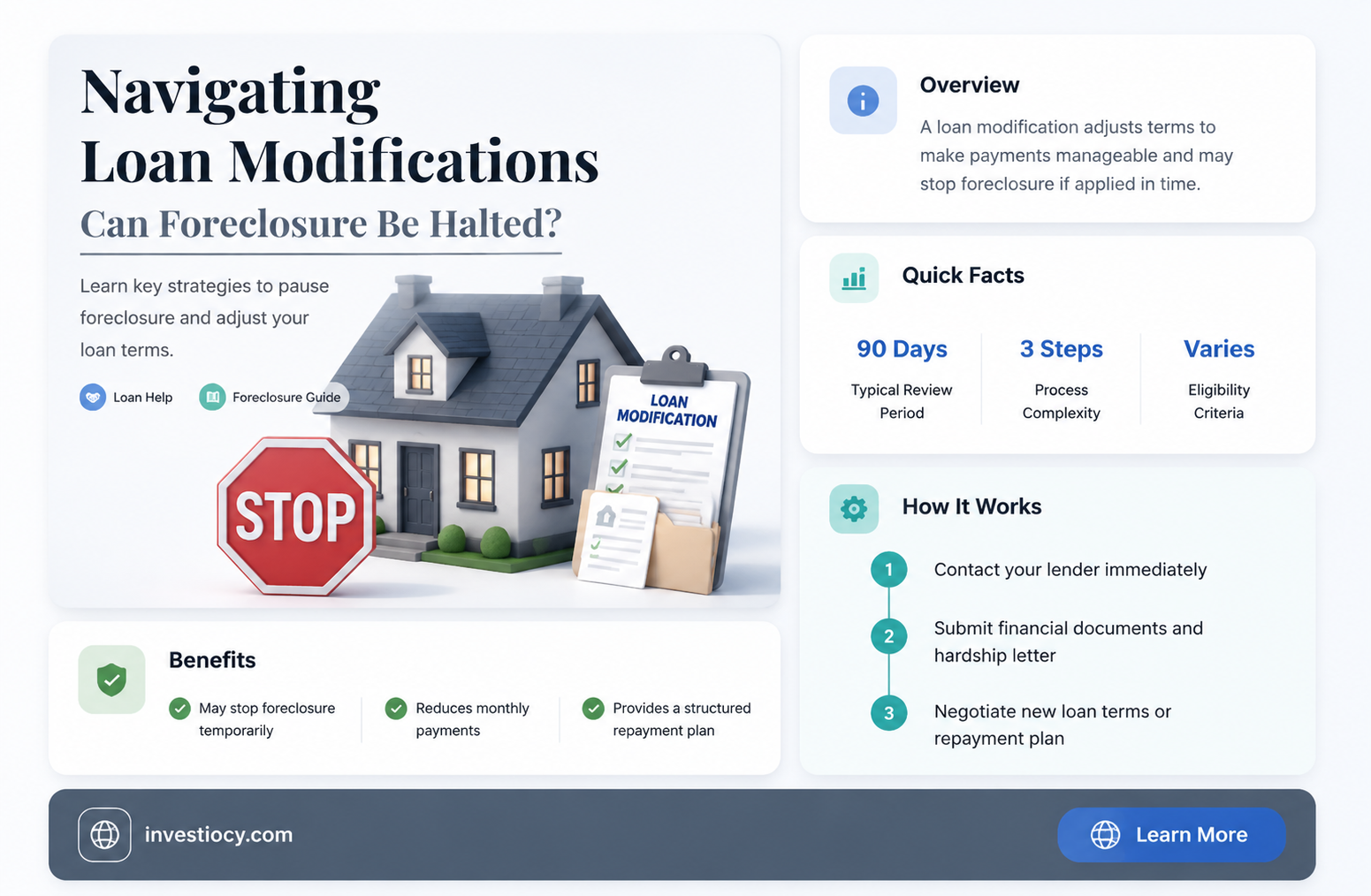

Foreclosure is a legal process that allows a lender to recover the amount owed on a defaulted loan by selling the mortgaged property. However, loan modifications can potentially halt or delay the foreclosure process. A loan modification is a change to the original terms of a mortgage, often aimed at making the payments more affordable for the borrower. When a borrower is struggling to make their mortgage payments, they may seek a loan modification to avoid foreclosure. In some cases, the lender may agree to modify the loan terms, which could include a temporary or permanent reduction in interest rate, an extension of the loan term, or even a principal reduction. If a loan modification is granted, the foreclosure process may be halted or delayed while the borrower works to meet the new payment terms. However, it's important to note that not all loan modifications will stop foreclosure, and the specific terms of the modification will depend on the lender's policies and the borrower's individual circumstances.

| Characteristics | Values |

|---|---|

| Definition | Foreclosure is a legal process where a lender attempts to recover the amount owed on a defaulted loan by selling or taking ownership of the mortgaged property. Loan modification is a change to the original terms of a loan, often to make payments more manageable for the borrower. |

| Purpose | The purpose of foreclosure is to allow the lender to recoup their losses on a defaulted loan. The purpose of loan modification is to adjust the loan terms to make them more affordable for the borrower and to prevent default. |

| Process | Foreclosure involves a series of legal steps, including filing a notice of default, serving the borrower with a summons and complaint, and conducting a foreclosure sale. Loan modification involves negotiating new loan terms between the borrower and the lender, often with the assistance of a loan modification attorney or counselor. |

| Timeline | The foreclosure process can take several months to a year or more, depending on the state and the complexity of the case. Loan modification can take anywhere from a few weeks to several months, depending on the lender's policies and the borrower's situation. |

| Impact on Credit | Foreclosure can have a significant negative impact on a borrower's credit score, potentially dropping it by 100-200 points or more. Loan modification may also have a negative impact on credit, but it is typically less severe than foreclosure. |

| Alternatives | Alternatives to foreclosure include loan modification, short sale, and deed in lieu of foreclosure. Alternatives to loan modification include refinancing, selling the property, or filing for bankruptcy. |

| Legal Requirements | Foreclosure is governed by state law, and the specific requirements vary from state to state. Loan modification is typically governed by the terms of the original loan agreement and any applicable federal or state laws. |

| Costs | The costs of foreclosure can be significant, including legal fees, court costs, and the cost of selling the property. The costs of loan modification may include application fees, appraisal fees, and other miscellaneous costs. |

| Benefits | The benefits of foreclosure include allowing the lender to recover their losses and potentially preventing further financial harm to the borrower. The benefits of loan modification include making the loan more affordable for the borrower, preventing default, and potentially reducing the lender's losses. |

| Drawbacks | The drawbacks of foreclosure include the negative impact on the borrower's credit score, the potential for the borrower to lose their home, and the time-consuming and costly legal process. The drawbacks of loan modification include the potential for the borrower to pay more in interest over the life of the loan, the possibility of the lender denying the modification, and the time-consuming negotiation process. |

Explore related products

What You'll Learn

- Foreclosure Process Overview: Understanding the steps involved in foreclosure and how loan modifications can intervene

- Loan Modification Options: Exploring different types of loan modifications available to homeowners facing foreclosure

- Legal Protections: Discussing federal and state laws that protect homeowners during the loan modification process

- Bank Policies: Reviewing common bank policies regarding foreclosure and loan modifications, including timelines and requirements

- Homeowner Responsibilities: Outlining the homeowner's role and responsibilities during the loan modification process to avoid foreclosure

![]()

Foreclosure Process Overview: Understanding the steps involved in foreclosure and how loan modifications can intervene

The foreclosure process typically begins when a homeowner fails to make mortgage payments as agreed. The lender then initiates legal proceedings to reclaim the property. This process can be lengthy and complex, involving multiple steps such as notice of default, notice of sale, and the actual sale of the property. Understanding these steps is crucial for homeowners facing foreclosure, as it allows them to navigate the process more effectively and potentially find ways to avoid losing their home.

Loan modifications can be a viable option for homeowners struggling to make their mortgage payments. A loan modification involves changing the terms of the existing loan, which can include reducing the interest rate, extending the loan term, or even forgiving a portion of the principal balance. These modifications can make the mortgage more affordable and help the homeowner avoid foreclosure. However, it's important to note that loan modifications are not automatic and require negotiation with the lender.

One common question homeowners facing foreclosure ask is whether the foreclosure process has to stop during loan modification negotiations. The answer to this question can vary depending on the specific circumstances and the lender's policies. In some cases, lenders may agree to temporarily halt the foreclosure process while loan modification negotiations are underway. This can give the homeowner more time to work out a solution and avoid the loss of their home.

However, it's important for homeowners to be aware that not all lenders will agree to stop the foreclosure process during loan modification negotiations. Some lenders may continue with the foreclosure process even while negotiations are ongoing. This can create a sense of urgency for the homeowner, as they may need to take additional steps to protect their property.

In conclusion, understanding the foreclosure process and the potential for loan modifications can be a valuable tool for homeowners facing foreclosure. While loan modifications can offer a way to avoid losing a home, it's important to be aware of the lender's policies and the potential for the foreclosure process to continue even during negotiations. Homeowners should seek professional advice and explore all available options to find the best solution for their specific situation.

Understanding Foreclosure: Does It Hurt Your Loan Prospects?

You may want to see also

Explore related products

![]()

Loan Modification Options: Exploring different types of loan modifications available to homeowners facing foreclosure

Homeowners facing foreclosure may be unaware of the various loan modification options available to them. These options can provide a lifeline, allowing individuals to stay in their homes while they work through financial difficulties. One such option is a forbearance agreement, where the lender agrees to temporarily suspend or reduce mortgage payments. This can provide immediate relief, but it's crucial to understand that the missed payments will need to be repaid in the future.

Another option is a loan modification, which involves changing the terms of the existing mortgage. This could include reducing the interest rate, extending the loan term, or even forgiving a portion of the principal balance. Loan modifications can be complex, and it's essential to work with a qualified professional to ensure the best possible outcome.

In some cases, homeowners may be able to refinance their mortgage, replacing the existing loan with a new one that has more favorable terms. This can be a good option for those who have equity in their home and are looking to lower their monthly payments. However, refinancing can be costly, and it's important to weigh the potential benefits against the fees and closing costs involved.

For those who are struggling to make their mortgage payments due to a temporary hardship, such as a job loss or medical emergency, a temporary loan modification may be available. These modifications typically involve a short-term reduction or suspension of payments, followed by a return to the original loan terms.

It's important to note that not all loan modification options are suitable for every homeowner, and the best course of action will depend on individual circumstances. Homeowners facing foreclosure should consult with a qualified professional, such as a housing counselor or attorney, to explore their options and determine the best path forward. By understanding the various loan modification options available, homeowners can make informed decisions and take steps to protect their investment and avoid foreclosure.

Explore related products

![]()

Legal Protections: Discussing federal and state laws that protect homeowners during the loan modification process

Federal laws provide several protections for homeowners seeking loan modifications. The Home Affordable Modification Program (HAMP), established in 2009, offers incentives to lenders to modify loans for homeowners who are struggling to make their mortgage payments. HAMP requires lenders to reduce monthly payments to no more than 31% of the borrower's gross income and to extend the loan term to 40 years. Additionally, the Federal Housing Administration (FHA) offers a program called FHA-HAMP, which provides similar protections for homeowners with FHA-insured loans.

State laws also offer protections for homeowners during the loan modification process. Many states have enacted legislation that requires lenders to consider loan modifications for homeowners who are facing foreclosure. For example, California's Homeowner Bill of Rights prohibits lenders from pursuing foreclosure while a loan modification application is pending. Similarly, New York's foreclosure prevention law requires lenders to negotiate with homeowners in good faith to reach a mutually agreeable resolution.

Furthermore, some states have implemented programs to assist homeowners with loan modifications. For instance, the California Housing Finance Agency offers a program called Keep Your Home California, which provides financial assistance to homeowners who are struggling to make their mortgage payments. The program offers several options, including loan modifications, principal reductions, and temporary payment assistance.

In addition to these legal protections, homeowners should be aware of their rights during the loan modification process. Lenders are required to provide homeowners with a written response to their loan modification application within a certain timeframe, typically 30 days. If the application is denied, the lender must provide a written explanation of the reasons for the denial. Homeowners also have the right to appeal a denial and to seek assistance from a housing counseling agency.

Overall, federal and state laws provide significant protections for homeowners during the loan modification process. These laws require lenders to consider loan modifications, provide financial assistance, and ensure that homeowners are treated fairly and transparently. By understanding their rights and the available protections, homeowners can navigate the loan modification process with greater confidence and security.

Explore related products

![]()

Bank Policies: Reviewing common bank policies regarding foreclosure and loan modifications, including timelines and requirements

Banks typically have specific policies in place regarding foreclosure and loan modifications. These policies often include timelines and requirements that must be met in order for a loan modification to be considered. For example, a bank may require that a borrower be at least 90 days delinquent on their mortgage payments before they will consider a loan modification. Additionally, banks may have different policies for different types of loans, such as conventional loans versus FHA loans.

One common policy among banks is to require a borrower to provide proof of income and financial hardship in order to qualify for a loan modification. This may include pay stubs, tax returns, and bank statements. The bank will then review the borrower's financial situation to determine if they are eligible for a loan modification. If the borrower is eligible, the bank may offer them a temporary loan modification, which will lower their monthly payments for a set period of time.

Another common policy among banks is to require a borrower to make a certain number of payments on time before they will consider a permanent loan modification. This may be three, six, or twelve months, depending on the bank's policy. If the borrower makes all of their payments on time during this period, the bank may then offer them a permanent loan modification, which will lower their monthly payments for the remainder of the loan term.

It is important to note that bank policies regarding foreclosure and loan modifications can vary widely. Some banks may be more lenient than others, and some may have more stringent requirements. It is also important to note that these policies are subject to change, and borrowers should always check with their bank to determine the most current policies.

In conclusion, bank policies regarding foreclosure and loan modifications are complex and can vary widely from one bank to another. Borrowers who are struggling to make their mortgage payments should contact their bank to discuss their options and determine if they are eligible for a loan modification. By understanding the bank's policies and requirements, borrowers can better navigate the loan modification process and potentially avoid foreclosure.

Explore related products

![]()

Homeowner Responsibilities: Outlining the homeowner's role and responsibilities during the loan modification process to avoid foreclosure

During the loan modification process, homeowners have a critical role to play in ensuring the successful outcome of their application. One of the primary responsibilities is to provide accurate and complete financial documentation to the lender. This includes proof of income, bank statements, and any other relevant financial records. Homeowners must also be proactive in communicating with their lender, promptly responding to requests for additional information or clarification.

Another key responsibility is to understand the terms and conditions of the loan modification agreement. Homeowners should carefully review the proposed modifications, ensuring they are aware of any changes to their interest rate, monthly payments, or loan term. It is also essential to be aware of any potential fees associated with the loan modification process.

Homeowners must also take steps to prevent further financial distress during this period. This may include creating a budget and sticking to it, prioritizing essential expenses, and seeking assistance from a housing counselor if necessary. By demonstrating a commitment to financial responsibility and stability, homeowners can increase their chances of successfully modifying their loan and avoiding foreclosure.

In addition to these responsibilities, homeowners should be aware of potential scams and fraudulent schemes that target individuals facing foreclosure. It is important to be cautious of any unsolicited offers or requests for upfront fees, and to verify the legitimacy of any organization or individual offering assistance.

Ultimately, the loan modification process requires homeowners to be proactive, organized, and vigilant. By fulfilling their responsibilities and working closely with their lender, homeowners can take control of their financial situation and work towards a more stable future.

Frequently asked questions

Yes, foreclosure proceedings must typically halt during loan modification negotiations. Lenders are required to evaluate modification applications in a timely manner and, in many cases, must cease foreclosure actions while the application is being reviewed.

Exceptions can include situations where the borrower has previously been evaluated for a loan modification and was deemed ineligible, or if the lender has already filed a foreclosure lawsuit and the borrower has not responded or contested it. Additionally, some lenders may continue foreclosure if they believe the borrower is not acting in good faith or if the property is at risk of damage or loss of value.

The foreclosure process can vary significantly depending on the state and the complexity of the situation. On average, it can take several months to a few years from the initial default notice to the final sale of the property. Factors influencing the timeline include state laws, lender policies, and the borrower's response to the foreclosure proceedings.

Foreclosure can have severe consequences for borrowers, including the loss of their home, damage to their credit score, and potential deficiency judgments if the sale of the property does not cover the full amount owed on the mortgage. Additionally, foreclosure can lead to emotional distress and financial instability for the borrower and their family.