Taking out a loan can have a significant impact on an individual's net worth. When you borrow money, you are essentially taking on debt, which is a liability that reduces your overall financial standing. The loan amount itself does not directly decrease your net worth, but the interest and fees associated with the loan can erode your wealth over time. Additionally, the loan payments can limit your ability to save and invest, further hindering your net worth growth. However, it's important to note that not all loans are created equal, and some, like mortgages or student loans, can be considered investments in your future earning potential or asset value.

Explore related products

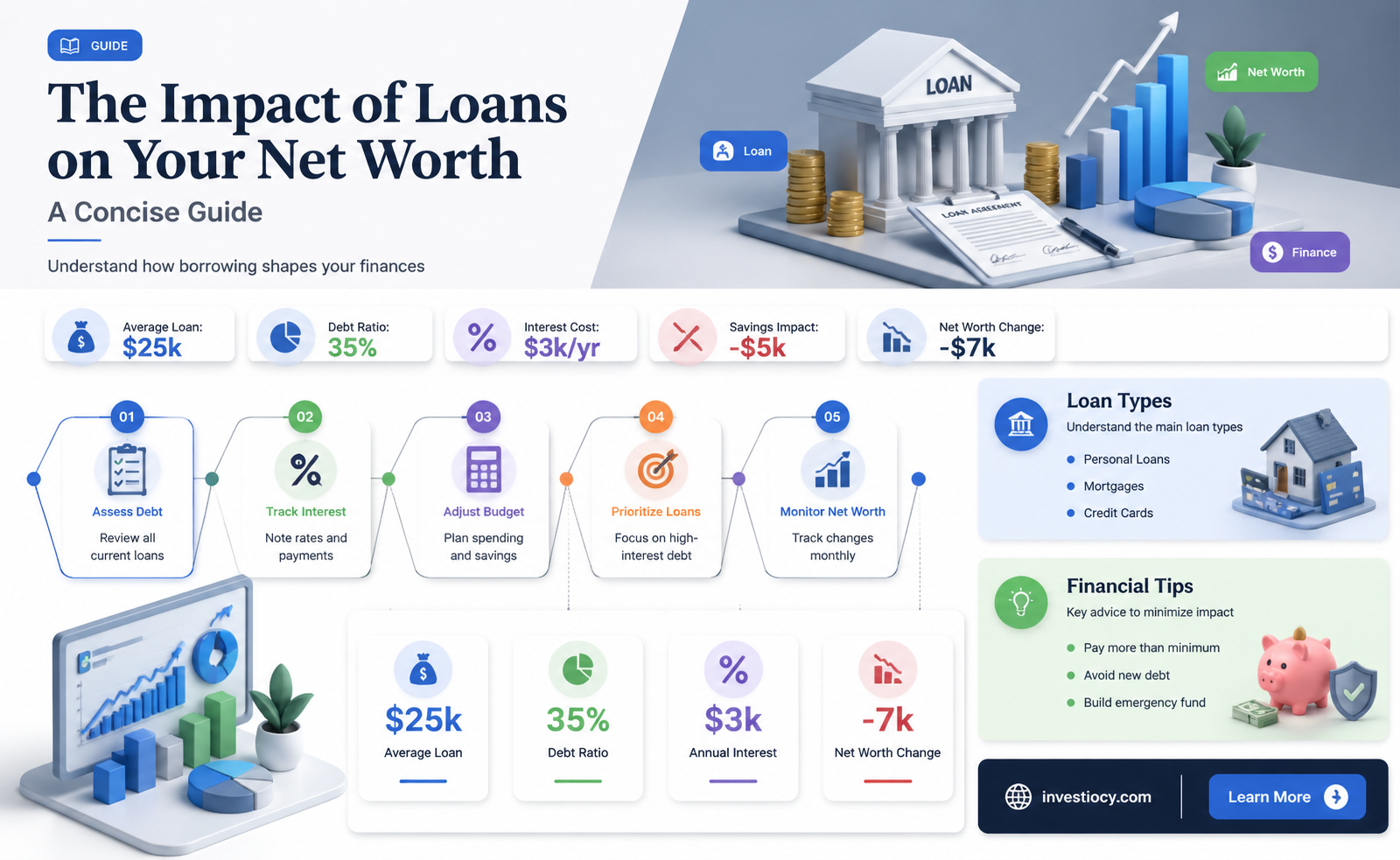

What You'll Learn

- Loan Basics: Understanding how loans work, including interest rates and repayment terms

- Impact on Net Worth: Analyzing how taking a loan affects your overall financial position

- Types of Loans: Exploring different loan types (e.g., personal, mortgage, student) and their implications

- Debt Management: Strategies for managing loan debt to minimize negative impacts on net worth

- Long-Term Effects: Considering the long-term consequences of loans on financial stability and wealth accumulation

![]()

Loan Basics: Understanding how loans work, including interest rates and repayment terms

Loans are a fundamental financial tool that many individuals and businesses utilize to achieve their goals. Understanding the basics of how loans work is crucial for making informed decisions about borrowing money. At its core, a loan is a sum of money lent by a financial institution or individual to a borrower, with the expectation that the borrower will repay the principal amount plus interest over a specified period.

Interest rates play a significant role in determining the cost of a loan. They can be fixed, meaning the rate remains constant throughout the loan term, or variable, where the rate fluctuates based on market conditions. The interest rate directly impacts the total amount repaid, with higher rates resulting in greater interest charges over time. Borrowers should carefully consider their financial situation and the current economic climate when choosing between fixed and variable interest rates.

Repayment terms are another critical aspect of loans. These terms outline the schedule for repaying the principal and interest, including the frequency of payments (e.g., monthly, quarterly, annually) and the duration of the loan. Longer repayment terms generally result in lower monthly payments but higher total interest costs, while shorter terms lead to higher monthly payments but lower overall interest expenses. Borrowers must balance their cash flow needs with their long-term financial goals when selecting repayment terms.

Understanding how loans work can help borrowers make better decisions about when and how to use debt to their advantage. By carefully considering interest rates and repayment terms, individuals can minimize the negative impact of loans on their net worth and maximize the benefits of borrowing for investments, education, or other productive purposes.

Understanding the Impact of Loans on Life Insurance Premiums

You may want to see also

Explore related products

![]()

Impact on Net Worth: Analyzing how taking a loan affects your overall financial position

Taking a loan can have a significant impact on your net worth, but the effect is not always straightforward. It's essential to understand that net worth is a snapshot of your financial position at a particular point in time, representing the difference between your assets and liabilities. When you take out a loan, you're essentially increasing your liabilities, which can decrease your net worth if not managed properly. However, loans can also be a strategic tool for building wealth, depending on their purpose and how they're utilized.

For instance, consider a scenario where an individual takes out a mortgage to purchase a home. In the short term, this loan increases their liabilities, potentially reducing their net worth. However, over time, as the home appreciates in value and the loan is paid down, the individual's net worth can actually increase. This is because the asset (the home) grows in value, while the liability (the mortgage) decreases. Moreover, the interest paid on the mortgage can be tax-deductible, providing additional financial benefits.

On the other hand, taking out a loan for discretionary spending, such as a vacation or luxury goods, can have a more detrimental impact on net worth. In this case, the loan increases liabilities without a corresponding increase in assets, leading to a decrease in net worth. Furthermore, the interest paid on such loans is typically not tax-deductible, adding to the financial burden.

To mitigate the negative impact of loans on net worth, it's crucial to focus on debt repayment and asset accumulation. Creating a budget that prioritizes loan payments can help reduce the principal balance more quickly, while also avoiding additional interest charges. Simultaneously, investing in assets that have the potential to appreciate in value, such as stocks, bonds, or real estate, can help offset the decrease in net worth caused by the loan.

In conclusion, the impact of taking a loan on your net worth depends on the purpose of the loan, how it's managed, and your overall financial strategy. By understanding the nuances of loan usage and focusing on responsible debt management, it's possible to minimize the negative effects of loans on net worth and even use them as a tool for building), wealth over time.

Explore related products

![]()

Types of Loans: Exploring different loan types (e.g., personal, mortgage, student) and their implications

Personal loans are typically unsecured, meaning they don't require collateral, and are based on the borrower's creditworthiness. They can be used for various purposes, such as consolidating debt, financing a large purchase, or covering unexpected expenses. The interest rates on personal loans can vary widely depending on the lender and the borrower's credit score.

Mortgage loans, on the other hand, are secured by the property being purchased. If the borrower defaults on the loan, the lender can foreclose on the property. Mortgages are typically long-term loans, with repayment periods ranging from 15 to 30 years. The interest rates on mortgages can be fixed or variable, and they are often lower than those on personal loans due to the collateral involved.

Student loans are designed to help cover the cost of higher education. They can be federal or private, and the interest rates and repayment terms can vary significantly. Federal student loans often have lower interest rates and more flexible repayment options, including income-driven repayment plans and loan forgiveness programs.

Each type of loan has its own implications for the borrower's net worth. Personal loans can be a good option for consolidating debt or financing a necessary expense, but they can also lead to overspending if not managed carefully. Mortgages can help build equity in a property over time, but they also come with significant interest costs and the risk of foreclosure if payments are not made. Student loans can be a necessary investment in one's education, but they can also lead to a significant amount of debt that can impact future financial goals.

When considering whether taking a loan will decrease net worth, it's important to weigh the potential benefits against the costs. Loans can provide access to capital that might not otherwise be available, but they also come with interest costs and the risk of default. Borrowers should carefully consider their financial situation and goals before taking on any new debt.

Explore related products

![]()

Debt Management: Strategies for managing loan debt to minimize negative impacts on net worth

Effective debt management is crucial for maintaining a healthy net worth. One key strategy is to prioritize high-interest debts for repayment first. This approach, known as the debt avalanche method, involves listing all debts in order of their interest rates and focusing on paying off the highest-rate debt while making minimum payments on others. Once the highest-rate debt is paid off, the next highest is targeted, and so on. This method can save money on interest charges over time, allowing for faster debt reduction and less negative impact on net worth.

Another strategy is the debt snowball method, which involves paying off debts in order of their balance, starting with the smallest. This approach can provide quick wins and a sense of accomplishment, which can be motivating. While it may not save as much on interest as the avalanche method, it can still be effective in reducing overall debt and improving net worth.

It's also important to consider the terms of the loan when managing debt. For example, some loans may have prepayment penalties, which can offset the benefits of early repayment. In such cases, it may be more beneficial to focus on other debts or investment opportunities. Additionally, borrowers should be aware of any variable interest rates on their loans, as these can fluctuate and impact the total cost of borrowing.

Consolidating debt can be another useful strategy. By combining multiple debts into a single loan with a lower interest rate, borrowers can simplify their payments and potentially save on interest. However, it's important to carefully consider the terms of the consolidation loan and ensure that it doesn't result in higher overall costs or longer repayment periods.

Finally, maintaining a good credit score is essential for effective debt management. A high credit score can qualify borrowers for lower interest rates on loans and credit cards, which can reduce the cost of borrowing and improve net worth over time. Regularly monitoring credit reports and addressing any errors or discrepancies can help maintain a strong credit profile.

Explore related products

![]()

Long-Term Effects: Considering the long-term consequences of loans on financial stability and wealth accumulation

The long-term effects of loans on financial stability and wealth accumulation are multifaceted and depend on various factors, including the type of loan, interest rates, repayment terms, and the borrower's financial discipline. While loans can provide immediate financial relief or enable significant purchases, such as a home or education, they can also have lasting implications on one's net worth if not managed properly. High-interest loans, for instance, can lead to a cycle of debt, where the borrower pays more in interest than the principal amount, significantly reducing their ability to accumulate wealth over time.

One of the primary long-term consequences of loans is the impact on credit scores. Timely repayments can improve creditworthiness, leading to better loan terms in the future. However, missed payments or defaults can severely damage credit scores, making it difficult to secure loans or credit cards at favorable rates. This can limit financial opportunities and increase the cost of borrowing, further hindering wealth accumulation.

Another consideration is the opportunity cost of taking a loan. The money spent on interest payments could have been invested in assets that generate returns, such as stocks, bonds, or real estate. Over time, the compounding effect of these investments could significantly increase net worth. Therefore, it's essential to weigh the benefits of taking a loan against the potential long-term financial gains that could be achieved through investing.

Moreover, loans can affect financial stability by increasing debt-to-income ratios. A high debt-to-income ratio can make it challenging to manage monthly expenses, leaving little room for savings or investments. This can lead to a precarious financial situation, where unexpected expenses or income loss can result in financial hardship.

To mitigate these long-term effects, borrowers should focus on developing a solid financial plan that includes strategies for debt repayment, savings, and investment. Seeking professional financial advice can also help in creating a roadmap for achieving financial stability and wealth accumulation while managing loans effectively.

In conclusion, while loans can be a necessary financial tool, their long-term effects on financial stability and wealth accumulation should not be overlooked. By understanding the potential consequences and implementing sound financial strategies, individuals can minimize the negative impacts of loans and work towards building a secure financial future.

Frequently asked questions

Not necessarily. Taking a loan increases your liabilities, but it doesn't directly decrease your net worth unless the loan is used to purchase an asset that depreciates in value or doesn't generate returns.

A loan can positively impact your net worth if it's used to invest in assets that appreciate in value or generate income, such as real estate or a business. The returns from these investments can offset the loan amount and increase your overall net worth.

Loans with high interest rates, such as credit card debt or payday loans, are more likely to decrease net worth over time due to the significant interest charges that can accumulate.

Yes, student loans can affect net worth. While they are often considered an investment in future earning potential, the interest that accrues on student loans can increase the total amount owed, potentially reducing net worth if not managed properly.

To minimize the negative impact of a loan on your net worth, focus on paying off high-interest loans first, make timely payments to avoid additional fees, and consider refinancing to lower interest rates. Additionally, ensure that the loan is used for productive purposes that can generate returns or increase asset value.