and a commitment to budgeting and potentially refinancing. By taking a proactive approach to loan repayment, borrowers can save money, reduce stress, and achieve financial freedom more quickly.

![]()

Financial Literacy: Educating individuals on the importance of credit scores, debt management, and responsible borrowing practices

Understanding the intricacies of financial literacy is crucial for navigating the complex world of personal finance. One key aspect is comprehending the significance of credit scores. A credit score is a numerical representation of an individual's creditworthiness, which lenders use to determine the likelihood of repayment. A higher credit score can lead to better loan terms, lower interest rates, and increased borrowing capacity. Conversely, a lower credit score may result in higher interest rates, stricter loan conditions, or even loan denial.

Effective debt management is another cornerstone of financial literacy. This involves creating a budget, prioritizing debt repayment, and understanding the different types of debt, such as secured and unsecured loans. Secured debts, like mortgages or car loans, are backed by collateral, while unsecured debts, like credit card balances or personal loans, are not. Managing debt responsibly requires making timely payments, avoiding excessive borrowing, and seeking assistance when needed, such as through credit counseling or debt consolidation services.

Responsible borrowing practices are essential to maintaining financial health. This includes understanding the terms and conditions of loans, comparing interest rates and fees, and borrowing only what is necessary. It's also important to be aware of predatory lending practices, such as payday loans or title loans, which often come with exorbitant interest rates and fees. By educating oneself on these topics, individuals can make informed decisions about borrowing and avoid falling into debt traps.

Financial literacy education can start at a young age, with parents teaching children about saving, budgeting, and the value of money. Schools can also play a role by incorporating financial literacy into their curricula. For adults, there are numerous resources available, including online courses, workshops, and financial advisors. By investing time and effort into learning about personal finance, individuals can empower themselves to make better financial decisions and achieve long-term financial stability.

In conclusion, financial literacy is a critical skill for managing personal finances effectively. By understanding credit scores, debt management, and responsible borrowing practices, individuals can navigate the financial landscape with confidence and avoid common pitfalls. Education and awareness are key to improving financial literacy, and it's never too early or too late to start learning about these important topics.

Frequently asked questions

This phrase seems to be a misspelling or misinterpretation of the common saying "does everyone go alone in the journey." It suggests that at some point in life, everyone may find themselves traveling or facing challenges alone.

While it's not a universal truth that everyone will experience loneliness, it is common for individuals to face periods of solitude or isolation. These experiences can vary greatly in duration and intensity, and people cope with them in different ways.

Preparing for or coping with loneliness during a journey can involve several strategies:

- Building a support network of friends and family before embarking on the journey.

- Engaging in activities that bring joy and fulfillment, such as hobbies or volunteering.

- Practicing mindfulness and self-reflection to better understand and manage emotions.

- Seeking out opportunities to connect with others, such as joining local groups or attending events.

- Maintaining regular communication with loved ones through letters, calls, or video chats.