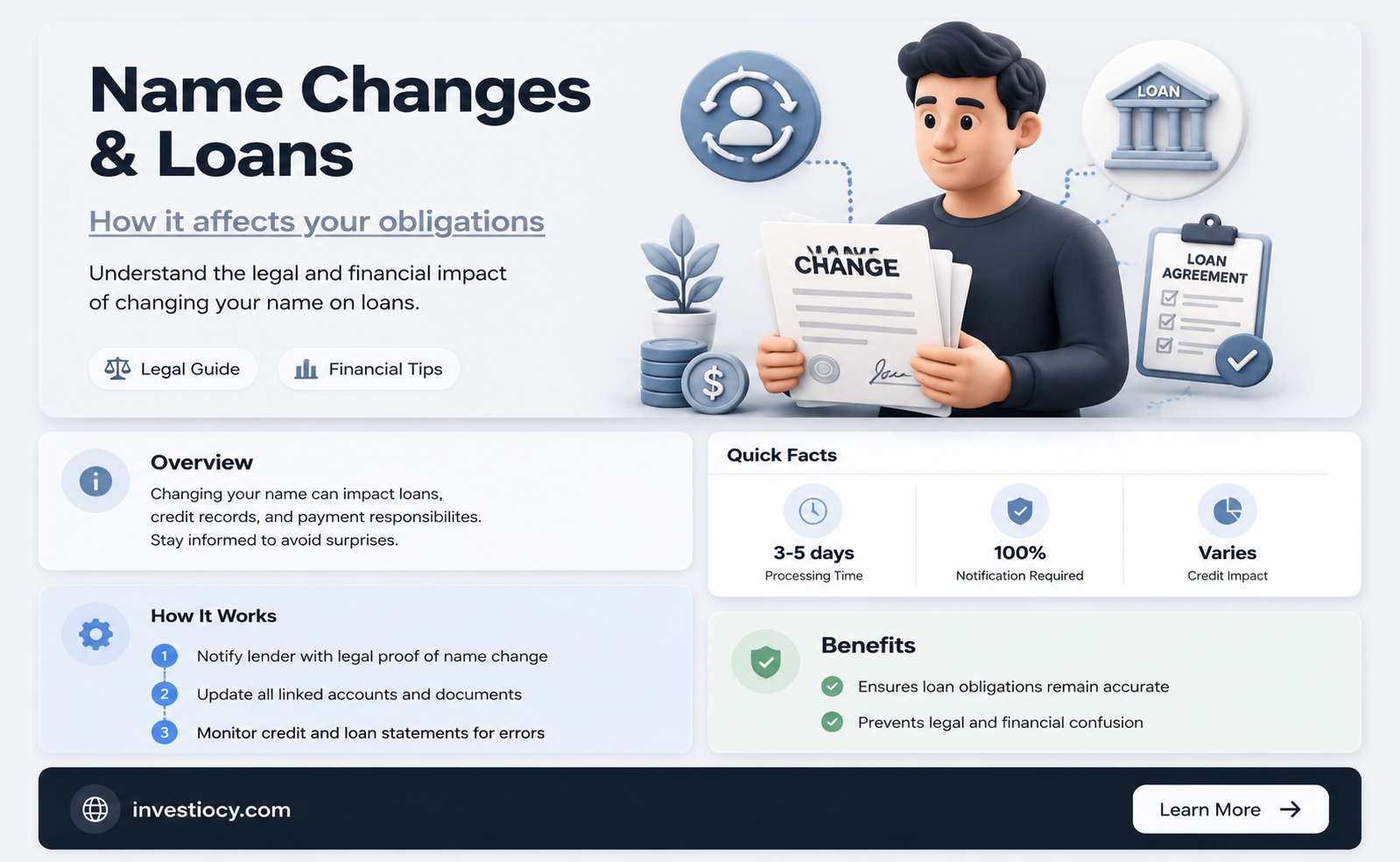

Changing your name can have various implications, especially when it comes to financial matters such as loans. One common question people ask is whether altering their name will affect their loan obligations. The answer is not straightforward and depends on several factors, including the type of loan, the lender's policies, and the legal requirements in your jurisdiction. Generally, changing your name does not automatically absolve you of your loan responsibilities. Lenders typically require you to notify them of any name changes and may ask for updated identification and documentation to reflect the change. This ensures that they can still contact you and enforce the loan agreement if necessary. However, it's essential to review your specific loan contract and consult with a legal or financial advisor to understand the exact implications of a name change on your loan obligations.

Explore related products

What You'll Learn

- Impact on Credit Score: Changing your name may affect your credit score, influencing loan eligibility

- Loan Agreement Terms: Review loan agreements to understand name change implications on loan obligations

- Legal Documentation: Ensure all legal documents, including deeds and titles, reflect the new name

- Notification of Lenders: Inform all lenders and financial institutions of the name change promptly

- Potential Fraud Concerns: Be aware of potential fraud risks associated with name changes and monitor credit reports

![]()

Impact on Credit Score: Changing your name may affect your credit score, influencing loan eligibility

Changing your name can have a significant impact on your credit score, which in turn affects your eligibility for loans. This is because credit scores are based on a variety of factors, including payment history, credit utilization, length of credit history, and new credit inquiries. When you change your name, it can disrupt the continuity of your credit history, making it more difficult for lenders to assess your creditworthiness.

One of the primary ways that changing your name can affect your credit score is by causing a mismatch between the information on your credit reports and the information that lenders use to evaluate your loan application. This mismatch can lead to errors on your credit report, which can lower your credit score. Additionally, if you have a history of late payments or other negative credit behaviors, changing your name may not necessarily erase these blemishes from your credit report. In fact, they may continue to haunt you, even under your new name.

Furthermore, changing your name can also affect your ability to obtain new credit. When you apply for a loan or credit card under a new name, lenders may not have enough information to make an informed decision about your creditworthiness. This can lead to higher interest rates, lower credit limits, or even outright denial of credit. In some cases, you may be required to provide additional documentation or information to prove your identity and credit history, which can be a time-consuming and frustrating process.

It's also worth noting that changing your name can have different impacts on your credit score depending on the reason for the change. For example, if you change your name due to marriage or divorce, the impact on your credit score may be less severe than if you change your name for other reasons, such as to avoid creditors or to start a new life. In any case, it's important to be aware of the potential consequences of changing your name on your credit score and to take steps to mitigate any negative impacts.

In conclusion, changing your name can have a significant impact on your credit score and your ability to obtain loans and credit. It's important to carefully consider the potential consequences of changing your name and to take steps to maintain your credit history and creditworthiness. This may include updating your credit reports, providing additional documentation to lenders, and being patient as you rebuild your credit history under your new name.

Exploring Centrelink's Loan Options: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Loan Agreement Terms: Review loan agreements to understand name change implications on loan obligations

Reviewing loan agreements is crucial when considering a name change, as it can have significant implications on your loan obligations. Loan agreements are legally binding contracts that outline the terms and conditions of the loan, including the borrower's responsibilities and the lender's rights. A name change may affect the lender's ability to identify and contact the borrower, potentially leading to complications in the loan repayment process.

To understand the implications of a name change on loan obligations, it's essential to carefully examine the loan agreement. Look for clauses that specify the borrower's name and address, as well as any requirements for notifying the lender of changes to personal information. Some loan agreements may include provisions that allow for name changes without affecting the loan terms, while others may require the borrower to provide additional documentation or undergo a formal process to update their information.

In cases where the loan agreement does not explicitly address name changes, it's advisable to contact the lender directly to inquire about their policies and procedures. This can help ensure that the lender is aware of the name change and can take any necessary steps to update their records. Failure to notify the lender of a name change may result in missed payments, late fees, or even default on the loan.

It's also important to consider the impact of a name change on other aspects of the loan, such as credit reporting and tax implications. A name change may affect the borrower's credit score, as credit reporting agencies may not immediately recognize the new name. This can lead to difficulties in obtaining future loans or credit. Additionally, a name change may have tax implications, as the borrower's new name may not match the name on their tax returns or other financial documents.

In conclusion, reviewing loan agreements and understanding the implications of a name change on loan obligations is a critical step in the name change process. By carefully examining the loan agreement, contacting the lender, and considering the broader financial implications, borrowers can ensure a smooth transition and avoid potential complications.

Exploring Cashfloat: A Comprehensive Guide to US Loan Services

You may want to see also

Explore related products

![]()

Legal Documentation: Ensure all legal documents, including deeds and titles, reflect the new name

After changing your name, it's crucial to update all legal documents to reflect this change. This includes deeds and titles, which are often overlooked but can cause significant issues if not properly amended. For instance, if you own property and your name on the deed does not match your new legal name, it can lead to complications in selling or refinancing the property. Similarly, if your name on a car title or other vehicle documents is outdated, it can create problems when trying to transfer ownership or obtain insurance.

To ensure a smooth transition, it's essential to follow a systematic approach to updating your legal documents. Start by obtaining certified copies of your birth certificate, marriage certificate, or court order approving the name change. These documents will serve as proof of your new legal name and are necessary for updating most official records. Next, create a comprehensive list of all legal documents that need to be updated, including deeds, titles, bank accounts, credit cards, and any other relevant paperwork.

When updating deeds and titles, it's important to work with a legal professional or a title company to ensure the process is done correctly. They can help you prepare the necessary paperwork, file it with the appropriate government agencies, and obtain new deeds or titles that reflect your updated name. This process may involve paying certain fees and providing proof of identity and ownership, so it's essential to be prepared and patient.

In addition to updating deeds and titles, don't forget to notify other relevant parties of your name change. This includes your employer, insurance companies, and any creditors or lenders you may have. By doing so, you can avoid potential issues with payroll, insurance coverage, and credit reporting. It's also a good idea to update your name on social media and other online platforms to maintain consistency and protect your identity.

In conclusion, updating legal documents after a name change is a critical step in ensuring a smooth transition and avoiding potential legal and financial issues. By following a systematic approach and working with legal professionals when necessary, you can successfully update all relevant documents and enjoy the benefits of your new name without any unnecessary complications.

Exploring Centrelink's Role in Bond Loans: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Notification of Lenders: Inform all lenders and financial institutions of the name change promptly

Promptly notifying all lenders and financial institutions of a name change is crucial to maintaining financial stability and ensuring that your credit history remains intact. This process involves more than just a simple phone call; it requires a structured approach to ensure that all necessary parties are informed and that your financial records are updated accordingly.

The first step in this process is to gather a comprehensive list of all your lenders and financial institutions. This includes banks, credit card companies, investment firms, and any other entities with which you have a financial relationship. Once you have this list, you should contact each institution individually to inform them of your name change. It is important to provide them with your new name, as well as any supporting documentation that may be required, such as a marriage certificate or a court order.

In addition to notifying your lenders, you should also update your credit reports with the three major credit bureaus: Equifax, Experian, and TransUnion. This will ensure that your credit history is accurately reflected under your new name and that you continue to benefit from your established creditworthiness.

Another important consideration is the potential impact of a name change on your loan agreements. While changing your name does not automatically disqualify you from your loans, it is essential to review your loan agreements to ensure that there are no clauses that could be triggered by a name change. In some cases, you may need to renegotiate your loan terms or provide additional documentation to confirm your identity and financial status.

Finally, it is important to be aware of any potential scams or fraudulent activities that could arise in the wake of a name change. Criminals may attempt to exploit the confusion surrounding a name change to steal your identity or access your financial accounts. Therefore, it is crucial to remain vigilant and to monitor your accounts closely for any suspicious activity.

In conclusion, notifying lenders and financial institutions of a name change is a critical step in maintaining financial stability and protecting your credit history. By following a structured approach and remaining vigilant, you can ensure a smooth transition and minimize any potential disruptions to your financial life.

Navigating Bankruptcy: Can Chapter 7 Discharge Your Student Loans?

You may want to see also

Explore related products

![]()

Potential Fraud Concerns: Be aware of potential fraud risks associated with name changes and monitor credit reports

Changing your name can have several implications, one of which is the potential for fraud. It's crucial to be aware of these risks and take proactive steps to protect yourself. One of the primary concerns is that a name change can make it easier for fraudulent activities to go unnoticed, especially if the change is not promptly reflected in all financial and credit records.

To mitigate these risks, it's essential to monitor your credit reports closely. This involves checking your reports from all three major credit bureaus—Equifax, Experian, and TransUnion—regularly to ensure that all accounts and inquiries are accurate and up-to-date. If you notice any discrepancies or suspicious activities, report them immediately to the relevant credit bureau and your financial institutions.

Another important step is to update all your financial accounts and credit cards with your new name as soon as possible. This includes notifying your bank, credit card companies, and any other financial service providers you use. By doing so, you can help prevent fraudulent use of your old name and ensure that all financial transactions are properly recorded under your new name.

Additionally, consider placing a fraud alert on your credit reports. This can be done by contacting one of the credit bureaus and requesting a fraud alert. Once in place, this alert will notify creditors to take extra steps to verify your identity before opening new accounts or making changes to existing ones.

Finally, be cautious when sharing your personal information, especially your new name and any associated documents, such as a new driver's license or passport. Only provide this information when necessary and to trusted sources. By being vigilant and taking these precautions, you can help protect yourself from potential fraud risks associated with a name change.

Exploring Loan Modification Options with Cenlar: A Comprehensive Guide

You may want to see also

Frequently asked questions

No, changing your name does not automatically remove you from a loan. You must notify the lender of your name change and provide necessary documentation to update their records.

After a name change, you should contact your lender directly to inform them of the change. They will likely require you to provide a copy of your marriage certificate, divorce decree, or court order documenting the name change. You may also need to fill out and submit a name change request form.

Changing your name itself does not affect your credit score. However, if you do not update your loan and credit card information with your new name, it could lead to missed payments or confusion, which might negatively impact your credit score. It's important to ensure all financial institutions have your correct name to avoid any issues.