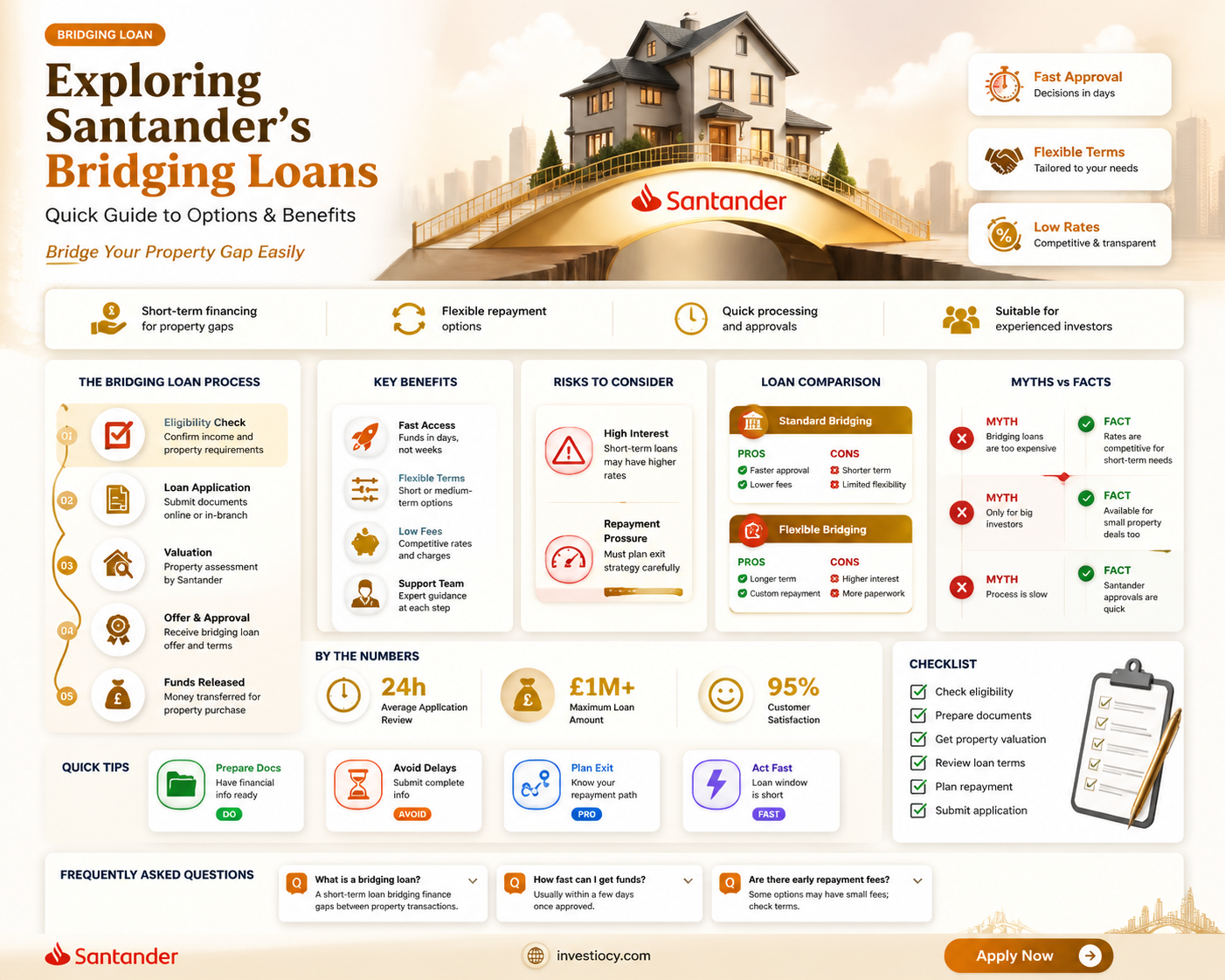

Santander, a prominent global banking group, offers a wide range of financial products and services, including various types of loans. One specific type of loan that individuals and businesses may seek is a bridging loan, which is a short-term loan designed to cover expenses until a longer-term financing solution is secured. Bridging loans are often used in real estate transactions, business acquisitions, or other situations where immediate funds are needed but the primary source of funding is not yet available. Given Santander's extensive portfolio of financial offerings, it is reasonable to inquire whether they provide bridging loans to their customers.

| Characteristics | Values |

|---|---|

| Loan Type | Bridging Loan |

| Lender | Santander |

| Purpose | Short-term financing to bridge the gap between selling a property and buying a new one |

| Eligibility | Typically available to homeowners who are in the process of buying a new property |

| Loan Amount | Varies, usually up to a certain percentage of the property value |

| Interest Rates | Competitive, fixed or variable rates |

| Repayment Terms | Short-term, usually 6 to 12 months |

| Security | Secured against the property |

| Application Fee | May apply, varies by lender |

| Valuation Fee | May apply, varies by lender |

| Legal Fees | May apply, varies by lender |

| Early Repayment | Possible, may incur penalties |

| Loan-to-Value | Typically up to 70-80% of the property value |

| Credit Check | Yes, creditworthiness is assessed |

| Documentation | Proof of identity, income, property ownership, and purchase agreement |

| Approval Time | Varies, usually quicker than traditional mortgages |

| Funding Time | Varies, usually within a few weeks of approval |

Explore related products

What You'll Learn

- Eligibility Criteria: Requirements for businesses or individuals to qualify for a bridging loan from Santander

- Loan Terms: Duration, interest rates, and repayment conditions specific to Santander's bridging loans

- Application Process: Steps and documentation needed to apply for a bridging loan with Santander

- Fees and Costs: Any associated fees, penalties, or additional costs with Santander's bridging loans

- Customer Reviews: Feedback and experiences from customers who have used Santander's bridging loan services

![]()

Eligibility Criteria: Requirements for businesses or individuals to qualify for a bridging loan from Santander

To qualify for a bridging loan from Santander, businesses and individuals must meet specific eligibility criteria. These requirements are designed to ensure that borrowers have the necessary financial stability and creditworthiness to repay the loan. One of the primary criteria is a strong credit history, demonstrating a track record of timely repayments and responsible financial management. Additionally, applicants must provide evidence of a stable income, which could include financial statements, tax returns, or pay stubs, depending on whether they are applying as a business or an individual.

Another key requirement is the presence of sufficient collateral. Bridging loans are typically secured against property or other valuable assets, so applicants must own assets that can be used as security for the loan. The value of the collateral must be sufficient to cover the loan amount, and Santander will conduct a thorough valuation to ensure that the assets are worth the claimed amount. Furthermore, businesses applying for a bridging loan may need to demonstrate a viable business plan, outlining their growth strategy and how the loan will be used to support their operations.

It's also important to note that Santander may have specific requirements regarding the purpose of the loan. Bridging loans are often used for short-term financing needs, such as purchasing new premises, expanding operations, or covering cash flow gaps. Applicants will need to clearly articulate the intended use of the funds and demonstrate how the loan will help them achieve their financial goals. Additionally, Santander may impose minimum and maximum loan amounts, so applicants should be aware of these limits when considering a bridging loan.

In summary, to qualify for a bridging loan from Santander, applicants must meet stringent eligibility criteria, including a strong credit history, stable income, sufficient collateral, and a clear purpose for the loan. By understanding these requirements and preparing their application accordingly, businesses and individuals can increase their chances of securing the financing they need.

Exploring Santander's Loan Options: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Loan Terms: Duration, interest rates, and repayment conditions specific to Santander's bridging loans

Santander's bridging loans are designed to provide short-term financing solutions for individuals and businesses. The duration of these loans typically ranges from a few months to a maximum of two years, allowing borrowers to bridge the gap between the sale of one property and the purchase of another, or to cover unexpected expenses. Interest rates on Santander's bridging loans are competitive and may vary depending on the loan amount, creditworthiness of the borrower, and the specific terms of the loan agreement.

Repayment conditions for Santander's bridging loans are structured to ensure that borrowers can comfortably meet their obligations. Borrowers are required to make regular interest payments throughout the loan term, with the principal amount due at the end of the term. In some cases, Santander may offer flexible repayment options, such as the ability to make overpayments or to extend the loan term, subject to certain conditions and fees.

It is important for borrowers to carefully review the terms and conditions of Santander's bridging loans before committing to a loan agreement. This includes understanding the total cost of the loan, including any fees and charges, as well as the potential risks and consequences of defaulting on the loan. Borrowers should also consider seeking independent financial advice to ensure that a bridging loan is the most suitable option for their specific circumstances.

In conclusion, Santander's bridging loans offer a viable financing solution for those in need of short-term funding. By understanding the loan terms, including duration, interest rates, and repayment conditions, borrowers can make informed decisions and effectively manage their financial obligations.

![]()

Application Process: Steps and documentation needed to apply for a bridging loan with Santander

To apply for a bridging loan with Santander, you'll need to follow a specific process and provide certain documentation. Here's a step-by-step guide to help you navigate the application:

- Initial Contact: Reach out to Santander's customer service team to express your interest in a bridging loan. They will guide you through the initial steps and provide you with the necessary forms.

- Documentation: Gather all required documents, which typically include:

- Proof of identity (e.g., passport, driver's license)

- Proof of address (e.g., utility bills, bank statements)

- Financial statements (e.g., income tax returns, bank statements)

- Details of the property you intend to purchase or refinance

- Evidence of the sale of your existing property (if applicable)

- Application Form: Fill out the application form provided by Santander. Be sure to include all requested information accurately and completely to avoid delays in processing.

- Submission: Submit your application form and supporting documentation to Santander. This can usually be done online, by mail, or in person at a Santander branch.

- Review and Approval: Santander will review your application and documentation. If additional information is needed, they will contact you. Once your application is approved, you will receive a loan offer detailing the terms and conditions.

- Acceptance and Funding: Review the loan offer carefully and accept it if you agree with the terms. Once you've accepted the offer, Santander will finalize the loan and disburse the funds according to the agreed-upon schedule.

Remember to keep all communication and documentation organized throughout the process. If you have any questions or concerns, don't hesitate to reach out to Santander's customer service team for assistance.

![]()

Fees and Costs: Any associated fees, penalties, or additional costs with Santander's bridging loans

Santander's bridging loans come with a variety of fees and costs that borrowers should be aware of. These include arrangement fees, valuation fees, legal fees, and interest charges. The arrangement fee is typically a percentage of the loan amount and covers the administrative costs of setting up the loan. Valuation fees are charged to assess the value of the property being used as security for the loan. Legal fees cover the costs of legal advice and documentation required for the loan. Interest charges are calculated based on the loan amount and the length of time the loan is outstanding.

In addition to these fees, borrowers may also be subject to penalties if they fail to meet the terms of the loan agreement. For example, if a borrower misses a repayment, they may be charged a late payment fee. If the borrower is unable to repay the loan in full at the end of the term, they may be charged an extension fee. It is important for borrowers to carefully review the terms and conditions of the loan agreement to understand all of the potential fees and penalties.

One unique aspect of Santander's bridging loans is that they offer a fixed interest rate for the duration of the loan. This can provide borrowers with certainty about their repayment costs, which can be helpful for budgeting purposes. However, it is important to note that the fixed interest rate may be higher than the variable interest rates offered by other lenders. Borrowers should carefully compare the interest rates and fees charged by different lenders to ensure they are getting the best deal.

Another important consideration for borrowers is the impact of fees and costs on the overall cost of the loan. While the interest rate is a key factor in determining the cost of the loan, fees and penalties can also add up quickly. Borrowers should use a loan calculator to estimate the total cost of the loan, including all fees and interest charges, before committing to a lender.

In conclusion, while Santander's bridging loans can provide a useful source of short-term financing, borrowers should be aware of the various fees and costs associated with these loans. By carefully reviewing the terms and conditions and comparing the costs of different lenders, borrowers can make an informed decision about whether a bridging loan is right for them.

![]()

Customer Reviews: Feedback and experiences from customers who have used Santander's bridging loan services

Santander's bridging loan services have garnered a mix of feedback from customers. A common theme in the reviews is the bank's efficient processing time. Many customers have noted that Santander's bridging loans are approved and disbursed relatively quickly compared to other lenders. This efficiency is particularly appreciated by those in urgent need of funds to bridge the gap between selling and buying properties.

However, some customers have expressed dissatisfaction with the interest rates charged by Santander. While competitive in some cases, there are instances where customers felt the rates were higher than expected, especially when compared to other bridging loan providers in the market. This has led to some customers seeking alternative lenders for their bridging loan needs.

Another area of concern for some customers is the lack of flexibility in repayment terms. Santander's bridging loans typically come with fixed repayment schedules, which may not be suitable for all borrowers. Customers who require more flexible repayment options, such as those who are awaiting the sale of a property, may find Santander's terms restrictive.

Despite these criticisms, Santander's bridging loan services have also received praise for their customer service. Many reviewers have noted that the bank's staff are helpful and responsive, providing clear guidance throughout the application and approval process. This level of customer support is seen as a significant advantage for those navigating the complexities of bridging loans.

In conclusion, while Santander's bridging loan services have their strengths, such as quick processing times and good customer service, they also have areas for improvement, including interest rates and repayment flexibility. Potential borrowers should weigh these factors carefully when considering Santander for their bridging loan needs.

Frequently asked questions

Yes, Santander does offer bridging loans. These loans are designed to help customers who are looking to purchase a new property before selling their existing one.

The purpose of a bridging loan is to provide temporary financing to cover the cost of purchasing a new property before the borrower's existing property is sold. This type of loan is often used by homebuyers who need to move quickly and don't have the time to wait for their current home to sell.

A bridging loan works by providing a short-term loan that is secured against the borrower's existing property. The loan amount is typically based on the value of the property being purchased, and the borrower is required to pay back the loan once their existing property is sold.

The advantages of a bridging loan include the ability to move quickly on a new property purchase, the flexibility to choose a loan term that suits the borrower's needs, and the potential to avoid paying double mortgage payments.

The disadvantages of a bridging loan include the high interest rates, the need to have a clear exit strategy in place, and the potential for the borrower to end up in negative equity if the value of their existing property falls.