Forebearance is a temporary suspension or reduction of loan payments, often granted by lenders to borrowers facing financial hardship. It's designed to provide short-term relief without negatively impacting the borrower's credit score. However, it's important to understand that while forbearance can help in the short term, it may have implications for your loan in the long run. Interest may continue to accrue during the forbearance period, potentially increasing the total amount you owe. Additionally, lenders may view forbearance as a sign of financial instability, which could affect future lending decisions. It's crucial to communicate with your lender and understand the terms of any forbearance agreement to make informed decisions about your financial situation.

Explore related products

What You'll Learn

- Understanding Foreclosure: Explains the legal process and its impact on homeowners and their credit scores

- Immediate Financial Effects: Discusses how foreclosure affects personal finances, including bank accounts and other assets

- Long-term Credit Implications: Details the lasting impact on credit reports and scores, and how it may affect future borrowing

- Options to Avoid Foreclosure: Lists potential strategies and resources available to homeowners to prevent foreclosure

- Rebuilding After Foreclosure: Offers guidance on recovering financially and rebuilding credit after experiencing foreclosure

![]()

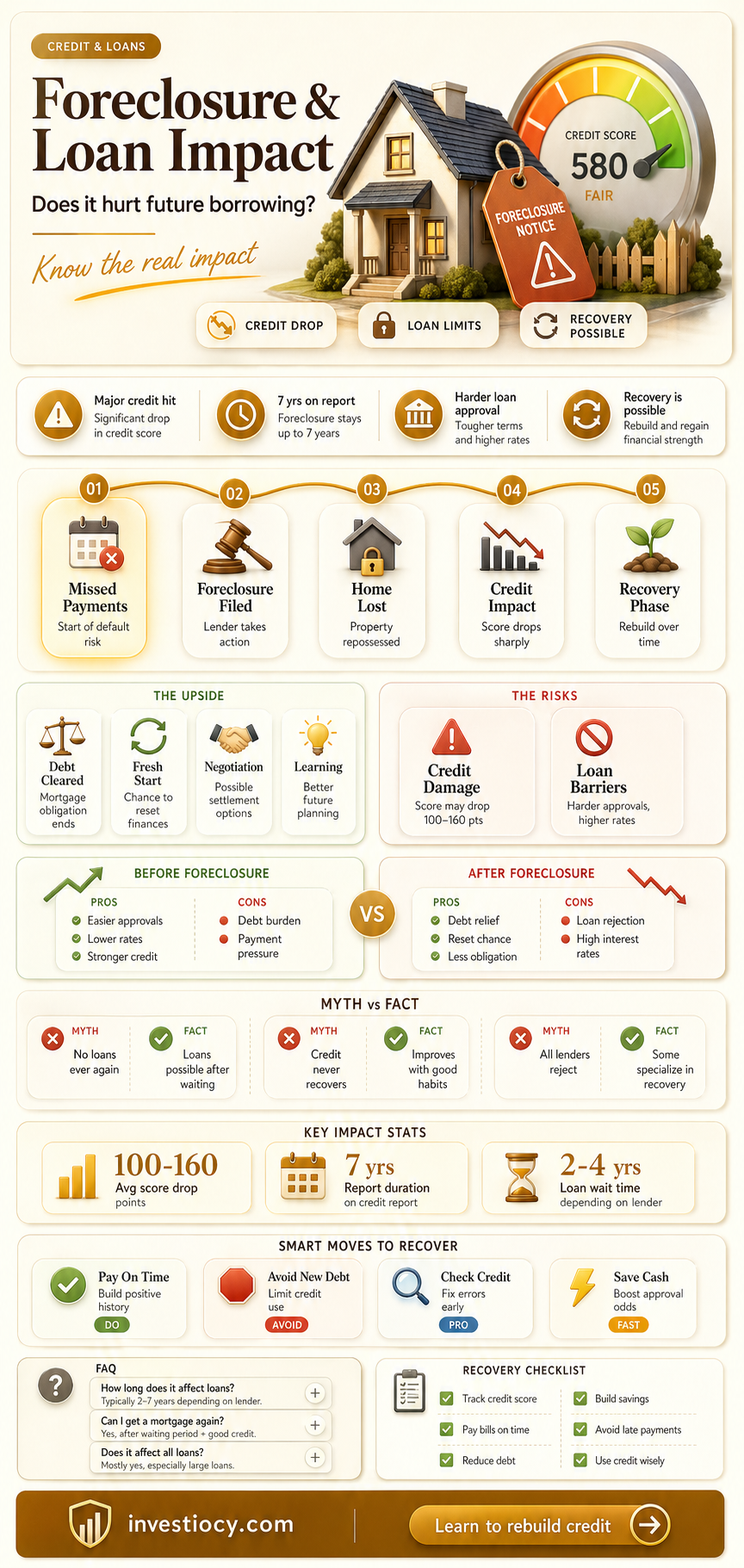

Understanding Foreclosure: Explains the legal process and its impact on homeowners and their credit scores

Foreclosure is a legal process that occurs when a homeowner fails to make mortgage payments as agreed upon in the loan contract. This process can have severe consequences for the homeowner, including the loss of their property and a significant negative impact on their credit score. It's essential to understand the steps involved in foreclosure and the potential ramifications to take proactive measures to avoid it.

The foreclosure process typically begins when the lender sends a Notice of Default to the homeowner, indicating that they have missed a certain number of payments. If the homeowner fails to respond or make the required payments, the lender may then file a Notice of Sale with the county recorder's office. This notice informs the homeowner and the public that the property will be sold at auction to the highest bidder. The sale date is usually set for a few weeks after the notice is filed, giving the homeowner a final opportunity to reinstate the loan or sell the property themselves to avoid foreclosure.

If the property is sold at auction, the new owner will typically evict the former homeowner, who may then face difficulties finding new housing due to their damaged credit score. Foreclosure can also lead to deficiency judgments, where the lender sues the homeowner for the difference between the sale price of the property and the outstanding loan balance. This can result in further financial hardship and legal complications for the homeowner.

To avoid foreclosure, homeowners should communicate with their lender as soon as they encounter financial difficulties. Lenders may be willing to work out a payment plan or modify the loan terms to help the homeowner get back on track. Additionally, homeowners should be cautious of foreclosure scams, where fraudulent companies promise to help save their home but instead take advantage of their vulnerable situation.

In conclusion, understanding the foreclosure process and its potential consequences is crucial for homeowners facing financial difficulties. By taking proactive steps to communicate with their lender and avoid scams, homeowners can minimize the risk of foreclosure and protect their credit score and financial well-being.

Explore related products

![]()

Immediate Financial Effects: Discusses how foreclosure affects personal finances, including bank accounts and other assets

Foreclosure can have a profound and immediate impact on an individual's personal finances. One of the first areas to be affected is often the bank accounts. When a foreclosure occurs, the lender may freeze the accounts to prevent the withdrawal of funds, ensuring that any available assets are used to offset the outstanding debt. This can leave the individual without access to their money, making it difficult to pay for essential expenses such as food, housing, and utilities.

In addition to bank accounts, other assets may also be at risk. For example, if the individual has investments, such as stocks or bonds, these may be liquidated to help cover the debt. Retirement accounts, such as 401(k)s or IRAs, may also be targeted, potentially resulting in significant tax penalties and reducing the individual's ability to save for the future. Even personal property, such as vehicles or jewelry, may be seized and sold to help satisfy the debt.

The immediate financial effects of foreclosure can also extend to credit scores. A foreclosure will likely result in a significant drop in credit score, making it more difficult to obtain credit in the future. This can have long-term consequences, affecting the individual's ability to purchase a new home, obtain a car loan, or even secure a credit card.

Furthermore, foreclosure can lead to additional expenses, such as legal fees and court costs. These costs can quickly add up, further depleting the individual's financial resources. In some cases, the individual may also be responsible for any deficiency balance, which is the difference between the sale price of the property and the outstanding debt. This can result in a significant financial burden that may take years to overcome.

In conclusion, the immediate financial effects of foreclosure can be severe and far-reaching, impacting not only bank accounts and other assets but also credit scores and future financial opportunities. It is essential for individuals facing foreclosure to seek professional advice and explore all available options to mitigate these effects and protect their financial well-being.

Explore related products

$22.8 $26.99

$24.99 $24.99

![]()

Long-term Credit Implications: Details the lasting impact on credit reports and scores, and how it may affect future borrowing

Forebearance can have a lasting impact on your credit reports and scores, potentially affecting your ability to borrow in the future. While it may provide temporary relief from loan payments, it's essential to understand the long-term credit implications.

One of the primary concerns with forbearance is that it can lead to a negative credit history. When you stop making payments, even if it's due to a forbearance agreement, it can be reported to the credit bureaus as a delinquency. This can significantly lower your credit score, making it more challenging to secure loans or credit cards in the future.

Furthermore, forbearance can also impact your debt-to-income ratio. Since the interest on your loan may continue to accrue during the forbearance period, your overall debt could increase. This, in turn, can make it more difficult to qualify for new loans or credit, as lenders may view you as a higher risk.

It's also important to consider the potential impact on your credit utilization ratio. If you're not making payments during the forbearance period, your credit utilization ratio may increase, which can further lower your credit score.

To mitigate these long-term credit implications, it's crucial to work with your lender to develop a plan for resuming payments as soon as possible. You may also want to consider credit counseling or financial planning services to help you manage your debt and improve your credit health.

In conclusion, while forbearance can provide temporary relief, it's essential to understand the potential long-term credit implications. By taking proactive steps to manage your debt and credit, you can minimize the negative impact of forbearance on your future borrowing ability.

Explore related products

![]()

Options to Avoid Foreclosure: Lists potential strategies and resources available to homeowners to prevent foreclosure

Homeowners facing the threat of foreclosure have several options to explore in order to prevent the loss of their property. One potential strategy is to negotiate with the lender for a loan modification. This could involve extending the repayment term, reducing the interest rate, or temporarily suspending payments. Homeowners should gather all necessary financial documentation and contact their lender to discuss possible modifications.

Another option is to seek assistance from a housing counseling agency. These agencies provide free or low-cost counseling services to help homeowners understand their options and develop a plan to avoid foreclosure. They can also assist with negotiating with lenders and may have access to additional resources such as emergency funds or grants.

In some cases, homeowners may be able to sell their property through a short sale, where the sale price is less than the outstanding mortgage balance. This can help avoid the negative impact of a foreclosure on the homeowner's credit score. However, it's important to note that a short sale may still have tax implications and could result in a deficiency judgment.

Refinancing the mortgage is another potential strategy to avoid foreclosure. By refinancing, homeowners may be able to secure a lower interest rate or extend the repayment term, making their monthly payments more manageable. However, refinancing can be challenging for homeowners who are already struggling with payments, as it often requires a good credit score and sufficient equity in the property.

Lastly, homeowners should be aware of scams that target those facing foreclosure. These scams often promise to help homeowners avoid foreclosure for a fee, but may actually make the situation worse. Homeowners should always verify the legitimacy of any organization offering assistance and should never pay for services upfront.

Explore related products

![]()

Rebuilding After Foreclosure: Offers guidance on recovering financially and rebuilding credit after experiencing foreclosure

Foreclosure can be a devastating financial event, but it's not the end of the road. Rebuilding your finances and credit after foreclosure requires a strategic approach and patience. Here's a step-by-step guide to help you recover:

- Assess Your Financial Situation: Start by taking stock of your current financial standing. Pull your credit reports from all three major bureaus (Equifax, Experian, and TransUnion) to understand where you stand credit-wise. Review your income, expenses, and any outstanding debts. This will help you identify areas that need improvement and create a realistic budget.

- Create a Budget and Stick to It: Develop a strict budget that prioritizes essential expenses like housing, food, and utilities. Cut back on non-essential spending and allocate extra funds towards paying off debts. Consider using the 50/30/20 rule: 50% of your income for necessities, 30% for discretionary spending, and 20% for savings and debt repayment.

- Pay Off Debts and Rebuild Credit: Focus on paying off any outstanding debts, especially those that went into collections during the foreclosure process. Consider consolidating debts into a single loan with a lower interest rate. As you pay off debts, your credit score will gradually improve. You can also consider applying for a secured credit card to start rebuilding credit.

- Save for a Down Payment: If you're planning to buy a home again in the future, start saving for a down payment. This will not only help you qualify for a mortgage but also demonstrate to lenders that you're financially responsible. Aim to save at least 20% of the home's purchase price to avoid paying private mortgage insurance (PMI).

- Monitor Your Credit Score: Keep a close eye on your credit score as you work on rebuilding your finances. You can use free credit monitoring services or check your score regularly through your bank or credit card issuer. This will help you track your progress and identify any potential issues that need to be addressed.

- Seek Professional Help if Needed: If you're struggling to manage your finances or create a budget, consider seeking help from a financial advisor or credit counselor. They can provide personalized guidance and support to help you get back on track.

Remember, rebuilding after foreclosure takes time and effort, but it's possible. By following these steps and staying committed to your financial goals, you can recover from foreclosure and achieve financial stability once again.

Frequently asked questions

Forbearance is a temporary agreement between you and your lender to pause or reduce your loan payments for a specific period. It does not hurt your loan in the sense that it's a structured plan to help you manage financial difficulties. However, interest may continue to accrue during the forbearance period, which could increase the total amount you owe.

Forbearance itself does not necessarily hurt your credit score, as it's a formal arrangement with your lender. However, if you miss payments or default on the loan after the forbearance period ends, this could negatively affect your credit score.

While forbearance can provide immediate relief, it's important to understand the long-term implications. The accrued interest during the forbearance period will need to be paid, which could extend the life of your loan or increase your monthly payments. Additionally, if you're not careful about managing your finances during this time, you might find yourself in a similar situation once the forbearance ends.