The new stimulus package has been a subject of much discussion, particularly regarding its provisions for businesses and individuals affected by the pandemic. One key aspect that many are inquiring about is whether the package includes Economic Injury Disaster Loans (EIDL). These loans have been a vital source of financial support for businesses struggling to stay afloat during these challenging times. The inclusion of EIDL loans in the stimulus package would provide a significant boost to these enterprises, helping them to recover and rebuild. However, the specifics of the package are complex, and understanding the details is crucial for those seeking assistance.

Explore related products

What You'll Learn

- EIDL Loan Eligibility: Details on which businesses qualify for Economic Injury Disaster Loans under the new stimulus

- Loan Terms and Conditions: Information about interest rates, repayment terms, and forgiveness options for EIDL loans

- Application Process: Steps and requirements for businesses to apply for EIDL loans, including necessary documentation

- Funding Timeline: Expected time frame for loan approval and disbursement of funds to eligible businesses

- Comparison with PPP Loans: Differences and similarities between EIDL loans and Paycheck Protection Program loans

![]()

EIDL Loan Eligibility: Details on which businesses qualify for Economic Injury Disaster Loans under the new stimulus

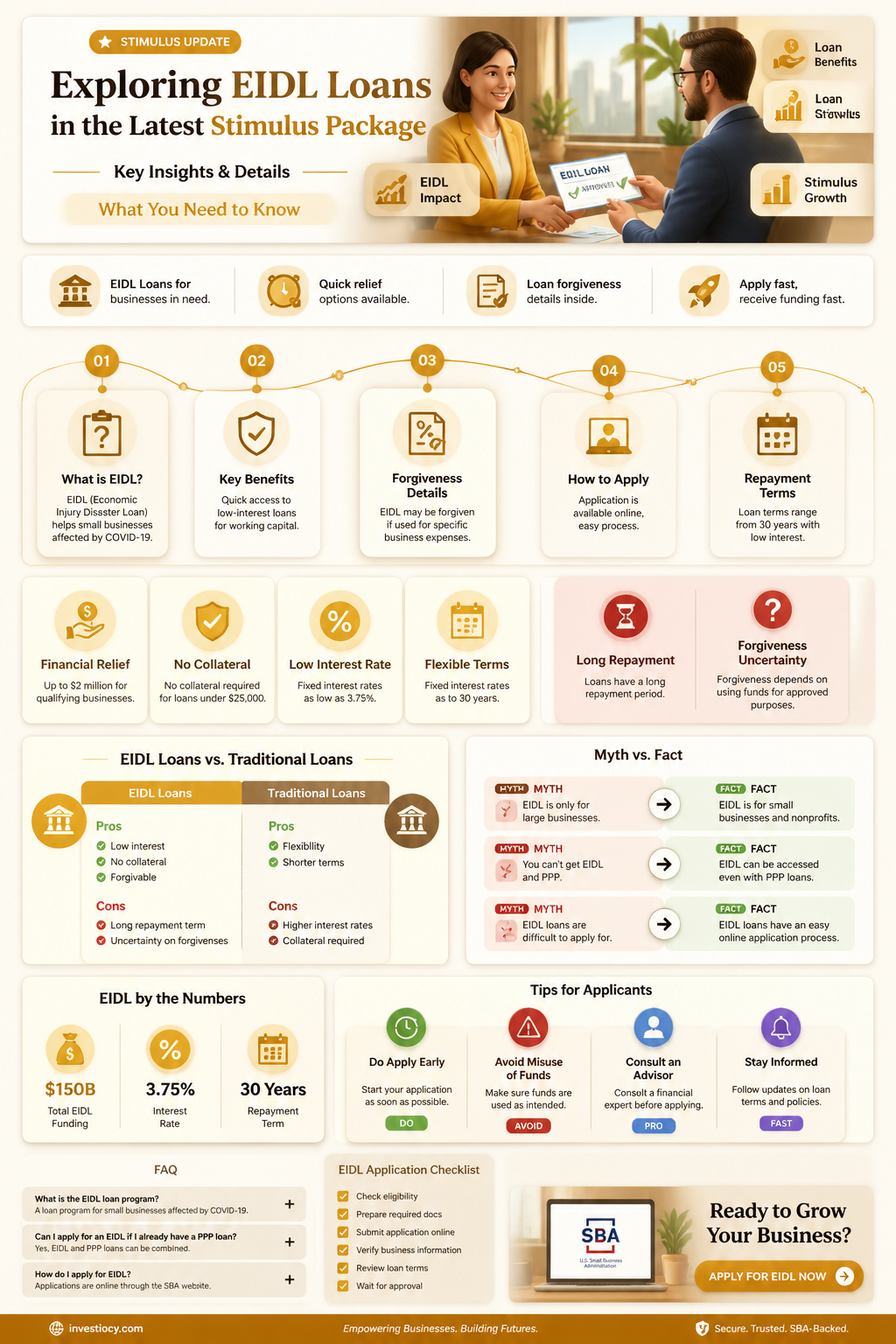

To qualify for an Economic Injury Disaster Loan (EIDL) under the new stimulus package, businesses must meet specific eligibility criteria. These loans are designed to provide financial assistance to small businesses and non-profit organizations that have suffered economic injury due to a declared disaster. The eligibility requirements include having a credit score of at least 680, being located in a declared disaster area, and demonstrating a direct economic impact from the disaster. Additionally, businesses must have been in operation for at least one year prior to the disaster declaration and must not have any outstanding tax liens or federal debt.

The application process for an EIDL involves submitting a formal loan application to the Small Business Administration (SBA), which includes providing detailed financial information and documentation of the economic impact. The SBA will then review the application and determine the loan amount based on the business's financial needs and ability to repay the loan. It's important to note that EIDLs are not grants and must be repaid with interest. However, the interest rates are typically lower than those of traditional loans, and the repayment terms can be up to 30 years.

One unique aspect of the new stimulus package is that it includes additional funding for EIDLs, which means that more businesses may be eligible for these loans than in previous years. Additionally, the package includes provisions for loan forgiveness for certain businesses that have been severely impacted by the disaster. This could provide significant relief for businesses that are struggling to recover from the economic downturn.

In conclusion, the new stimulus package includes important provisions for EIDL loans, which can provide critical financial assistance to businesses that have been affected by a declared disaster. By understanding the eligibility criteria and application process, businesses can take advantage of these loans to help them recover and rebuild.

Exploring Military Benefits: College Loan Forgiveness Options

You may want to see also

Explore related products

![]()

Loan Terms and Conditions: Information about interest rates, repayment terms, and forgiveness options for EIDL loans

The Economic Injury Disaster Loan (EIDL) program, a critical component of the federal government's response to economic crises, offers low-interest loans to businesses and non-profit organizations. These loans are designed to provide financial relief and help entities recover from economic losses due to disasters, including the COVID-19 pandemic. The terms and conditions of EIDL loans are particularly favorable, with interest rates that are significantly lower than those offered by private lenders. For example, as of my last update, the interest rate for businesses was 3.75%, while non-profits were offered an even lower rate of 2.75%. These rates are fixed for the life of the loan, providing borrowers with predictable monthly payments.

Repayment terms for EIDL loans are also designed to be manageable, with a maximum repayment period of 30 years. This extended timeframe allows businesses to spread out their payments over a longer period, reducing the immediate financial burden. The first payment is deferred for two years from the date of the loan disbursement, giving borrowers additional breathing room as they work to recover from their economic setbacks. During this deferment period, interest continues to accrue, but no payments are required. It's important to note that these loans do not have any prepayment penalties, allowing borrowers to pay off their loans early if they are able to do so.

One of the most attractive features of EIDL loans is the potential for loan forgiveness. Under certain conditions, a portion of the loan may be forgiven, reducing the overall amount that needs to be repaid. For instance, during the COVID-19 pandemic, the federal government announced that EIDL loans could be used to cover payroll and operating expenses, and a portion of these loans would be forgiven if specific criteria were met. This forgiveness option has been a lifeline for many businesses struggling to survive during these challenging times.

To qualify for an EIDL loan, businesses must demonstrate that they have suffered a substantial economic injury as a result of a declared disaster. This typically involves providing financial statements and other documentation to show the impact of the disaster on their operations. Once approved, the loan funds can be used for a variety of purposes, including rent, utilities, payroll, and other operating expenses. However, the funds cannot be used for new construction or to refinance existing debt.

In conclusion, the EIDL loan program offers a valuable source of financial assistance for businesses and non-profits affected by economic disasters. With its low interest rates, manageable repayment terms, and potential for loan forgiveness, this program provides a critical safety net for entities working to recover from financial setbacks. As with any loan program, it's essential for borrowers to carefully review the terms and conditions and to seek professional advice if needed to ensure that they are making informed decisions about their financial future.

Unraveling the Mystery: Missing Documents and Their Impact on Nelnet Loans

You may want to see also

Explore related products

![]()

Application Process: Steps and requirements for businesses to apply for EIDL loans, including necessary documentation

To apply for an Economic Injury Disaster Loan (EIDL), businesses must follow a specific process and meet certain requirements. The first step is to determine eligibility, which typically includes being a small business or non-profit organization located in a declared disaster area. Once eligibility is confirmed, the next step is to gather necessary documentation. This may include financial statements, tax returns, and other relevant business records. It's important to have these documents readily available to streamline the application process.

After gathering the required documentation, businesses can proceed to fill out the EIDL application form. This form will ask for detailed information about the business, including its legal structure, ownership, and financial status. It's crucial to provide accurate and complete information to avoid delays or rejection of the application. Once the form is completed, it can be submitted to the Small Business Administration (SBA) for review.

During the review process, the SBA may request additional documentation or clarification on certain aspects of the application. It's important to respond promptly to these requests to keep the process moving forward. If the application is approved, the business will be notified and provided with information on the loan terms, including the interest rate and repayment schedule.

One key aspect of the EIDL application process is understanding the specific requirements and timelines. For example, businesses may need to provide proof of insurance or demonstrate that they have been in operation for a certain period of time. Additionally, there may be deadlines for submitting applications, so it's important to stay informed about these dates to ensure timely submission.

In conclusion, the EIDL application process involves several steps and requirements that businesses must navigate to secure funding. By understanding the eligibility criteria, gathering necessary documentation, and providing accurate information on the application form, businesses can increase their chances of successfully obtaining an EIDL loan.

Explore related products

![]()

Funding Timeline: Expected time frame for loan approval and disbursement of funds to eligible businesses

The funding timeline for loan approval and disbursement of funds to eligible businesses under the new stimulus package is a critical aspect for many business owners. The Economic Injury Disaster Loan (EIDL) program, which is part of the stimulus package, provides financial assistance to businesses affected by the COVID-19 pandemic. The timeline for loan approval and disbursement can vary based on several factors, including the volume of applications, the efficiency of the application process, and the specific guidelines set by the Small Business Administration (SBA).

Typically, the EIDL loan approval process can take anywhere from a few days to several weeks. The SBA has streamlined the application process to expedite approvals, but the exact timeframe can still fluctuate. Once a loan is approved, the disbursement of funds usually occurs within a few business days. However, in some cases, it may take longer due to additional verification or processing requirements.

To navigate this timeline effectively, businesses should ensure they have all necessary documentation ready before submitting their application. This includes financial statements, tax returns, and other relevant business information. Additionally, staying informed about the latest updates and guidelines from the SBA can help businesses manage their expectations and plan accordingly.

It's also important for businesses to consider the potential impact of the loan terms on their financial situation. EIDL loans have specific repayment terms and interest rates that businesses need to be aware of before committing to the loan. By understanding the funding timeline and loan terms, businesses can make informed decisions about whether the EIDL program is the right fit for their needs.

In summary, the funding timeline for EIDL loans under the new stimulus package can vary, but businesses can take steps to expedite the process by being prepared and staying informed. By doing so, they can better manage their expectations and make informed decisions about their financial future.

Explore related products

![]()

Comparison with PPP Loans: Differences and similarities between EIDL loans and Paycheck Protection Program loans

The Economic Injury Disaster Loan (EIDL) program and the Paycheck Protection Program (PPP) are two distinct loan initiatives designed to support businesses during economic downturns. While both programs aim to provide financial assistance, they differ significantly in their structure, eligibility criteria, and repayment terms.

EIDL loans are long-term, low-interest loans provided by the Small Business Administration (SBA) to help businesses recover from declared disasters. These loans can be used to cover a wide range of expenses, including rent, utilities, and other operational costs. In contrast, PPP loans are short-term loans designed to help businesses maintain their payroll and cover certain other expenses during the COVID-19 pandemic. PPP loans are unique in that they can be forgiven if the borrower meets specific criteria, such as retaining employees and using the loan funds for eligible expenses.

One key difference between EIDL and PPP loans is the interest rate. EIDL loans typically have lower interest rates compared to PPP loans, making them more attractive for long-term financial support. However, PPP loans offer the potential for loan forgiveness, which can be a significant advantage for businesses struggling to recover from the pandemic.

Another important distinction is the repayment term. EIDL loans generally have longer repayment terms, often up to 30 years, allowing businesses more time to recover and repay the loan. PPP loans, on the other hand, have a shorter repayment term of two years, which can be challenging for businesses that are still struggling financially.

In terms of eligibility, both programs have specific criteria that businesses must meet. EIDL loans are available to businesses in declared disaster areas, while PPP loans are available to businesses that have been affected by the COVID-19 pandemic. Additionally, PPP loans have a cap on the amount that can be borrowed, based on the business's payroll, while EIDL loans do not have a specific cap but are limited by the SBA's lending authority.

Overall, while both EIDL and PPP loans provide valuable financial support to businesses, they serve different purposes and have distinct features. Understanding the differences between these two programs can help businesses make informed decisions about which loan option is best suited to their needs.

Frequently asked questions

Yes, the new stimulus package does include EIDL loans. The Economic Injury Disaster Loan (EIDL) program has been extended and expanded to provide further assistance to businesses affected by the pandemic.

The key changes include an increase in the maximum loan amount, a longer repayment term, and a deferred payment period. Additionally, the interest rates for EIDL loans have been reduced to make them more accessible for businesses in need.

Eligibility for an EIDL loan under the new stimulus package has been expanded. Businesses with fewer than 500 employees, including sole proprietors and independent contractors, are generally eligible. Additionally, businesses in certain industries, such as hospitality and tourism, may also qualify for EIDL loans.

Businesses can apply for an EIDL loan through the Small Business Administration (SBA) website. The application process has been streamlined to facilitate quicker approval and disbursement of funds. It is recommended that businesses gather all necessary documentation and information before starting the application process to ensure a smooth and efficient experience.