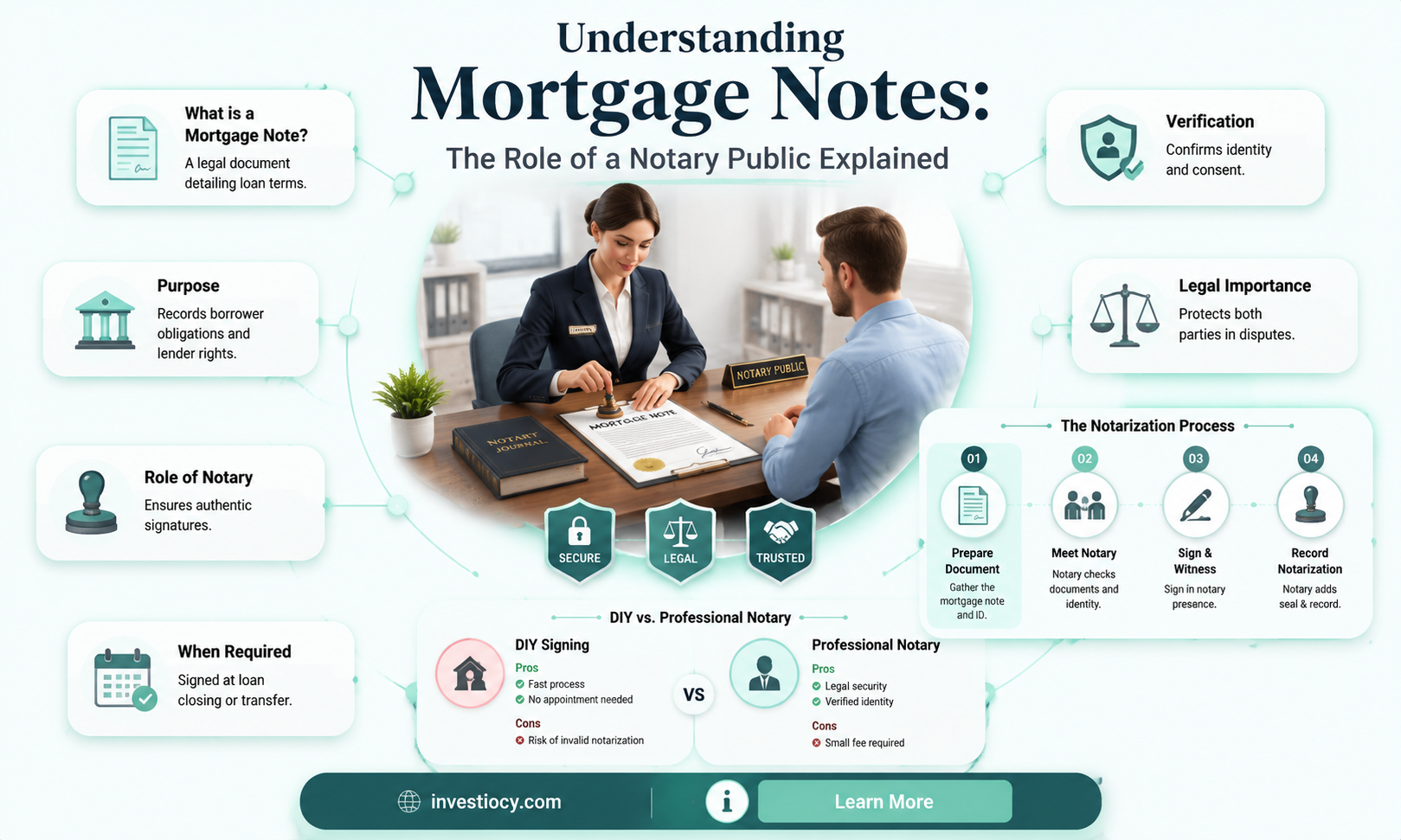

A notary public plays a crucial role in the legal process of document authentication, and one common question that arises is whether they are required to sign a mortgage note. In general, a notary public is not mandated to sign a mortgage note; their primary responsibility is to notarize the document, which involves verifying the identity of the signatories and ensuring that they are signing the document voluntarily and with full understanding of its contents. The notary's role is to provide an official seal or stamp and a signature that confirms the authenticity of the document, rather than to sign the mortgage note itself as a party to the agreement.

Explore related products

What You'll Learn

- Role of Notary Public: Explains the legal responsibilities and duties of a notary public in the mortgage process

- Signing Requirements: Details the specific conditions under which a notary public must sign a mortgage note

- Verification Process: Describes how notaries verify the identity and willingness of signatories in mortgage transactions

- Legal Implications: Discusses the potential legal consequences if a notary public fails to properly sign or verify a mortgage note

- State-Specific Regulations: Highlights variations in notary public requirements and regulations across different states

![]()

Role of Notary Public: Explains the legal responsibilities and duties of a notary public in the mortgage process

A notary public plays a crucial role in the mortgage process, ensuring the legality and authenticity of the documents involved. Their primary responsibility is to verify the identity of the parties signing the mortgage note and other related documents. This involves checking government-issued identification, confirming that the signatories are who they claim to be, and that they are signing the documents voluntarily and with full understanding of their contents.

In addition to verifying identities, a notary public is responsible for witnessing the signing of the mortgage note. This means they must be physically present when the borrower signs the document, observe the signing, and then sign their own name on the document to certify that they have witnessed the event. Their signature serves as a legal acknowledgment that the document has been signed in their presence and that they have verified the identity of the signatory.

Notaries public also have the duty to ensure that the mortgage note and other documents are complete and accurate. They must review the documents for any errors or omissions, and if they find any, they are obligated to inform the parties involved and refuse to notarize the documents until the issues are corrected. This helps to prevent legal problems down the line and ensures that all parties are entering into the mortgage agreement with a clear understanding of the terms.

Furthermore, a notary public is responsible for maintaining a record of the notarial act. This typically includes keeping a journal or log that details the date, time, and location of the notarization, as well as the names of the parties involved and the type of document notarized. These records are important for tracking the notarial act and can be used as evidence in legal proceedings if necessary.

In summary, the role of a notary public in the mortgage process is multifaceted and critical to ensuring the legality and enforceability of the mortgage note. They are responsible for verifying identities, witnessing signatures, ensuring document accuracy, and maintaining records of their notarial acts. Without the involvement of a notary public, the mortgage process would lack the necessary legal safeguards to protect all parties involved.

Understanding Navy Federal Mortgage Pre-Qualification: Does It Go to Underwriting?

You may want to see also

Explore related products

![]()

Signing Requirements: Details the specific conditions under which a notary public must sign a mortgage note

A notary public's signature on a mortgage note is not a mere formality; it is a crucial step in the legal process that ensures the document's authenticity and enforceability. The specific conditions under which a notary public must sign a mortgage note are governed by state laws and regulations, which vary slightly from one jurisdiction to another. However, there are certain universal requirements that must be met in order for a notary public to legally affix their signature to such a document.

Firstly, the notary public must verify the identity of the signer(s) of the mortgage note. This typically involves checking government-issued identification, such as a driver's license or passport, to ensure that the person signing the document is who they claim to be. In some cases, additional identification methods, such as fingerprinting or facial recognition, may be required.

Secondly, the notary public must ensure that the signer(s) are signing the document voluntarily and without duress. This means that the notary must observe the signing process and ask the signer(s) if they are signing of their own free will, without any coercion or pressure from another party. If the notary has any reason to believe that the signer(s) are being forced to sign the document, they are legally obligated to refuse to notarize it.

Thirdly, the notary public must verify that the signer(s) have the legal capacity to sign the mortgage note. This means that the notary must ensure that the signer(s) are of legal age, are not under any legal disability (such as bankruptcy or mental incompetence), and have the authority to enter into the mortgage agreement.

Finally, the notary public must ensure that the mortgage note is complete and accurate. This involves reviewing the document for any missing information or errors, and verifying that all necessary signatures and initials are present. Once the notary has confirmed that all of these conditions have been met, they may legally sign and seal the mortgage note, thereby notarizing it and giving it legal effect.

Understanding NACA Mortgages: Is PMI Included?

You may want to see also

Explore related products

![]()

Verification Process: Describes how notaries verify the identity and willingness of signatories in mortgage transactions

In the realm of mortgage transactions, the role of a notary public is pivotal in ensuring the authenticity and legality of the documents involved. The verification process undertaken by notaries is a critical step that safeguards the interests of all parties engaged in the transaction. This process is multifaceted, involving several key steps that collectively validate the identity and willingness of the signatories.

Firstly, notaries must verify the identity of the signatories. This typically involves examining government-issued identification documents such as driver's licenses, passports, or state IDs. The notary must ensure that the identification presented is current, valid, and matches the name of the signatory on the mortgage document. In some cases, additional identification methods may be employed, such as biometric verification or witness testimony, to further substantiate the identity of the parties involved.

Following identity verification, the notary must ascertain the willingness of the signatories to enter into the mortgage agreement. This step is crucial as it ensures that the signatories are fully aware of the terms and conditions of the mortgage and are entering into the agreement of their own volition. The notary may ask the signatories questions about the nature of the transaction, the terms of the mortgage, and whether they have been coerced or unduly influenced in any way. This verbal confirmation is often supplemented by the execution of a notarized affidavit or acknowledgment, in which the signatories formally declare their willingness to proceed with the transaction.

The notary's verification process also includes a review of the mortgage documents themselves. This review is intended to ensure that the documents are complete, accurate, and comply with all relevant legal requirements. The notary must check for any discrepancies or inconsistencies in the documents and confirm that all necessary disclosures have been made. This step helps to prevent fraud and ensures that the mortgage agreement is legally binding and enforceable.

Once the verification process is complete, the notary will execute the notarization by signing and sealing the mortgage documents. This act serves as a formal certification that the identity and willingness of the signatories have been verified and that the documents are authentic and legally valid. The notary's signature and seal are essential elements of the mortgage transaction, as they provide a layer of legal protection and certainty for all parties involved.

In conclusion, the verification process conducted by notaries in mortgage transactions is a comprehensive and meticulous procedure that plays a vital role in maintaining the integrity and legality of the transaction. By verifying the identity and willingness of the signatories, reviewing the mortgage documents, and executing the notarization, notaries help to ensure that mortgage agreements are entered into fairly and are legally binding.

Understanding Mortgage Agreements: Non-Borrowing Spouse's Signature Requirements

You may want to see also

Explore related products

![]()

Legal Implications: Discusses the potential legal consequences if a notary public fails to properly sign or verify a mortgage note

If a notary public fails to properly sign or verify a mortgage note, it can lead to serious legal implications. One of the primary consequences is the potential invalidation of the mortgage document itself. Without a proper notarization, the mortgage may not be legally binding, which could result in disputes over the ownership of the property or the enforceability of the loan terms. This could lead to lengthy and costly legal battles, potentially resulting in financial losses for both the lender and the borrower.

Furthermore, a notary public who fails to properly perform their duties may face disciplinary action from their state licensing board. This could include fines, suspension, or even revocation of their notary commission. In some cases, if the notary's actions are deemed to be fraudulent or intentional, they may also face criminal charges.

In addition to the direct consequences for the notary, there can also be broader implications for the real estate and lending industries. If lenders lose confidence in the notarization process, they may become more hesitant to issue loans, which could lead to a tightening of credit and a decrease in real estate transactions. This, in turn, could have a ripple effect on the overall economy.

To avoid these potential legal consequences, it is crucial for notary publics to carefully follow all applicable laws and regulations when notarizing mortgage documents. This includes verifying the identity of the signatories, ensuring that they are signing the document voluntarily and with full understanding of its contents, and properly executing the notarization in accordance with state law.

In conclusion, the legal implications of a notary public failing to properly sign or verify a mortgage note can be severe and far-reaching. It is essential for notaries to take their responsibilities seriously and to adhere to the highest standards of professionalism and integrity in order to maintain the trust and confidence of the public and the industries they serve.

Understanding Multiple Indebtedness Mortgages: Maturity Insights

You may want to see also

Explore related products

![]()

State-Specific Regulations: Highlights variations in notary public requirements and regulations across different states

Notary public regulations vary significantly from state to state, impacting the process of notarizing documents such as mortgage notes. For instance, some states require notaries to be attorneys, while others do not. This fundamental difference affects the level of legal advice a notary can provide and the types of documents they are qualified to notarize.

In states like Florida, notaries are prohibited from providing legal advice or preparing legal documents, including mortgage notes. They are strictly limited to witnessing signatures and verifying identities. Conversely, states such as Louisiana allow notaries to prepare and notarize certain legal documents, including mortgage notes, as long as they are not acting as an attorney for either party.

Another variation lies in the requirements for notary education and training. States like California mandate a specific number of hours of notary education, while others, such as Texas, do not have such stringent requirements. This disparity can influence the competency and preparedness of notaries when handling complex documents like mortgage notes.

Furthermore, the fees charged by notaries for their services can differ widely between states. Some states, like New York, have fixed fees for notary services, while others allow notaries to set their own rates. This can impact the cost of notarizing a mortgage note and may influence the choice of notary for lenders and borrowers.

In conclusion, the role and responsibilities of a notary public in the context of mortgage notes are subject to state-specific regulations. These variations can affect the legal authority, education, and fees associated with notary services, highlighting the importance of understanding and complying with state laws when dealing with mortgage transactions.

Frequently asked questions

Yes, a notary public must sign a mortgage note to notarize it, which involves verifying the identity of the signer and witnessing the signing of the document.

A notary public's role in the mortgage process is to act as an impartial witness, verifying the identity of the parties involved and ensuring that they are signing the mortgage note voluntarily and with full understanding of the terms.

Yes, a notary public can refuse to notarize a mortgage note if they have reasonable grounds to believe that the document is fraudulent, the signer is not who they claim to be, or the signer is being coerced into signing.

If a notary public does not sign a mortgage note, the document may not be legally binding, and the mortgage transaction could be delayed or invalidated.

Yes, there are legal requirements for a notary public when notarizing a mortgage note, which include verifying the signer's identity, witnessing the signing, and completing a notarial certificate that includes their signature and seal.