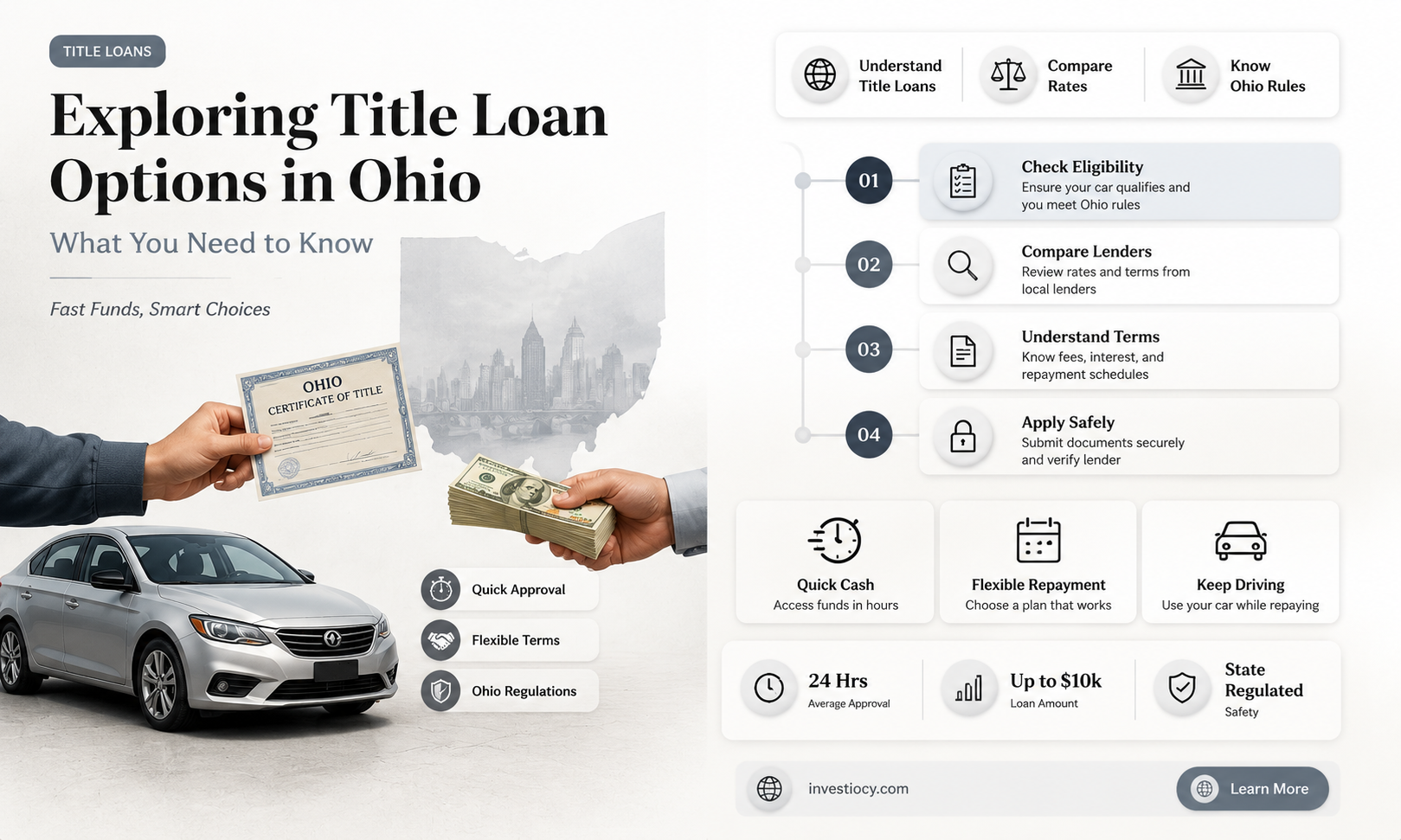

Ohio does permit title loans, which are short-term, high-interest loans secured by the title of a vehicle. These loans are often sought by individuals who need quick cash and may not have access to other forms of credit. However, it's important to note that title loans in Ohio come with significant risks, including the potential for the lender to repossess the vehicle if the borrower fails to repay the loan as agreed. Borrowers should carefully consider the terms and conditions of a title loan before entering into such an agreement, and explore alternative options if possible.

Explore related products

What You'll Learn

- Eligibility Criteria: Requirements for obtaining a title loan in Ohio, including vehicle ownership and identification

- Loan Amounts: Typical ranges of title loan amounts available in Ohio, based on vehicle value

- Interest Rates and Fees: Average interest rates and additional fees associated with title loans in the state

- Repayment Terms: Standard repayment periods and options for title loans in Ohio

- Legal Regulations: Overview of the legal framework governing title loans in Ohio, including consumer protections

![]()

Eligibility Criteria: Requirements for obtaining a title loan in Ohio, including vehicle ownership and identification

To obtain a title loan in Ohio, there are specific eligibility criteria that must be met. One of the primary requirements is that the applicant must own a vehicle outright, with no outstanding liens or loans against it. This means that the vehicle must be fully paid off and the title must be in the applicant's name. Additionally, the vehicle must be in good working condition and meet certain age and mileage requirements, as older or high-mileage vehicles may not be accepted as collateral for a title loan.

In terms of identification, applicants must provide a valid government-issued ID, such as a driver's license or state ID. They must also be at least 18 years old and a resident of Ohio. Proof of residency, such as a utility bill or lease agreement, may be required to verify the applicant's address. Furthermore, some title loan lenders in Ohio may require additional documentation, such as proof of income or employment, to ensure that the applicant has the means to repay the loan.

It's important to note that while these are the general eligibility criteria for obtaining a title loan in Ohio, individual lenders may have their own specific requirements. Therefore, it's recommended that applicants shop around and compare different lenders to find the best terms and conditions for their situation. Additionally, applicants should be aware of the potential risks associated with title loans, such as high interest rates and the possibility of losing their vehicle if they default on the loan.

In conclusion, to obtain a title loan in Ohio, applicants must meet certain eligibility criteria, including vehicle ownership and identification requirements. By understanding these criteria and shopping around for the best lender, applicants can increase their chances of obtaining a title loan that meets their needs. However, it's important to carefully consider the potential risks and consequences before taking out a title loan.

Exploring Ocwen's Role in Loan Origination: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Loan Amounts: Typical ranges of title loan amounts available in Ohio, based on vehicle value

In Ohio, title loan amounts typically range from $100 to $10,000, depending on the value of the vehicle used as collateral. The loan amount is usually a percentage of the vehicle's current market value, with lenders often offering between 25% to 50% of the car's worth. For instance, if a borrower's vehicle is valued at $5,000, they might be eligible for a title loan ranging from $1,250 to $2,500.

Several factors influence the specific loan amount a borrower can receive. These include the make, model, year, mileage, and overall condition of the vehicle. Lenders may also consider the borrower's income and credit history to determine their ability to repay the loan. Additionally, some lenders might impose minimum and maximum loan amounts, which can vary significantly from one company to another.

It's important for borrowers to understand that title loans are secured loans, meaning the lender has the right to repossess the vehicle if the borrower fails to repay the loan as agreed. Therefore, borrowers should carefully consider their financial situation and the value of their vehicle before taking out a title loan. They should also shop around for the best rates and terms, as these can vary widely among different lenders in Ohio.

When applying for a title loan, borrowers will typically need to provide proof of ownership, a government-issued ID, and proof of income. The lender will then assess the vehicle's value and determine the loan amount based on their criteria. If approved, the borrower will receive the loan funds and must repay the principal plus interest within the agreed-upon timeframe, usually ranging from 30 days to several months.

In conclusion, while title loans can provide quick access to cash for Ohio residents, it's crucial for borrowers to understand the risks and responsibilities involved. By carefully evaluating their financial situation and the terms of the loan, borrowers can make informed decisions about whether a title loan is the right option for their needs.

Tool Lending at O'Reilly: A Comprehensive Guide for DIY Enthusiasts

You may want to see also

Explore related products

![]()

Interest Rates and Fees: Average interest rates and additional fees associated with title loans in the state

Ohio does permit title loans, and these loans come with specific interest rates and fees that borrowers should be aware of. Title loans in Ohio are regulated by the Ohio Revised Code, which sets the maximum interest rate at 28% per annum. However, the actual interest rates charged by lenders can vary, and it's not uncommon for rates to be significantly higher, sometimes reaching triple digits when annualized.

In addition to interest rates, title loan borrowers in Ohio may also face various fees. These can include origination fees, which are charged for processing the loan application; lien fees, which cover the cost of placing a lien on the vehicle title; and repossession fees, which are incurred if the lender needs to repossess the vehicle due to default. Some lenders may also charge for additional services like roadside assistance or credit reporting.

The total cost of a title loan in Ohio can quickly add up, making it a potentially expensive form of borrowing. For instance, if a borrower takes out a $1,000 title loan with a 30-day term and an annual interest rate of 25%, they would owe approximately $120.83 in interest and fees by the end of the term, in addition to the principal amount. This underscores the importance of carefully considering the costs and risks associated with title loans before proceeding.

It's also worth noting that Ohio law requires title loan lenders to provide borrowers with a written agreement that clearly outlines the terms of the loan, including the interest rate, fees, and repayment schedule. Borrowers should review this agreement thoroughly and ask questions about any terms they do not understand. Additionally, borrowers have the right to cancel a title loan within three business days of signing the agreement, provided they return the loan proceeds to the lender.

In conclusion, while title loans can provide quick access to cash for Ohio residents, they come with significant costs and risks. Borrowers should be mindful of the interest rates and fees associated with these loans and should carefully consider their options before entering into a title loan agreement.

Exploring Loan Modification Options with Ocwen: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Repayment Terms: Standard repayment periods and options for title loans in Ohio

In Ohio, title loans typically come with repayment terms that can vary significantly depending on the lender and the specific loan agreement. Standard repayment periods for title loans in the state generally range from 30 days to several months. However, some lenders may offer longer repayment terms, potentially extending up to a year or more, especially for larger loan amounts.

One common repayment option for title loans in Ohio is a single lump-sum payment, where the borrower pays off the entire loan amount, including interest and fees, in one go at the end of the repayment period. This option is often preferred by lenders as it ensures they receive the full amount owed. However, it can be challenging for borrowers who may not have the financial means to come up with a large sum of money in a short period.

Another repayment option that some lenders in Ohio may offer is installment payments. With this option, the borrower pays off the loan in smaller, regular installments over the course of the repayment period. This can make it easier for borrowers to manage their finances and ensure they can meet their repayment obligations. However, installment payments may come with higher interest rates or fees, as the lender takes on more risk by allowing the borrower to pay off the loan over time.

It's important for borrowers in Ohio to carefully review the repayment terms of any title loan agreement before signing. They should consider factors such as the length of the repayment period, the total amount they will need to pay back, and the feasibility of making the required payments. Borrowers should also be aware of any potential penalties or fees for late payments or defaulting on the loan.

In conclusion, repayment terms for title loans in Ohio can vary, and borrowers should carefully consider their options and financial situation before entering into a loan agreement. Understanding the repayment terms and obligations is crucial for ensuring a positive borrowing experience and avoiding potential financial difficulties.

Explore related products

![]()

Legal Regulations: Overview of the legal framework governing title loans in Ohio, including consumer protections

Ohio has a comprehensive legal framework that governs title loans, designed to protect consumers and regulate the industry. Title loans in Ohio are subject to specific statutes and regulations that cap interest rates, limit loan amounts, and mandate disclosure requirements. These laws are enforced by the Ohio Consumer Financial Protection Bureau, which ensures that lenders comply with the state's regulations and that consumers are treated fairly.

One key aspect of Ohio's title loan regulations is the interest rate cap. The state has set a maximum interest rate of 28% per annum on title loans, which is significantly lower than the rates charged in some other states. This cap helps to prevent predatory lending practices and ensures that consumers are not burdened with exorbitant interest charges. Additionally, Ohio law requires that lenders provide clear and conspicuous disclosures to borrowers, including the total amount of the loan, the interest rate, and the repayment terms.

Another important consumer protection in Ohio is the requirement for lenders to obtain a license from the state before offering title loans. This licensing process helps to weed out unscrupulous lenders and ensures that only reputable companies are allowed to operate in the state. Furthermore, Ohio law prohibits lenders from engaging in certain practices, such as making loans to individuals who are already indebted to another title loan lender or who have had a title loan repossessed within the past 30 days.

In terms of loan amounts, Ohio law limits the maximum amount that can be borrowed through a title loan to $10,000. This cap helps to prevent consumers from taking on more debt than they can reasonably repay. Additionally, the state requires that lenders offer repayment terms of at least 30 days, which gives borrowers sufficient time to repay the loan without facing undue financial strain.

Overall, Ohio's legal framework for title loans provides robust consumer protections and helps to ensure that the industry operates in a fair and transparent manner. By capping interest rates, limiting loan amounts, and mandating disclosure requirements, the state has taken significant steps to protect its residents from predatory lending practices and to promote responsible borrowing.

Frequently asked questions

Yes, Ohio does offer title loans. Title loans are a type of secured loan where the borrower uses their vehicle title as collateral.

To qualify for a title loan in Ohio, you typically need to be at least 18 years old, have a valid government-issued ID, and own a vehicle with a clear title. The vehicle must be in working condition, and you'll need to provide proof of income and residency.

The amount you can borrow with a title loan in Ohio depends on the value of your vehicle and your ability to repay the loan. Loan amounts can range from a few hundred to several thousand dollars.

Title loans in Ohio come with high interest rates and fees, which can make them expensive. If you fail to repay the loan on time, you risk losing your vehicle to repossession. It's important to carefully consider the terms and conditions before taking out a title loan.