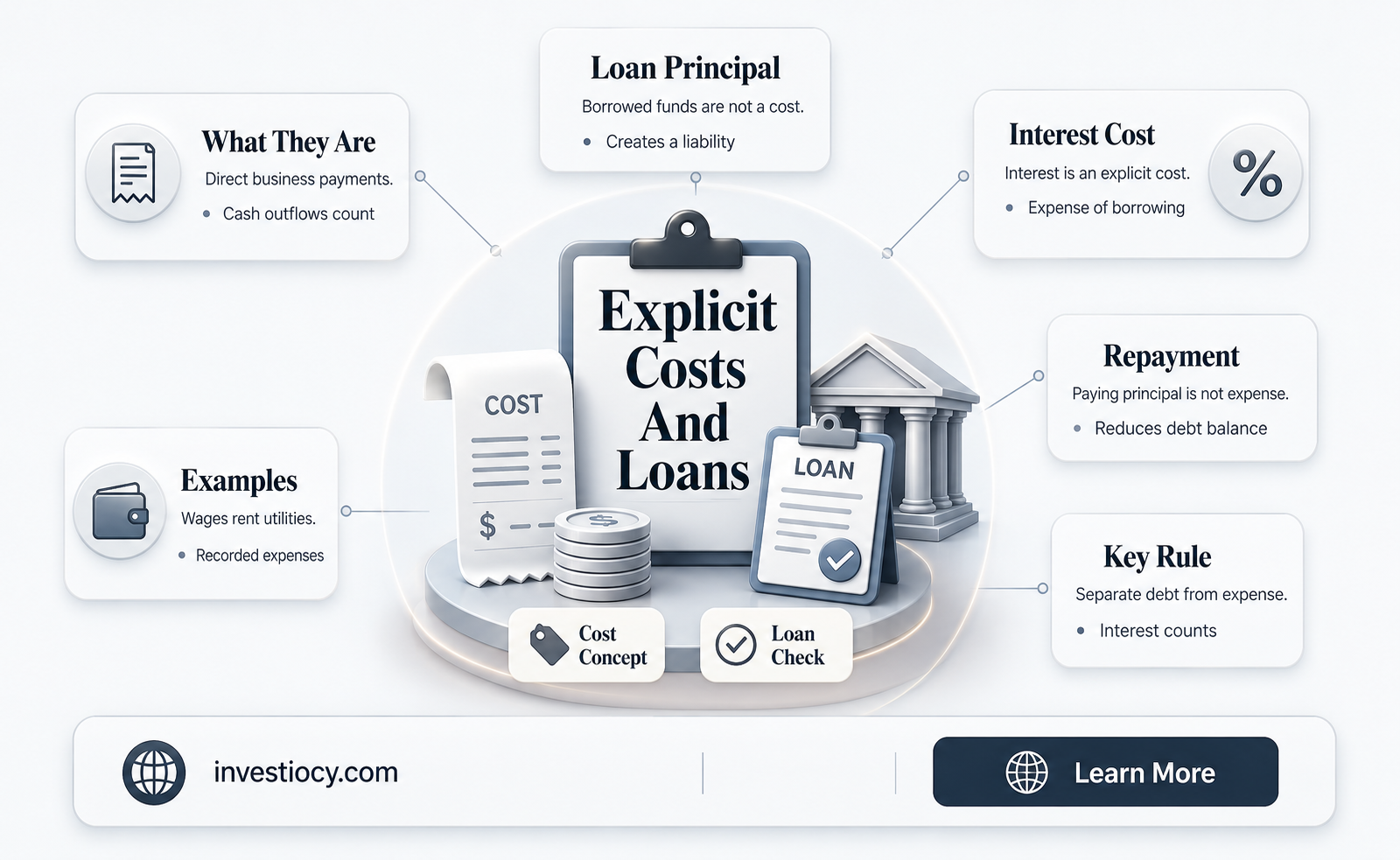

Explicit costs in business accounting refer to the direct, measurable expenses that a company incurs to operate its business. These costs are tangible and can be easily quantified, such as wages, rent, utilities, and materials. When considering whether explicit costs include loans, it's important to understand that loans themselves are not typically classified as explicit costs. Instead, the interest paid on loans is considered an explicit cost because it is a direct expense related to the borrowing of funds. The principal amount of the loan is a liability on the balance sheet, not an expense on the income statement. Therefore, while loans are a significant financial consideration for businesses, they do not directly contribute to the explicit costs of operation in the traditional accounting sense.

Explore related products

What You'll Learn

- Definition of Explicit Costs: Understanding what explicit costs entail in financial contexts

- Loan Interest as an Explicit Cost: Examining whether interest payments on loans qualify as explicit costs

- Principal Repayment: Considering if the principal amount repaid on loans is categorized under explicit costs

- Explicit vs. Implicit Costs: Differentiating between explicit costs and implicit costs in business decisions

- Impact on Financial Statements: Analyzing how explicit costs related to loans affect financial statements and ratios

![]()

Definition of Explicit Costs: Understanding what explicit costs entail in financial contexts

Explicit costs refer to the direct, out-of-pocket expenses that a business incurs in the production of goods or services. These costs are tangible and can be easily measured and recorded. Examples include raw materials, labor wages, rent, utilities, and depreciation. Understanding explicit costs is crucial for businesses to accurately calculate their total cost of production and make informed decisions about pricing and resource allocation.

In financial contexts, explicit costs are often contrasted with implicit costs, which are the opportunity costs of using resources for a particular purpose. While explicit costs are directly observable, implicit costs are not as easily quantifiable and represent the value of the next best alternative forgone. For instance, if a business owner uses their own car for deliveries, the explicit costs might include fuel and maintenance, while the implicit costs could include the value of the time spent driving instead of managing the business.

When considering loans, it's important to note that the interest paid on loans is typically classified as an explicit cost. This is because the interest is a direct expense that the business must pay out of pocket to the lender. However, the principal amount of the loan itself is not considered an explicit cost until it is repaid. Instead, it is treated as a liability on the balance sheet.

In summary, explicit costs are the direct, measurable expenses that a business incurs in its operations. They are distinct from implicit costs, which represent the value of forgone opportunities. When it comes to loans, the interest paid is an explicit cost, while the principal amount is not until it is repaid. Understanding these distinctions is essential for accurate financial analysis and decision-making.

Exploring the Universal Path: Do We All Encounter Loans?

You may want to see also

Explore related products

![]()

Loan Interest as an Explicit Cost: Examining whether interest payments on loans qualify as explicit costs

In the realm of financial analysis, the classification of loan interest as an explicit cost is a subject of considerable debate. Explicit costs are typically defined as direct, out-of-pocket expenses that can be easily identified and measured. These might include salaries, rent, utilities, and raw materials. However, when it comes to loan interest, the waters become murkier. While interest payments are certainly a financial burden, they do not fit neatly into the category of explicit costs as they are not a direct expense but rather a consequence of borrowing money.

To understand why loan interest might not be considered an explicit cost, it's essential to examine the nature of explicit costs more closely. Explicit costs are usually associated with the day-to-day operations of a business or individual. They are the costs that are immediately apparent and can be directly attributed to specific activities or purchases. In contrast, loan interest is a cost that arises from the financing of operations rather than the operations themselves. It is an indirect cost that is incurred over time as a result of borrowing money, rather than a direct expense that is paid upfront.

However, there are arguments to be made for considering loan interest as an explicit cost in certain contexts. For instance, in the case of a business taking out a loan to finance a specific project, the interest payments on that loan could be seen as a direct cost of the project. This is because the interest is a necessary expense that must be paid in order to secure the funding needed for the project. In this scenario, the interest payments are closely tied to the project's operations and can be directly attributed to the decision to undertake the project.

Ultimately, whether or not loan interest is considered an explicit cost depends on the specific circumstances and the perspective from which the analysis is conducted. From a strict accounting standpoint, loan interest may not be classified as an explicit cost because it is not a direct expense. However, from a broader financial analysis perspective, loan interest can be seen as an explicit cost in certain situations where it is directly related to specific operations or projects.

In conclusion, the classification of loan interest as an explicit cost is not a straightforward matter. It requires careful consideration of the nature of explicit costs and the specific context in which the interest payments are incurred. While loan interest may not fit the traditional definition of an explicit cost, there are valid arguments for considering it as such in certain scenarios.

Impact of Exit Counseling on Loan Disbursement: What You Need to Know

You may want to see also

![]()

Principal Repayment: Considering if the principal amount repaid on loans is categorized under explicit costs

In the realm of financial analysis, the classification of costs is crucial for accurate budgeting and decision-making. One area of contention is whether the principal amount repaid on loans should be considered an explicit cost. Explicit costs are those that are directly measurable and involve a clear outlay of cash, such as wages, rent, and materials. In contrast, implicit costs are opportunity costs that are not directly measurable, like the potential profit forgone by not investing in a different project.

The principal repayment on loans is a periodic expense that reduces the outstanding balance of the loan. It is a direct cash outflow that can be easily quantified, which aligns with the definition of explicit costs. However, the argument against classifying it as an explicit cost stems from the fact that it is a repayment of a previously borrowed amount, rather than a new expenditure. This perspective suggests that the principal repayment is more akin to a reduction in liability than an outright cost.

From an accounting standpoint, principal repayments are typically recorded as a reduction in the loan liability account, rather than as an expense on the income statement. This treatment reinforces the idea that it is not an explicit cost, as expenses are usually recorded on the income statement. However, this accounting treatment does not necessarily reflect the economic reality of the situation.

In economic terms, the principal repayment represents a real cost to the borrower, as it reduces their liquidity and available funds for other uses. This opportunity cost of not having access to those funds for alternative investments or expenditures can be significant. Therefore, while the principal repayment may not be classified as an explicit cost in traditional accounting, it can be argued that it should be considered an explicit cost from an economic perspective.

Ultimately, the classification of principal repayment as an explicit cost depends on the context and the specific financial analysis being conducted. In some cases, it may be more appropriate to treat it as an implicit cost, while in others, it may be necessary to recognize it as an explicit cost to accurately reflect the financial reality of the situation.

Decoding the Myth: Do All Students Complete Their MPN Student Loans?

You may want to see also

![]()

Explicit vs. Implicit Costs: Differentiating between explicit costs and implicit costs in business decisions

In the realm of business decision-making, understanding the distinction between explicit and implicit costs is crucial. Explicit costs are those that are directly measurable and can be easily quantified in monetary terms. They include expenses such as rent, utilities, wages, and raw materials. These costs are typically recorded in a company's financial statements and are used to calculate profit and loss.

On the other hand, implicit costs are more elusive. They represent the opportunity costs of using resources in a particular way, essentially the value of the next best alternative forgone. For instance, if a company decides to expand its production capacity by building a new factory, the implicit cost might be the potential revenue it could have earned by investing in a different project. Unlike explicit costs, implicit costs are not directly measurable and often require careful analysis to estimate.

When considering loans, it's important to recognize that while the interest payments and principal repayments are explicit costs, the opportunity cost of borrowing—such as the potential investment returns that could have been earned with the borrowed funds—represents an implicit cost. This distinction is vital for businesses to make informed decisions about whether to take on debt.

In summary, explicit costs are tangible expenses that can be easily quantified, while implicit costs are intangible opportunity costs that require more nuanced analysis. Both types of costs play a significant role in business decision-making, and understanding their differences is key to evaluating the true cost of any business strategy.

Exploring Experian's Loan Services: What You Need to Know

You may want to see also

![]()

Impact on Financial Statements: Analyzing how explicit costs related to loans affect financial statements and ratios

Explicit costs related to loans can have a significant impact on a company's financial statements and ratios. These costs, which include interest payments, loan origination fees, and other charges directly associated with borrowing, are typically recorded as expenses on the income statement. This can reduce net income and, consequently, affect profitability ratios such as return on equity (ROE) and return on assets (ROA).

For instance, if a company takes out a loan with a high interest rate, the interest expense will increase, reducing the net income reported on the income statement. This decrease in net income will then lower the ROE, which is calculated by dividing net income by shareholders' equity. Similarly, the ROA, which is net income divided by total assets, will also be negatively impacted.

Moreover, explicit loan costs can affect the balance sheet by increasing the company's debt obligations. This can lead to a higher debt-to-equity ratio, which may raise concerns about the company's financial leverage and ability to meet its debt repayments. Additionally, if the loan costs are capitalized, they will be recorded as an asset on the balance sheet, which can artificially inflate the company's asset base and potentially mislead investors.

To mitigate these impacts, companies may consider various strategies, such as refinancing loans at lower interest rates, renegotiating loan terms, or exploring alternative financing options. By carefully managing explicit loan costs, companies can improve their financial performance and maintain a healthier balance sheet.

In conclusion, explicit costs related to loans can have far-reaching implications for a company's financial statements and ratios. It is essential for businesses to understand these impacts and implement effective strategies to manage their borrowing costs and maintain financial stability.

Understanding Excess Distribution: Does It Include Loan Basis?

You may want to see also

Frequently asked questions

Explicit costs do not typically include loans. Explicit costs are direct, out-of-pocket expenses that a business incurs, such as wages, rent, and materials. Loans are considered implicit costs because they represent the opportunity cost of using borrowed funds rather than investing them elsewhere.

Examples of explicit costs include salaries, utilities, raw materials, marketing expenses, and depreciation. These are costs that a business can easily measure and record in its financial statements.

Explicit costs are tangible expenses that a business can directly attribute to its operations, while implicit costs are intangible costs that represent the opportunity cost of using resources in one way rather than another. For example, the cost of borrowing money (interest) is an explicit cost, while the opportunity cost of not investing that money elsewhere is an implicit cost.

Loans are considered implicit costs because they represent the opportunity cost of using borrowed funds rather than investing them elsewhere. When a business takes out a loan, it incurs an interest expense, which is an explicit cost. However, the opportunity cost of not using those funds for other investments or purposes is an implicit cost.

To calculate its total costs, a business needs to add up all of its explicit costs, such as salaries, utilities, and materials, as well as its implicit costs, such as the opportunity cost of using borrowed funds. This can be done by using a cost-benefit analysis, which compares the total costs of a decision to its total benefits.