When considering whether your bonus counts as income for loan purposes, it's essential to understand how lenders evaluate your financial situation. Lenders typically assess your income to determine your ability to repay a loan, and bonuses can be a significant part of your overall earnings. In most cases, bonuses are considered income for loan applications, but the specific treatment may vary depending on the lender's policies and the type of loan you're applying for. Some lenders may require proof of consistent bonus income over a certain period, while others may consider it as part of your gross income. It's crucial to check with your lender and provide all necessary documentation to ensure your bonus is accurately accounted for in your loan application.

Explore related products

What You'll Learn

- Definition of Income: Understanding what qualifies as income for loan applications

- Types of Bonuses: Differentiating between various bonus types and their impact

- Lender Policies: Exploring how different lenders treat bonuses in income calculations

- Documentation Requirements: What documentation is needed to prove bonus income

- Impact on Loan Eligibility: How bonuses affect loan eligibility and borrowing power

![]()

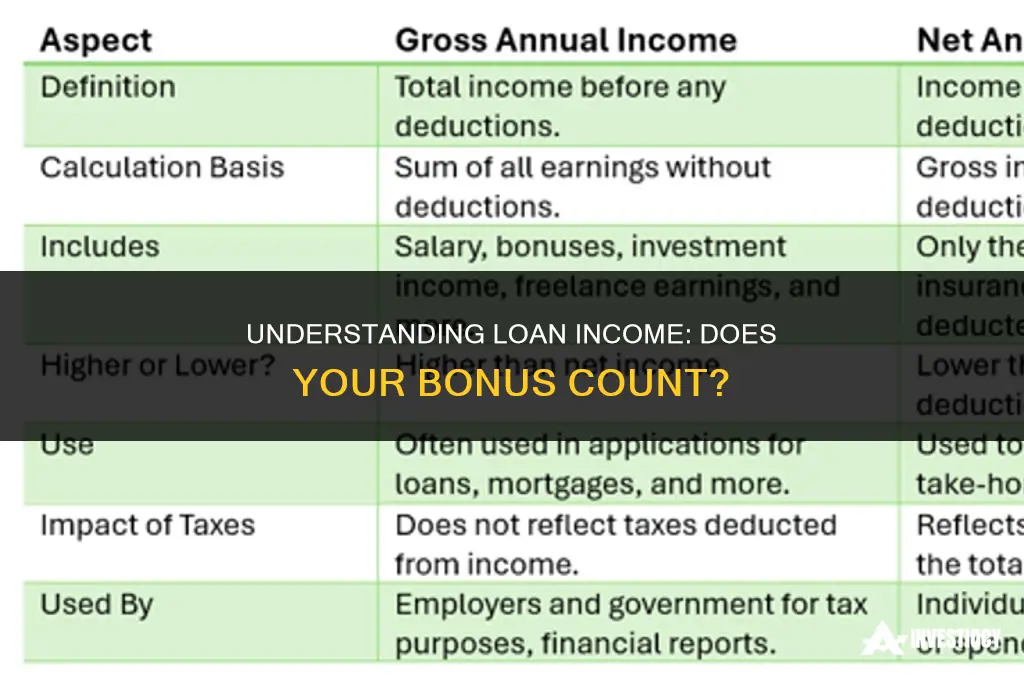

Definition of Income: Understanding what qualifies as income for loan applications

Lenders typically consider income to be any regular and predictable earnings that an individual receives. This can include wages, salaries, tips, commissions, and bonuses, as well as income from investments, rental properties, and certain government benefits. However, not all types of income are treated equally when it comes to loan applications. For example, some lenders may only consider income that is guaranteed and ongoing, while others may take into account irregular or seasonal income.

Bonuses can be a tricky area when it comes to loan applications, as they are often seen as irregular income. While some lenders may consider bonuses as part of an individual's overall income, others may not. It ultimately depends on the lender's specific criteria and the nature of the bonus itself. For example, if a bonus is a one-time payment, it may not be considered as regular income. However, if a bonus is part of a regular incentive structure and is paid out consistently, it may be taken into account.

When applying for a loan, it's important to understand how the lender defines income and what types of income they will consider. This can help you to determine whether your bonus will be counted as income and how it may impact your loan application. It's also important to note that even if your bonus is not considered as income, it may still be taken into account in other ways, such as when calculating your debt-to-income ratio.

In conclusion, the definition of income can vary significantly between lenders, and it's crucial to understand how your specific lender defines income when applying for a loan. While bonuses may not always be considered as regular income, they can still play a role in your overall financial picture and may be taken into account in other ways. By understanding the lender's criteria and providing accurate information about your income, you can increase your chances of a successful loan application.

Navigating Loan Dynamics: The Impact of Multiple Buyers Explained

You may want to see also

Explore related products

![]()

Types of Bonuses: Differentiating between various bonus types and their impact

Bonuses come in various forms, each with its own implications for your income and, consequently, your loan applications. Understanding the different types of bonuses and how they are treated by lenders is crucial for accurate financial planning.

Performance Bonuses: These are typically awarded based on an employee's performance and can be a significant part of their annual income. Lenders often consider performance bonuses as part of your gross income when calculating your debt-to-income ratio for loans. However, they may require proof of consistency in receiving such bonuses to ensure they are not one-time windfalls.

Sign-On Bonuses: These are upfront payments made to new employees as an incentive to join a company. Unlike performance bonuses, sign-on bonuses are usually considered separately from your regular income. Lenders may view them as a non-recurring source of income and might not include them in your gross income calculation for loan purposes.

Referral Bonuses: Companies often reward employees for referring new hires. These bonuses are generally treated similarly to sign-on bonuses, as they are not a regular part of your income. Lenders are likely to exclude referral bonuses from your income when assessing your loan eligibility.

Holiday Bonuses: These are additional payments made during the holiday season, which can be a regular occurrence in some industries. Holiday bonuses are typically considered part of your gross income by lenders, especially if they are consistent and predictable.

Profit-Sharing Bonuses: Some companies distribute a portion of their profits to employees as bonuses. These are usually considered part of your gross income, as they are directly tied to the company's financial performance and are often received annually.

Understanding how each type of bonus impacts your income is essential when applying for loans. Lenders will scrutinize your income sources to determine your ability to repay the loan, and knowing how to present your bonus income accurately can improve your chances of loan approval.

Unlocking the Potential: How MSHDA Loans Can Fulfill Your $7,500 Dream

You may want to see also

Explore related products

![]()

Lender Policies: Exploring how different lenders treat bonuses in income calculations

Lenders have varying policies when it comes to treating bonuses as income for loan applications. Some lenders may consider bonuses as part of your gross income, while others may not. This discrepancy can significantly impact your loan eligibility and the amount you can borrow. For instance, if a lender considers your bonus as income, it may increase your debt-to-income ratio, potentially disqualifying you for a loan or reducing the loan amount.

To navigate this complexity, it's essential to understand how different types of lenders approach bonus income. Traditional banks and credit unions often have more stringent guidelines compared to online lenders or alternative financing options. For example, a traditional bank may require you to provide proof of consistent bonus income over several years before considering it in your loan application. In contrast, an online lender might be more lenient and consider bonuses received in the previous year or even offer loans based on projected bonus income.

When applying for a loan, it's crucial to review the lender's specific policies regarding bonus income. This information is typically available on the lender's website or can be obtained by contacting their customer service. Understanding these policies can help you prepare your application and increase your chances of approval. Additionally, consider shopping around and comparing lenders to find one that offers the most favorable terms for your situation.

In some cases, lenders may require additional documentation to verify your bonus income, such as pay stubs, tax returns, or a letter from your employer. Being prepared to provide this documentation can streamline the loan application process and improve your likelihood of securing the loan. It's also important to note that some lenders may have specific requirements for the type of bonus income they consider, such as distinguishing between discretionary bonuses and guaranteed bonuses.

Ultimately, the key to successfully navigating lender policies regarding bonus income is to be informed and proactive. By understanding the different approaches lenders take and preparing your application accordingly, you can increase your chances of securing the loan you need.

Navigating Loan Options in Michigan: What You Need to Know

You may want to see also

Explore related products

![]()

Documentation Requirements: What documentation is needed to prove bonus income?

Lenders typically require specific documentation to verify bonus income when considering it for loan applications. This often includes a copy of the bonus agreement or contract, which outlines the terms and conditions of the bonus payment. Additionally, lenders may request a letter from the employer confirming the bonus amount and the likelihood of its recurrence. Pay stubs or bank statements showing the bonus deposit can also be required to substantiate the income.

In some cases, lenders might ask for tax returns or W-2 forms to further validate the bonus income. This is particularly true if the bonus is a significant portion of the borrower's overall income. The documentation process ensures that the lender has a clear understanding of the borrower's financial situation and can make an informed decision about the loan.

It's important for borrowers to gather all necessary documentation before applying for a loan to streamline the process and increase their chances of approval. Working closely with a loan officer or financial advisor can help ensure that all required documents are prepared and submitted correctly.

Understanding Your 401(k) Balance: Does It Include Your Loan?

You may want to see also

Explore related products

![]()

Impact on Loan Eligibility: How bonuses affect loan eligibility and borrowing power

Lenders typically consider bonuses as part of your gross income when assessing your loan eligibility. This means that a bonus can increase your borrowing power, as it contributes to a higher income figure. However, the impact of a bonus on your loan eligibility is not always straightforward and can vary depending on several factors.

One key consideration is the frequency and consistency of your bonuses. If you receive bonuses regularly, lenders may view them as a stable source of income and factor them into your debt-to-income ratio (DTI). This can improve your chances of qualifying for a loan and may allow you to borrow a larger amount. On the other hand, if your bonuses are irregular or unpredictable, lenders may be more cautious and may not give them as much weight when calculating your income.

Another factor to consider is the size of your bonus relative to your base salary. If your bonus is a significant portion of your overall income, it can have a substantial impact on your loan eligibility. Lenders may require additional documentation or verification to ensure that the bonus is legitimate and sustainable. They may also consider the bonus as a one-time event rather than a recurring source of income, which could limit its impact on your borrowing power.

It's also important to note that different types of loans may have varying requirements when it comes to bonuses. For example, mortgage lenders may have more stringent criteria for considering bonuses as income compared to personal loan lenders. Additionally, some lenders may have specific policies or guidelines regarding the treatment of bonuses, so it's essential to shop around and compare lenders to find the best option for your situation.

In conclusion, while bonuses can positively impact your loan eligibility and borrowing power, it's crucial to understand the nuances and factors that lenders consider. By being aware of these factors and taking steps to ensure that your bonuses are properly documented and verified, you can maximize the benefits of your bonus income when applying for loans.

Exploring the Benefits: Does Mudra Loan Offer a Subsidy?

You may want to see also

Frequently asked questions

Yes, your bonus typically counts as income when applying for loans. Lenders often consider bonuses as part of your overall income to determine your ability to repay the loan.

Lenders usually calculate your income by averaging your bonus over a certain period, often the past two years. They may also consider the stability and consistency of your bonus payments.

You will typically need to provide proof of your bonus income, such as pay stubs, tax returns, or a letter from your employer confirming the bonus amount and frequency.