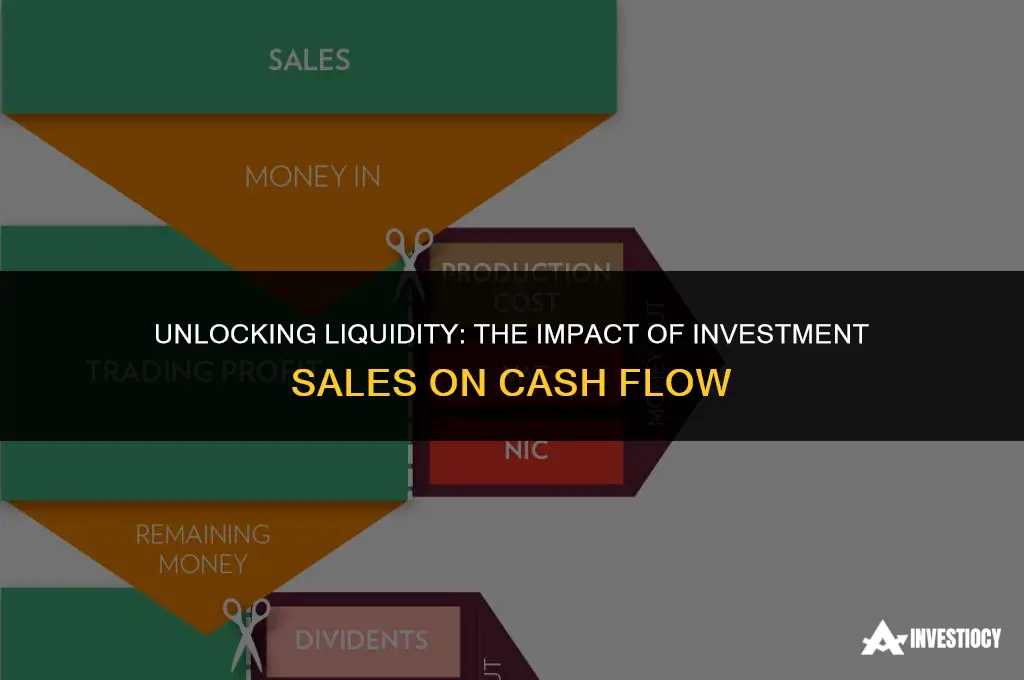

The sale of investments can indeed impact cash flow, but the nature of this impact depends on several factors. When an investment is sold, the proceeds from the sale can increase the cash balance, thereby enhancing liquidity. However, the timing and method of the sale, as well as the type of investment, play crucial roles in determining the actual cash flow implications. For instance, selling stocks or bonds typically results in immediate cash inflow, whereas selling real estate or other illiquid assets might involve a longer process and potentially delayed cash receipt. Additionally, the sale of investments might trigger capital gains taxes, which could reduce the net cash flow. Understanding these dynamics is essential for investors and financial managers to make informed decisions about when and how to sell investments to optimize cash flow.

Explore related products

$168.5 $179.95

$16.95 $24.95

What You'll Learn

- Types of Investments: Stocks, bonds, mutual funds, real estate, and other investment vehicles

- Capital Gains: Profits from selling investments at a higher price than the original purchase price

- Dividends and Interest: Regular income generated from investments, such as stock dividends or bond interest

- Tax Implications: Understanding how capital gains and investment income are taxed, including tax rates and deductions

- Investment Strategies: Approaches to selling investments, such as value investing, growth investing, or income investing

![]()

Types of Investments: Stocks, bonds, mutual funds, real estate, and other investment vehicles

The sale of investments can indeed generate cash flow, but the nature and timing of this cash flow vary significantly depending on the type of investment. For instance, stocks and bonds are typically liquid assets that can be sold quickly on the open market, providing immediate cash flow. However, the sale of these securities may also incur transaction costs and potentially trigger capital gains taxes, which can reduce the net cash flow.

Mutual funds offer a diversified portfolio of stocks, bonds, or other securities, and their sale can also generate cash flow. However, mutual funds may have specific redemption periods or fees associated with early withdrawals, which can impact the timing and amount of cash flow received. Additionally, the performance of mutual funds can fluctuate based on market conditions, affecting the overall cash flow from their sale.

Real estate investments, on the other hand, are generally considered illiquid assets. Selling a property can take time, and the process involves various costs such as real estate agent fees, closing costs, and potentially capital gains taxes. While real estate can provide substantial cash flow through rental income and property appreciation, the sale of a property may not offer immediate liquidity.

Other investment vehicles, such as private equity, hedge funds, or commodities, have their own unique characteristics that influence cash flow. Private equity investments, for example, are typically long-term and illiquid, with cash flow generated through periodic distributions or the eventual sale of the investment. Hedge funds may offer more liquidity than private equity but often come with high fees and minimum investment requirements. Commodities, such as gold or oil, can be traded on the open market, providing immediate cash flow, but their prices can be highly volatile.

In conclusion, while the sale of investments can generate cash flow, the specific type of investment, its liquidity, associated costs, and market conditions all play crucial roles in determining the timing and amount of cash flow received. Investors should carefully consider these factors when planning their investment strategies and cash flow needs.

Smart Strategies: Where to Invest Your Extra Cash Wisely

You may want to see also

Explore related products

![]()

Capital Gains: Profits from selling investments at a higher price than the original purchase price

Capital gains represent a crucial aspect of investment returns, occurring when an investment is sold for a higher price than its original purchase price. This concept is fundamental in understanding how investments can generate cash flow over time. When an investor sells an asset, such as a stock, bond, or real estate, for a profit, that profit is classified as a capital gain. This gain is calculated by subtracting the cost basis (the original purchase price plus any associated costs) from the sale price.

Capital gains can be categorized into two main types: short-term and long-term. Short-term capital gains occur when an investment is held for one year or less before being sold, while long-term capital gains result from investments held for more than one year. The distinction between these two types is significant because it affects how the gains are taxed. Typically, short-term capital gains are taxed at the investor's ordinary income tax rate, which can be higher than the tax rate applied to long-term capital gains.

The process of realizing capital gains involves several steps. First, the investor must identify the asset to be sold and determine its current market value. Next, they need to consider the potential tax implications of the sale, including any capital gains taxes that may be owed. Once the decision to sell is made, the investor executes the sale through a brokerage firm or other appropriate channels. After the sale is completed, the investor receives the proceeds, which can then be reinvested or used for other purposes.

One common strategy for managing capital gains is to reinvest the proceeds into new investments, potentially deferring taxes through a process known as a 1031 exchange in the case of real estate. Another strategy is to harvest losses, where an investor sells investments that have decreased in value to offset gains from other investments, thereby reducing their overall tax liability.

In summary, capital gains are a key component of investment returns, representing the profits realized when an investment is sold for more than its original purchase price. Understanding the nuances of capital gains, including the distinction between short-term and long-term gains, the process of realizing gains, and strategies for managing them, is essential for investors seeking to maximize their returns and minimize their tax obligations.

Maximize Your Returns: Cashing Out Investments on Cash App

You may want to see also

Explore related products

![]()

Dividends and Interest: Regular income generated from investments, such as stock dividends or bond interest

Dividends and interest represent a crucial aspect of investment income, providing regular cash flow to investors. This income is generated through various mechanisms, such as stock dividends or bond interest. Stock dividends are payments made by corporations to their shareholders, usually as a distribution of profits. Bond interest, on the other hand, is the return earned by investors who lend money to governments or corporations through the purchase of bonds.

One key advantage of dividends and interest is their ability to provide a steady stream of income, which can be particularly valuable for retirees or those seeking to supplement their primary income. This regular cash flow can help cover living expenses, reinvested to grow the investment portfolio further, or used to achieve specific financial goals.

Investors should consider the tax implications of dividends and interest income. In many jurisdictions, dividends and interest are subject to taxation, which can impact the overall return on investment. Understanding the tax laws and regulations related to investment income can help investors make informed decisions and optimize their portfolio for tax efficiency.

Another important consideration is the reinvestment of dividends and interest. By reinvesting this income, investors can take advantage of compounding returns, which can significantly grow their investment portfolio over time. This strategy can be particularly effective for long-term investors who are willing to let their investments grow and compound over several years or even decades.

In conclusion, dividends and interest play a vital role in generating regular income from investments. By understanding the mechanisms behind these income streams, considering the tax implications, and reinvesting wisely, investors can maximize the benefits of dividends and interest to achieve their financial goals.

Unlocking Financial Growth: Understanding Cash Investments

You may want to see also

Explore related products

![]()

Tax Implications: Understanding how capital gains and investment income are taxed, including tax rates and deductions

Understanding the tax implications of selling investments is crucial for effective financial planning. Capital gains and investment income are subject to different tax rates and rules, which can significantly impact your overall tax liability. When you sell an investment, such as stocks, bonds, or real estate, the profit you make is considered a capital gain. The tax rate on capital gains varies depending on your income level and the length of time you held the investment. Short-term capital gains, from investments held for less than a year, are taxed at your ordinary income tax rate, which can be as high as 37% for high-income earners. In contrast, long-term capital gains, from investments held for more than a year, are taxed at a lower rate, with the highest rate being 20% for most taxpayers.

Investment income, such as dividends and interest, is also subject to taxation. Dividends from stocks and mutual funds are taxed at different rates depending on whether they are qualified or non-qualified. Qualified dividends are taxed at the same rate as long-term capital gains, while non-qualified dividends are taxed at your ordinary income tax rate. Interest income from bonds, CDs, and other fixed-income investments is generally taxed at your ordinary income tax rate. However, there are some exceptions, such as tax-exempt municipal bonds, which are not subject to federal income tax.

One way to reduce your tax liability on investment income is to take advantage of tax deductions and credits. For example, you may be able to deduct investment expenses, such as brokerage fees and investment advisory fees, on your tax return. Additionally, you may be eligible for the foreign tax credit if you invest in foreign stocks or bonds that pay dividends or interest. This credit allows you to offset some of the taxes you pay to foreign governments.

Another important consideration is the impact of taxes on your investment strategy. For example, you may want to consider holding investments for longer periods to qualify for the lower long-term capital gains tax rate. You may also want to invest in tax-efficient vehicles, such as index funds or exchange-traded funds (ETFs), which tend to have lower turnover rates and therefore generate fewer capital gains. Finally, you may want to consider using tax-loss harvesting, a strategy that involves selling investments that have lost value to offset gains from other investments.

In conclusion, understanding the tax implications of selling investments is essential for maximizing your after-tax returns. By knowing the tax rates and rules that apply to capital gains and investment income, you can make informed decisions about your investment strategy and take advantage of tax deductions and credits to reduce your tax liability.

Unlocking Financial Insights: Understanding Cash Flow from Investing Activities

You may want to see also

Explore related products

$0.99 $9.99

![]()

Investment Strategies: Approaches to selling investments, such as value investing, growth investing, or income investing

Value investing is an investment paradigm that involves buying securities that appear underpriced by some form of fundamental analysis. Given the aim of value investing is to profit from the market's overreaction to cyclical events, the strategy often involves selling investments when they reach a price that reflects their intrinsic value, which may be higher than their purchase price. This approach requires patience and a deep understanding of market dynamics, as well as the ability to identify undervalued assets.

Growth investing, on the other hand, focuses on companies that are expected to grow at a faster rate than the market average. Investors in this category typically sell their investments when the growth potential is realized, or when the market valuation of the company aligns with its anticipated future performance. This strategy can be riskier than value investing, as it often involves investing in companies with high price-to-earnings ratios, which can be volatile.

Income investing is a strategy geared towards generating a steady income stream from investments. This can be achieved through investing in dividend-paying stocks, bonds, or other income-generating securities. The sale of investments in this category is often triggered by a need to rebalance the portfolio, adjust to changing market conditions, or meet specific income requirements. Income investing is generally considered a more conservative approach, as it prioritizes regular income over capital appreciation.

Each of these strategies has its own unique approach to selling investments, and the decision to sell is influenced by a variety of factors including market conditions, investment goals, and risk tolerance. Understanding these strategies can help investors make informed decisions about when to sell their investments to maximize returns and minimize risks.

Smart Investing on Cash App: Your Guide to Financial Growth

You may want to see also

Frequently asked questions

The cash flow from the sale of investments refers to the money received by an individual or organization when they sell their investments, such as stocks, bonds, or real estate. This cash inflow is typically considered a positive event in financial planning and can be used to fund other projects, pay off debts, or reinvest in other opportunities.

The sale of investments can significantly impact cash flow by providing a lump sum of money that can be used to improve liquidity, reduce debt, or fund new investments. However, it's essential to consider the potential tax implications and any fees associated with the sale, as these can affect the net cash flow.

Yes, there are often tax implications associated with the sale of investments. Depending on the type of investment and the jurisdiction, capital gains taxes may be applied to the profit made from the sale. It's crucial to consult with a tax professional to understand the specific tax implications and plan accordingly.

Some common reasons for selling investments include the need for liquidity, rebalancing a portfolio, taking advantage of market opportunities, paying off debts, funding major expenses, or retiring. The decision to sell investments should be based on a careful evaluation of financial goals and market conditions.

The cash flow from the sale of investments can be reinvested in various ways, such as purchasing new stocks, bonds, mutual funds, or real estate. It can also be used to fund a business venture, pay off high-interest debt, or build an emergency fund. The best reinvestment strategy will depend on an individual's financial goals, risk tolerance, and market conditions.