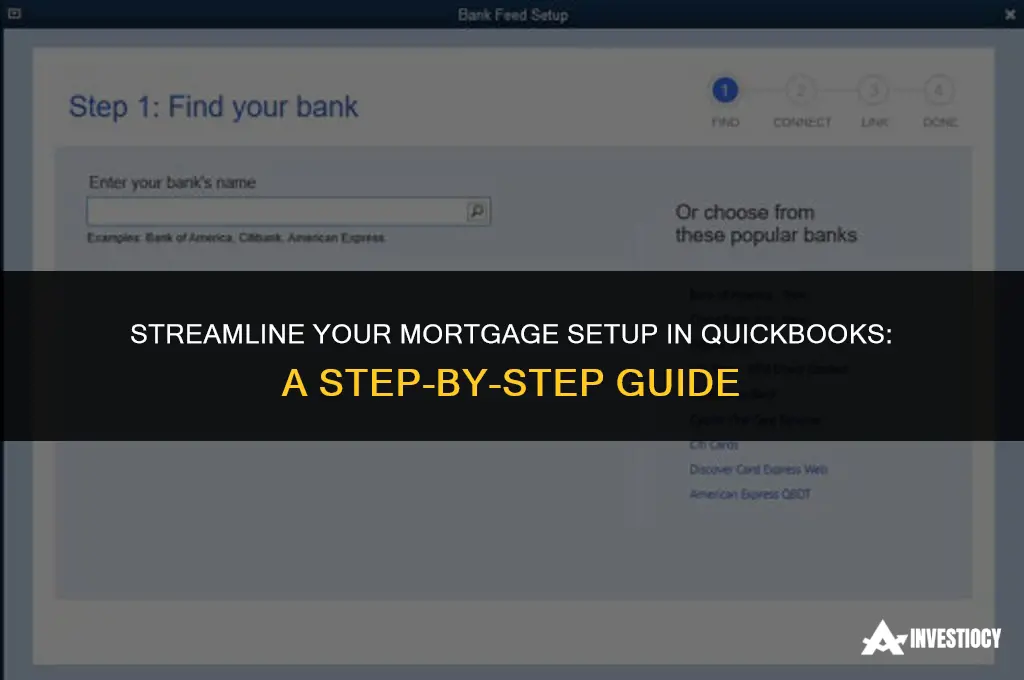

Setting up a mortgage in QuickBooks involves several key steps to ensure accurate financial tracking and reporting. First, you need to create a new loan account in QuickBooks to represent your mortgage. This account should be categorized under 'Long-Term Liabilities' to reflect the nature of the debt. Next, you'll need to record the initial mortgage loan amount as a credit to this new account. This will increase your liabilities on the balance sheet. Subsequently, you should set up a payment schedule that aligns with your mortgage terms, which can be done using QuickBooks' built-in payment reminders or by creating a recurring transaction. Each mortgage payment should be recorded as a debit to the loan account and a credit to your cash account, reflecting the reduction in the loan balance and the outflow of cash. Additionally, QuickBooks allows you to track the interest portion of your mortgage payments separately, which can be beneficial for tax purposes and financial analysis. By following these steps, you can effectively manage your mortgage within QuickBooks, ensuring that your financial records are up-to-date and accurate.

Explore related products

What You'll Learn

- Create a New Loan Account: Set up a new loan account in QuickBooks to track your mortgage payments

- Record Initial Loan Balance: Enter the initial loan balance as a liability on your balance sheet

- Schedule Regular Payments: Use QuickBooks to schedule regular mortgage payments, ensuring timely and accurate payment processing

- Track Interest and Principal: Monitor the interest and principal portions of each payment to understand your mortgage amortization

- Generate Reports: Create custom reports in QuickBooks to analyze your mortgage payment history and forecast future payments

![]()

Create a New Loan Account: Set up a new loan account in QuickBooks to track your mortgage payments

To create a new loan account in QuickBooks for tracking mortgage payments, begin by navigating to the "Lists" menu and selecting "Chart of Accounts." From here, you can right-click anywhere in the window and choose "New" to initiate the creation of a new account. Select "Loan" as the account type, and then choose "Mortgage Loan" from the sub-type options. Enter a name for the account, such as "Home Mortgage," and specify the account number if required by your accounting system.

Next, you'll need to set up the loan details. Click on the "Edit" menu and select "Edit Account." Go to the "Loan Info" tab and enter the loan amount, interest rate, loan term, and payment frequency. You can also specify the loan start date and the first payment due date. QuickBooks will use this information to calculate the payment schedule and amortization table for the loan.

Once the loan account is set up, you can start recording your mortgage payments. Go to the "Banking" menu and select "Make Payments." Choose the mortgage loan account from the list of accounts, enter the payment amount, and specify the payment date. QuickBooks will automatically apply the payment to the loan account and update the loan balance accordingly.

It's important to regularly review and reconcile your mortgage loan account in QuickBooks to ensure accuracy. You can do this by comparing the loan balance and payment history in QuickBooks with your bank statements and mortgage payment receipts. If you notice any discrepancies, you can make adjustments to the loan account or contact your lender to resolve the issue.

By setting up a new loan account in QuickBooks to track your mortgage payments, you can easily manage and monitor your home loan. This will help you stay on top of your payments, track your equity, and make informed financial decisions.

Navigating Mortgage Insurance Premiums: A Comprehensive Reporting Guide

You may want to see also

Explore related products

![]()

Record Initial Loan Balance: Enter the initial loan balance as a liability on your balance sheet

To record the initial loan balance in QuickBooks, you must first understand the importance of accurately entering this figure as a liability on your balance sheet. This is a crucial step in setting up a mortgage in the software, as it affects your financial reporting and tax calculations. Begin by navigating to the "Chart of Accounts" in QuickBooks and selecting "Liabilities" from the list. Then, choose "Add New" to create a new liability account specifically for your mortgage.

Once you've created the mortgage liability account, you're ready to record the initial loan balance. Click on the "Banking" menu and select "Make Deposits" to enter the loan amount as a deposit into your mortgage liability account. Be sure to use the correct account you just created for this purpose. After entering the deposit, QuickBooks will automatically update your balance sheet to reflect the new liability.

It's essential to double-check your work to ensure accuracy. Go to the "Reports" menu and select "Balance Sheet" to review your current financial standing. Verify that the mortgage liability is correctly listed and that the balance matches the initial loan amount. If you notice any discrepancies, return to the "Banking" menu and adjust the deposit as needed.

Recording the initial loan balance as a liability on your balance sheet is not only important for accurate financial reporting but also for tax purposes. The interest you pay on your mortgage may be tax-deductible, so it's crucial to have this information correctly recorded in QuickBooks. Additionally, tracking your mortgage payments and balance over time can help you make informed decisions about your financial future, such as refinancing or paying off your loan early.

In summary, recording the initial loan balance in QuickBooks involves creating a new liability account for your mortgage, entering the loan amount as a deposit, and verifying the accuracy of your work through financial reports. This process is essential for maintaining accurate financial records and making informed decisions about your mortgage and overall financial health.

Exploring Palm Beach County Mortgage Records: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Schedule Regular Payments: Use QuickBooks to schedule regular mortgage payments, ensuring timely and accurate payment processing

To schedule regular mortgage payments in QuickBooks, begin by setting up a new vendor for your mortgage lender. Enter the lender’s name, address, and other relevant details. Once the vendor is set up, create a new bill for the mortgage payment, specifying the amount, due date, and payment terms. QuickBooks allows you to automate the payment process by scheduling recurring bills. To do this, click on the "Schedule Recurring Bill" option and set the frequency of the payments (e.g., monthly). You can also specify the number of payments or set an end date for the recurring payments.

After scheduling the payments, it’s essential to ensure that your QuickBooks account has sufficient funds to cover the mortgage payments. You can set up a transfer from your checking account to the mortgage payment account to ensure that the funds are available when needed. Additionally, QuickBooks offers the option to track your mortgage payments and generate reports, providing you with a clear overview of your payment history and remaining balance.

One of the benefits of using QuickBooks for mortgage payments is the ability to make adjustments as needed. If your mortgage payment amount changes or if you need to make an extra payment, you can easily update the recurring bill settings. QuickBooks also allows you to track late fees or penalties, helping you stay on top of your mortgage payments and avoid any potential issues.

In summary, scheduling regular mortgage payments in QuickBooks is a straightforward process that can save you time and ensure accurate payment processing. By setting up a vendor, creating a bill, and scheduling recurring payments, you can automate your mortgage payments and focus on other aspects of your finances. QuickBooks’ reporting and tracking features provide additional benefits, allowing you to stay organized and informed about your mortgage payments.

Unlocking Your Illinois Home: A Guide to Mortgage Release

You may want to see also

Explore related products

![The Quick and Easy Mortgage Legislation Guide 2011 [Annotated]](https://m.media-amazon.com/images/I/41rAbFLjRIL._AC_UY218_.jpg)

![]()

Track Interest and Principal: Monitor the interest and principal portions of each payment to understand your mortgage amortization

To effectively track interest and principal in QuickBooks, you'll need to set up your mortgage as a long-term liability. This involves creating a new account specifically for your mortgage and entering the initial loan amount as a liability. Each payment you make will then be recorded as a reduction in this liability, with the interest portion being expensed and the principal portion reducing the outstanding balance.

One of the key benefits of tracking your mortgage in QuickBooks is the ability to generate detailed reports that show the breakdown of each payment. This can help you understand how much of your payment is going towards interest and how much is being applied to the principal balance. Over time, you'll be able to see how your payments are reducing the overall debt and how the interest expense is decreasing as the principal balance is paid down.

QuickBooks also allows you to set up automatic payments, which can help ensure that you never miss a mortgage payment. You can schedule these payments to be made on the same day each month, and QuickBooks will automatically record the payment and update your accounts accordingly. This can save you time and help you avoid late fees or penalties.

Another useful feature in QuickBooks is the ability to track escrow accounts. If your mortgage lender requires you to pay property taxes and insurance through an escrow account, QuickBooks can help you manage these payments as well. You can set up separate accounts for your escrow payments and track the funds as they are collected and disbursed.

In addition to tracking your mortgage payments, QuickBooks can also help you analyze your mortgage amortization schedule. This can help you understand how long it will take to pay off your mortgage and how much interest you will pay over the life of the loan. By running different scenarios, you can also see how changes in your payment amount or interest rate could affect your amortization schedule.

Overall, tracking your mortgage in QuickBooks can provide you with valuable insights into your home loan and help you make informed financial decisions. By understanding the breakdown of each payment and how your mortgage amortizes over time, you can better manage your finances and work towards paying off your mortgage more quickly.

Uncovering Deception: A Guide to Reporting Mortgage Fraud

You may want to see also

Explore related products

![NMLS Study Guide 2026-2027 - 5 Full-Length Practice Tests, SAFE MLO Exam Prep Secrets Book for the Mortgage Loan Originator Exam: [4th Edition]](https://m.media-amazon.com/images/I/717iHac5CwL._AC_UL320_.jpg)

![]()

Generate Reports: Create custom reports in QuickBooks to analyze your mortgage payment history and forecast future payments

To generate reports in QuickBooks for analyzing mortgage payment history and forecasting future payments, begin by navigating to the "Reports" tab on the main dashboard. From there, select "Custom Report" and choose "Transaction Detail" as the report type. This will allow you to create a detailed report of all mortgage-related transactions.

Next, set the date range for the report to include all past mortgage payments. You can also filter the report by selecting "Mortgage" from the "Account" dropdown menu. This will ensure that only transactions related to your mortgage are included in the report.

Once you have generated the report, you can analyze the data to identify trends and patterns in your mortgage payment history. For example, you may notice that your payments have been increasing or decreasing over time, or that there are certain months when your payments are consistently higher or lower.

To forecast future payments, you can use the data from your report to create a budget or financial projection. This will help you anticipate upcoming payments and plan accordingly. You can also use the report to identify areas where you may be able to save money on your mortgage, such as by refinancing or making extra payments.

In addition to generating reports, QuickBooks also offers a variety of tools and features that can help you manage your mortgage more effectively. For example, you can set up automatic payments, track your amortization schedule, and monitor your equity. By leveraging these tools, you can take control of your mortgage and make informed financial decisions.

Exploring Mortgage Records: A Comprehensive Research Guide

You may want to see also

Frequently asked questions

To set up a mortgage account in QuickBooks, go to the "Lists" menu and select "Chart of Accounts." Then, right-click anywhere in the chart and choose "New Account." Select "Loan" as the account type, and then choose "Mortgage" as the detail type. Enter the necessary information, such as the account name, description, and initial balance.

To record mortgage payments in QuickBooks, go to the "Banking" menu and select "Write Checks." Choose the mortgage account from the "Pay to the Order of" dropdown, enter the payment amount, and select the appropriate expense account for the interest portion of the payment. Click "Save & Close" to record the transaction.

To track mortgage interest in QuickBooks, you can create a separate expense account for mortgage interest. When recording mortgage payments, select this account for the interest portion of the payment. This will allow you to easily track and report on mortgage interest expenses.

QuickBooks does not have a built-in feature to generate a mortgage amortization schedule. However, you can create a custom report to track the principal and interest portions of each payment. To do this, go to the "Reports" menu and select "Custom Report." Choose the appropriate fields, such as date, amount, and account, and filter the report to only include mortgage payments. Then, you can export the report to Excel and create an amortization schedule using a spreadsheet template.