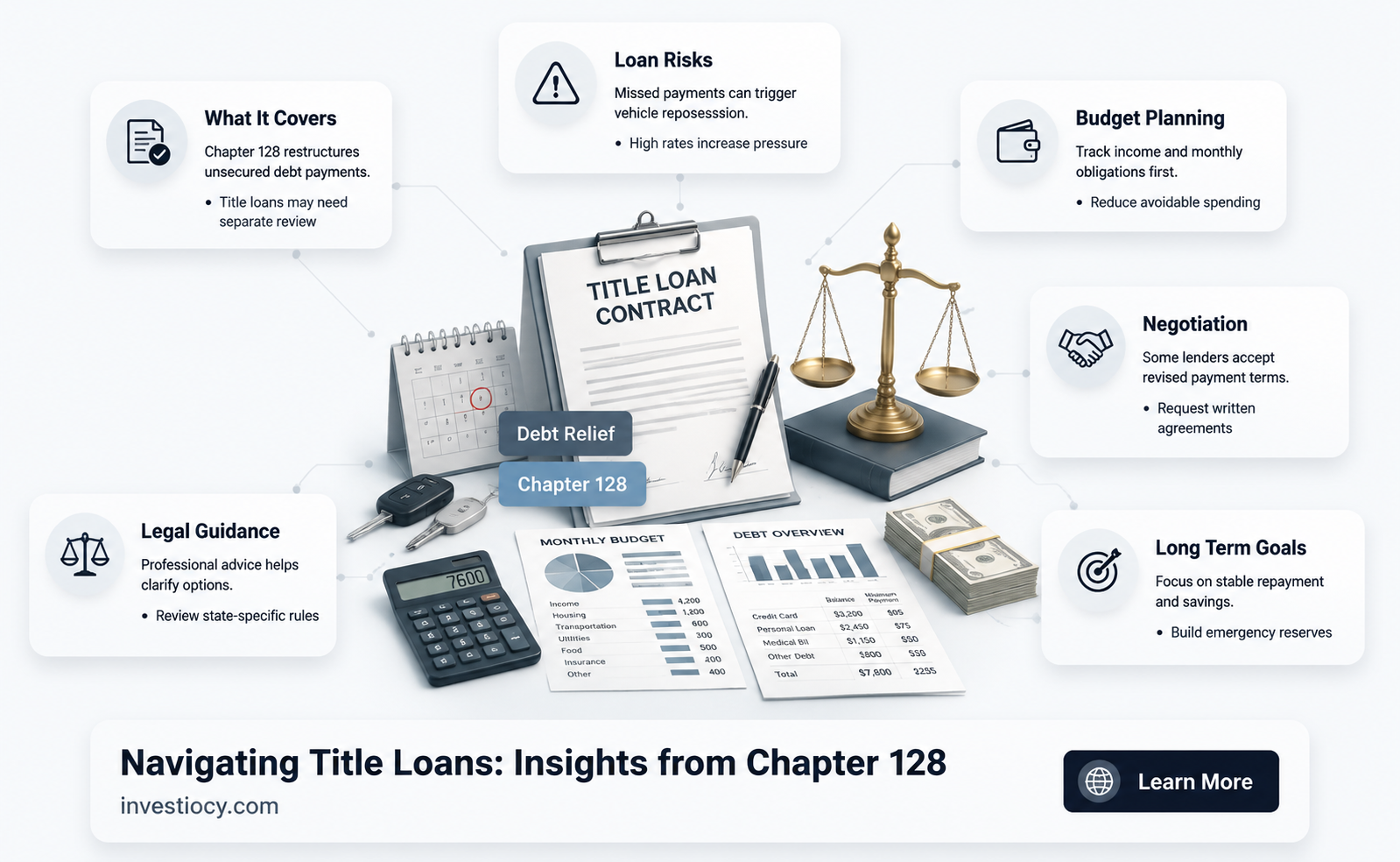

Chapter 128 of the Wisconsin Statutes is a powerful tool designed to help individuals struggling with debt, including title loans. This chapter outlines a debt adjustment program that allows debtors to repay their creditors over time under the supervision of the court. By filing for Chapter 128, individuals can halt creditor actions, such as repossession of a vehicle in the case of a title loan, and work towards a manageable repayment plan. This legal framework provides a structured approach to debt resolution, offering a lifeline to those overwhelmed by financial obligations and facing the loss of valuable assets.

Explore related products

$6.99

What You'll Learn

- Understanding Chapter 128: Overview of Chapter 128 and its relevance to title loans

- Eligibility for Title Loans: Criteria that must be met to qualify for a title loan under Chapter 128

- Benefits of Chapter 128: Advantages of using Chapter 128 for managing title loans

- Repayment Plans: Structured repayment plans offered under Chapter 128 for title loans

- Legal Protections: Legal safeguards provided by Chapter 128 to protect consumers with title loans

![]()

Understanding Chapter 128: Overview of Chapter 128 and its relevance to title loans

Chapter 128 of the legal code is a crucial section that outlines the regulations and guidelines for title loans. Title loans are a type of secured loan where borrowers use their vehicle's title as collateral. Understanding Chapter 128 is essential for both lenders and borrowers to ensure compliance with the law and to make informed decisions.

One of the key aspects of Chapter 128 is its focus on protecting consumers from predatory lending practices. The chapter imposes strict regulations on interest rates, fees, and repayment terms to prevent borrowers from being trapped in a cycle of debt. For instance, it caps the maximum interest rate that can be charged on a title loan and mandates that lenders provide clear and concise disclosure of all loan terms.

Moreover, Chapter 128 requires lenders to assess the borrower's ability to repay the loan before extending credit. This is to ensure that borrowers are not taking on more debt than they can handle, which can lead to financial distress and potential loss of their vehicle. Lenders must also provide borrowers with a written contract that outlines all the terms and conditions of the loan, including the repayment schedule and any penalties for late payments.

In addition to these consumer protections, Chapter 128 also sets out the legal framework for the enforcement of title loans. It establishes the procedures that lenders must follow to repossess a vehicle if the borrower defaults on the loan. This includes providing the borrower with notice of the default and an opportunity to cure the default before the vehicle can be repossessed.

Overall, Chapter 128 plays a vital role in regulating the title loan industry and protecting consumers from unfair and deceptive practices. By understanding the provisions of this chapter, borrowers can make more informed decisions about whether a title loan is right for them, and lenders can ensure that they are operating within the legal framework.

Exploring Chapel Hill Library's Wi-Fi Loan Services: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Eligibility for Title Loans: Criteria that must be met to qualify for a title loan under Chapter 128

To qualify for a title loan under Chapter 128, several specific eligibility criteria must be met. Firstly, the borrower must own a vehicle outright, with no outstanding liens or loans against it. This is because the vehicle's title is used as collateral for the loan, and any existing claims on the title could complicate the lending process. Additionally, the vehicle must be in good working condition and have a certain minimum value to be considered for a title loan.

Secondly, the borrower must be at least 18 years old and have a valid government-issued ID, such as a driver's license or passport. This is to ensure that the borrower is legally capable of entering into a loan agreement and can be identified by the lender. Furthermore, the borrower must provide proof of residency, typically in the form of a utility bill or lease agreement, to demonstrate that they have a stable living situation.

Thirdly, the borrower must have a source of income to repay the loan. This income can come from employment, self-employment, disability benefits, or other sources, but it must be sufficient to cover the loan payments. Lenders will often require proof of income, such as pay stubs or bank statements, to verify the borrower's ability to repay.

Fourthly, the borrower must not be in the process of filing for bankruptcy or have an outstanding bankruptcy case. This is because title loans are typically secured debts, and bankruptcy could affect the lender's ability to recover the loan amount if the borrower defaults. Additionally, the borrower must not have a history of defaulting on title loans or other secured debts, as this could indicate a higher risk of defaulting on the current loan.

Finally, the borrower must agree to the terms and conditions of the loan, including the interest rate, repayment schedule, and any fees associated with the loan. It is important for the borrower to carefully review these terms and ensure they understand their obligations before signing the loan agreement.

In summary, to qualify for a title loan under Chapter 128, a borrower must own a vehicle outright, be at least 18 years old with a valid ID and proof of residency, have a sufficient source of income, not be in the process of filing for bankruptcy or have a history of defaulting on secured debts, and agree to the terms and conditions of the loan. Meeting these criteria will help ensure that the borrower is eligible for a title loan and can successfully repay it.

Exploring Centrelink's Role in Bond Loans: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Benefits of Chapter 128: Advantages of using Chapter 128 for managing title loans

Chapter 128 offers several distinct advantages for individuals seeking to manage title loans. One of the primary benefits is the ability to consolidate multiple debts into a single, more manageable payment plan. This can significantly reduce the stress and complexity of dealing with various creditors and interest rates. By consolidating debts, individuals can often lower their overall monthly payments, making it easier to stay on top of their financial obligations.

Another key advantage of Chapter 128 is the protection it provides against creditor actions. Once a debtor files for Chapter 128, an automatic stay is issued, which prevents creditors from pursuing collection activities, including repossession of the vehicle. This can be particularly beneficial for individuals who are at risk of losing their car due to missed payments on a title loan. The automatic stay gives debtors a breathing room to reorganize their finances and propose a repayment plan that is more sustainable.

Furthermore, Chapter 128 allows debtors to potentially reduce the principal amount owed on their title loans. Through the bankruptcy process, debtors can challenge the validity of certain debts or negotiate with creditors to settle for a lower amount. This can result in significant savings and make it more feasible for debtors to repay their loans in full.

Additionally, Chapter 128 provides a structured framework for debtors to address their financial issues comprehensively. It requires debtors to complete a credit counseling course and to propose a repayment plan that is approved by the bankruptcy court. This ensures that debtors are making informed decisions about their finances and are committed to a realistic plan for repaying their debts.

In summary, Chapter 128 offers several benefits for managing title loans, including debt consolidation, protection from creditor actions, potential reduction of principal amounts, and a structured approach to financial reorganization. These advantages can make Chapter 128 a valuable tool for individuals struggling with title loan debt.

The Impact of Name Changes on Loan Obligations: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Repayment Plans: Structured repayment plans offered under Chapter 128 for title loans

Under Chapter 128, structured repayment plans are designed to assist individuals who are struggling with title loans. These plans offer a systematic approach to paying off the debt, typically over a longer period than the original loan term. This can help reduce the monthly payment amount, making it more manageable for the debtor.

One of the key benefits of these repayment plans is that they often include a fixed interest rate, which can be lower than the rate on the original title loan. This not only makes the payments more predictable but can also result in significant savings over the life of the repayment plan. Additionally, these plans may waive late fees or other penalties that can accumulate on unpaid title loans, further reducing the overall cost of the debt.

To qualify for a Chapter 128 repayment plan, debtors must meet certain eligibility criteria. This typically includes demonstrating a steady income and the ability to make regular payments. The court will also consider the debtor's overall financial situation, including other debts and expenses, to ensure that the repayment plan is feasible and sustainable.

Once approved, the repayment plan will be overseen by a trustee appointed by the court. The trustee will be responsible for collecting payments from the debtor and distributing them to the creditors. This provides an additional layer of protection for the debtor, as it ensures that payments are made in a timely and orderly manner.

In conclusion, structured repayment plans under Chapter 128 can be a valuable tool for individuals struggling with title loans. By offering a predictable and manageable way to pay off the debt, these plans can help debtors avoid the pitfalls of high-interest loans and get back on track financially.

Exploring Cashfloat: A Comprehensive Guide to US Loan Services

You may want to see also

Explore related products

![]()

Legal Protections: Legal safeguards provided by Chapter 128 to protect consumers with title loans

Chapter 128 of the legal code provides a robust framework of protections for consumers who have taken out title loans. One of the key legal safeguards is the requirement for lenders to disclose all terms and conditions of the loan agreement in a clear and conspicuous manner. This ensures that borrowers are fully aware of the interest rates, repayment terms, and any potential fees associated with the loan. Additionally, Chapter 128 mandates that lenders must provide borrowers with a written copy of the loan agreement, which serves as a tangible record of the transaction and can be used for future reference or in the event of a dispute.

Another important protection afforded by Chapter 128 is the prohibition on lenders from engaging in unfair or deceptive practices. This includes making false or misleading statements about the loan terms, charging excessive fees, or using aggressive collection tactics. Lenders who violate these provisions may be subject to legal action, including fines and restitution to affected borrowers. Furthermore, Chapter 128 establishes a cap on the maximum interest rate that can be charged on title loans, which helps to prevent borrowers from being trapped in a cycle of debt with exorbitant interest charges.

In addition to these protections, Chapter 128 also provides borrowers with the right to rescind the loan agreement within a certain timeframe if they find that the terms are not favorable or if they have been misled by the lender. This gives borrowers an opportunity to walk away from the loan without incurring any penalties or fees, provided they return the loan proceeds to the lender. Moreover, Chapter 128 requires lenders to maintain accurate records of all loan transactions, which can be audited by regulatory authorities to ensure compliance with the law.

Overall, the legal protections provided by Chapter 128 are designed to safeguard consumers from predatory lending practices and ensure that title loans are offered in a fair and transparent manner. By understanding these protections, borrowers can make informed decisions about whether to take out a title loan and can take steps to protect themselves from potential abuses by lenders.

Exploring Cashland's Loan Options: Installment Loans and More

You may want to see also

Frequently asked questions

Chapter 128 is a section of the Wisconsin Consumer Credit Code that provides protections and regulations for consumer credit transactions, including title loans. It outlines the requirements for lenders and the rights of borrowers.

Yes, Chapter 128 offers several protections for title loan borrowers, such as limiting the interest rate, requiring clear disclosure of loan terms, and providing a process for borrowers to refinance or reinstate their loans if they default.

Chapter 128 caps the interest rate on title loans at 36% APR, which helps to prevent borrowers from being charged excessive interest and fees.

Under Chapter 128, lenders are required to provide borrowers with a clear and concise disclosure of the loan terms, including the interest rate, fees, and repayment schedule. This helps borrowers to understand the terms of their loans and make informed decisions.

Chapter 128 provides a process for borrowers to refinance or reinstate their loans if they default. This helps to prevent borrowers from losing their vehicles and provides them with an opportunity to get back on track with their payments.