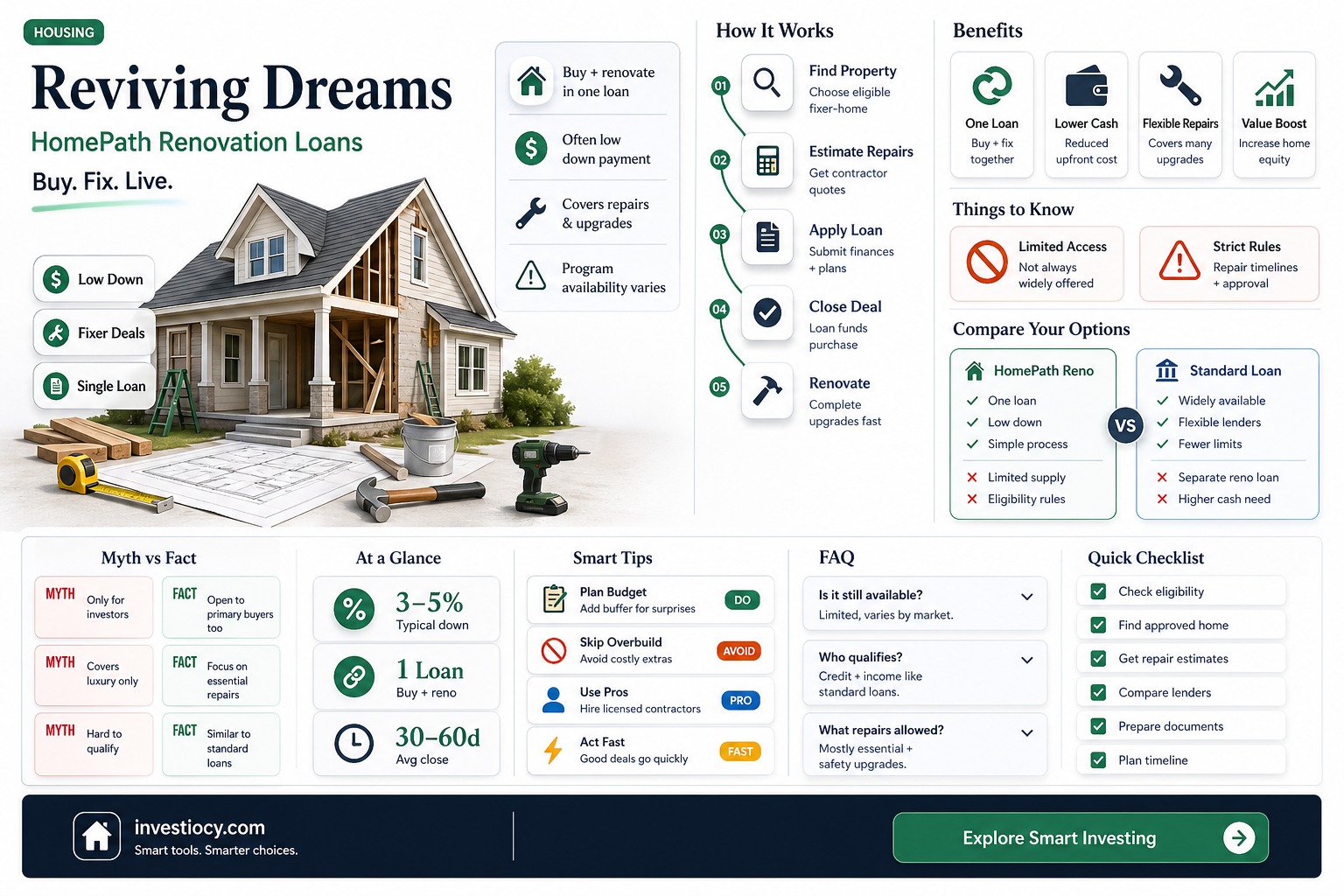

The HomePath Renovation Loan Program, previously offered by Fannie Mae, was a popular financing option for homebuyers looking to purchase and renovate foreclosed properties. However, as of my last update in June 2024, this specific program has been discontinued. Fannie Mae introduced the HomePath Ready Buyer program as a replacement, which focuses on providing financing for the purchase of foreclosed properties without the renovation component. For those interested in renovating a property, other loan options such as the FHA 203(k) loan or various private lender renovation loans may still be available. It's essential to check with current lenders and housing agencies for the most up-to-date information on renovation loan programs.

Explore related products

What You'll Learn

- Current Status: Investigate whether the HomePath Renovation Loan Program is still active as of the knowledge cutoff date

- Alternatives: Explore other loan programs or financial options available for home renovations if HomePath no longer exists

- Historical Context: Provide a brief overview of the HomePath Renovation Loan Program's inception, purpose, and impact on the housing market

- Eligibility Criteria: If the program still exists, outline the eligibility requirements for applicants, such as credit score, income limits, and property types

- Application Process: Describe the steps involved in applying for the HomePath Renovation Loan, including necessary documentation and approval timelines

![]()

Current Status: Investigate whether the HomePath Renovation Loan Program is still active as of the knowledge cutoff date

As of the knowledge cutoff date in June 2024, the HomePath Renovation Loan Program is no longer active. This program, which was designed to help homebuyers finance renovations, was discontinued by Fannie Mae in 2020. The program allowed borrowers to finance up to 50% of the renovation costs, which would be added to the base mortgage amount. However, due to various factors, including changes in the housing market and lending regulations, Fannie Mae decided to end the program.

Despite its discontinuation, the HomePath Renovation Loan Program remains a topic of interest for many potential homebuyers and real estate professionals. This is likely due to the ongoing demand for renovation financing options, as well as the program's previous popularity. However, it is important to note that the program is no longer available, and borrowers should explore alternative financing options for their renovation projects.

One alternative to the HomePath Renovation Loan Program is the FHA 203(k) loan, which is a government-backed mortgage that allows borrowers to finance both the purchase price and renovation costs of a property. Another option is a home equity loan or line of credit, which can be used to fund renovation projects. Additionally, some lenders offer renovation loans that are not government-backed, but may have more flexible terms and requirements.

In conclusion, while the HomePath Renovation Loan Program was a valuable financing option for many borrowers, it is no longer active as of June 2024. Borrowers interested in financing renovation projects should explore alternative options, such as the FHA 203(k) loan, home equity loans, or other renovation loans offered by private lenders.

Explore related products

![Homeowner's Renovation Tips & Log Book: From Planning to Completion [Cover Photo-Kitchen]](https://m.media-amazon.com/images/I/513QWTxjDEL._AC_UY218_.jpg)

![]()

Alternatives: Explore other loan programs or financial options available for home renovations if HomePath no longer exists

If you're looking to renovate your home and were considering the HomePath Renovation Loan Program, you may need to explore alternative financing options. This program, which was popular among homebuyers looking to purchase and renovate foreclosed properties, is no longer available. However, there are several other loan programs and financial options that can help you achieve your home renovation goals.

One alternative to consider is the FHA 203(k) Rehabilitation Loan. This program allows you to finance both the purchase and renovation of a home with a single loan. It's particularly useful for buying fixer-upper properties or for making significant improvements to your current home. Another option is the Fannie Mae HomeStyle Renovation Loan, which also combines the purchase and renovation costs into one loan. This program offers flexible terms and can be used for a variety of renovation projects.

For those who already own their home and are looking to refinance and renovate, a cash-out refinance could be a viable option. This type of refinance allows you to take out a new mortgage for more than the current value of your home, using the excess funds for renovations. Keep in mind that this option may require you to have a certain amount of equity in your home and may result in a higher monthly mortgage payment.

Personal loans or home equity loans are other alternatives to consider. Personal loans are unsecured loans that can be used for any purpose, including home renovations. They typically have fixed interest rates and repayment terms, making them a predictable financing option. Home equity loans, on the other hand, are secured by the equity in your home and can offer lower interest rates and longer repayment terms. However, they do put your home at risk if you fail to repay the loan.

Before choosing any of these alternatives, it's important to carefully consider your financial situation and renovation goals. Research each option thoroughly, compare interest rates and terms, and consult with a financial advisor or lender to determine the best choice for your specific needs. With the right financing in place, you can turn your home renovation dreams into reality.

Explore related products

![]()

Historical Context: Provide a brief overview of the HomePath Renovation Loan Program's inception, purpose, and impact on the housing market

The HomePath Renovation Loan Program was introduced by Fannie Mae in 2009 as a response to the housing crisis that left many homes in disrepair and communities struggling. The program aimed to provide financing for the renovation of foreclosed properties, making them more attractive to potential buyers and helping to stabilize neighborhoods. By offering a unique loan structure that combined the purchase and renovation costs into a single mortgage, HomePath made it easier for buyers to invest in fixer-uppers without the need for separate loans or out-of-pocket expenses.

The impact of the HomePath Renovation Loan Program on the housing market was significant, particularly in the early years following its inception. It helped to increase the sale of foreclosed properties, which in turn reduced the inventory of distressed homes and contributed to the overall recovery of the housing market. The program also spurred economic growth by creating jobs in the construction and renovation industries. Additionally, it provided an opportunity for first-time homebuyers and investors to enter the market at a lower cost, promoting homeownership and community development.

Over time, the HomePath Renovation Loan Program evolved to meet the changing needs of the housing market. In 2012, Fannie Mae expanded the program to include properties that were not foreclosed but still required significant renovation. This change allowed for a broader range of properties to be eligible for the loan, further increasing its appeal to buyers and investors. The program continued to grow in popularity, with thousands of loans being issued each year, until its eventual discontinuation in 2018.

Despite its success, the HomePath Renovation Loan Program faced criticism from some quarters. Opponents argued that the program was too risky, as it allowed buyers to take on significant debt without sufficient equity in the property. There were also concerns about the quality of the renovations being done, with some properties being flipped quickly for profit rather than being properly rehabilitated. These criticisms ultimately contributed to the program's demise, as Fannie Mae decided to focus on other initiatives that better aligned with its strategic goals.

In conclusion, the HomePath Renovation Loan Program played an important role in the recovery of the housing market following the 2008 financial crisis. It provided a unique financing option for the renovation of foreclosed properties, helping to stabilize neighborhoods and promote homeownership. While the program had its critics and was eventually discontinued, its impact on the housing market and the communities it served should not be overlooked.

![]()

Eligibility Criteria: If the program still exists, outline the eligibility requirements for applicants, such as credit score, income limits, and property types

To determine the eligibility criteria for the HomePath Renovation Loan Program, we must first establish whether the program is still active. As of my last update in June 2024, the HomePath program, which was previously offered by Fannie Mae, has been discontinued. However, for the sake of this exercise, let's assume the program still exists and outline the eligibility requirements that would typically apply.

In general, the HomePath Renovation Loan Program was designed to help homebuyers purchase and renovate properties that were owned by Fannie Mae. To be eligible, applicants would need to meet certain credit score requirements, which typically ranged from a minimum of 620 to 680, depending on the lender and the specific loan terms. Additionally, there would be income limits in place to ensure that the program was accessible to a wide range of borrowers, particularly those in lower- to moderate-income brackets.

The types of properties that could be purchased and renovated under the HomePath program would also be subject to specific criteria. Generally, the program would cover single-family homes, townhouses, and condominiums, but there might be restrictions on the property's condition, location, and value. For example, the property would need to be in a habitable condition, located in an area where there is a demand for housing, and priced within a certain range to ensure affordability for the borrower.

Furthermore, the renovation work would need to be substantial enough to improve the property's value and livability but not so extensive that it would exceed the program's limits. This could include repairs to the roof, plumbing, electrical systems, and other essential components, as well as cosmetic upgrades to the interior and exterior of the property.

In conclusion, while the HomePath Renovation Loan Program is no longer available, if it were still in existence, the eligibility criteria would likely include minimum credit score requirements, income limits, and restrictions on the types of properties that could be purchased and renovated. Borrowers would need to meet these criteria to qualify for the program and take advantage of its benefits.

![]()

Application Process: Describe the steps involved in applying for the HomePath Renovation Loan, including necessary documentation and approval timelines

To apply for the HomePath Renovation Loan, prospective borrowers must follow a series of steps that involve both preparation and submission of required documentation. Initially, applicants need to identify a property that qualifies for the loan, which typically includes foreclosed homes that are listed on the HomePath website. Once a suitable property is found, borrowers must work with a real estate agent who is registered with HomePath to submit an offer.

After the offer is accepted, the borrower will need to complete a loan application, which includes providing personal and financial information such as income, credit history, and employment details. Additionally, the borrower must submit documentation related to the property, including a purchase contract, property inspection report, and renovation plans. The lender will then review the application and conduct an appraisal to determine the property's value and the feasibility of the proposed renovations.

The approval process for the HomePath Renovation Loan typically takes several weeks, during which time the lender may request additional documentation or clarification on certain aspects of the application. Once the loan is approved, the borrower will need to finalize the purchase of the property and begin the renovation process within a specified timeframe, usually within 60 days of loan closing. Throughout the renovation process, the borrower will need to provide regular updates and documentation to the lender to ensure that the project is progressing as planned.

It is important to note that the HomePath Renovation Loan program has specific guidelines and requirements that must be met in order to qualify for the loan. Borrowers should carefully review these guidelines and work with a qualified lender to ensure that they are eligible for the program and that they understand the terms and conditions of the loan. By following the steps outlined above and providing all necessary documentation in a timely manner, borrowers can increase their chances of successfully obtaining a HomePath Renovation Loan and completing their property renovation project.

Frequently asked questions

No, the HomePath Renovation Loan Program was discontinued by Fannie Mae in 2018. It was a popular option for buyers looking to finance renovations, but it is no longer available.

The HomePath Renovation Loan Program was a mortgage program offered by Fannie Mae that allowed homebuyers to finance the cost of renovations into their mortgage. It was designed to help buyers purchase homes that needed repairs or updates.

Yes, there are several alternative programs available for financing home renovations. Some popular options include the FHA 203(k) loan, the VA Renovation Loan, and the Fannie Mae HomeStyle Renovation Loan. These programs allow buyers to finance the cost of renovations into their mortgage, similar to the HomePath Renovation Loan Program.