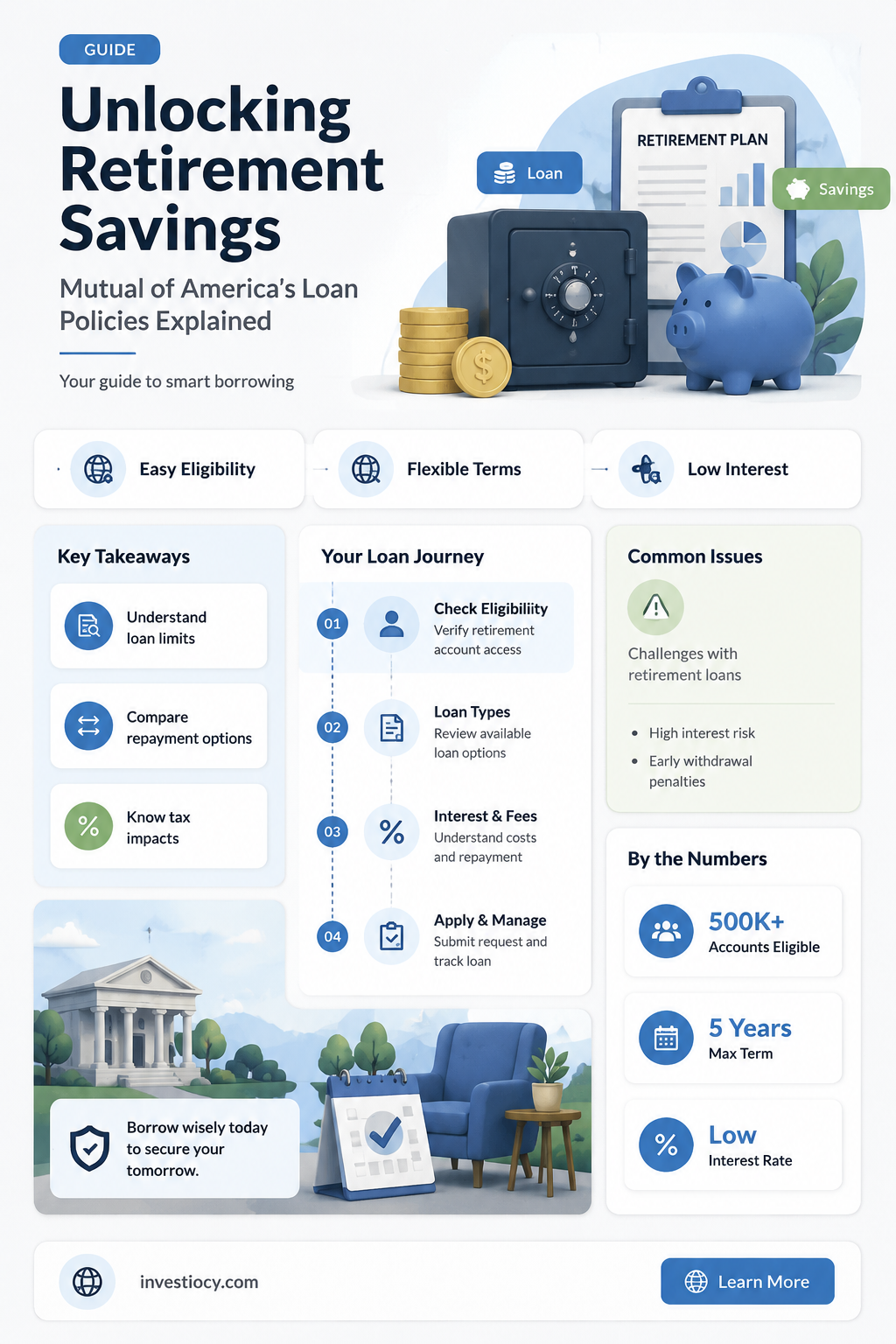

Mutual of America, a prominent insurance company, offers various financial products, including retirement savings plans. One common question among policyholders is whether they can take loans against their retirement savings with Mutual of America. The answer to this question involves understanding the specific terms and conditions of the retirement plan in question, as well as the company's lending policies. Generally, many retirement plans do allow for loans, but they come with certain restrictions and potential penalties. It's crucial for individuals to carefully review their plan documents and consult with a financial advisor before making any decisions regarding loans against their retirement savings.

Explore related products

What You'll Learn

- Loan eligibility criteria for Mutual of America retirement plans

- Interest rates and repayment terms for loans against retirement savings

- Impact of loans on retirement account balances and future earnings

- Alternatives to loans: exploring other financial assistance options

- Steps to apply for a loan against Mutual of America retirement savings

![]()

Loan eligibility criteria for Mutual of America retirement plans

To be eligible for a loan against your Mutual of America retirement savings, you must meet several specific criteria. First and foremost, you must be an active participant in the retirement plan, which means you are currently contributing to the plan or have contributed in the past. Additionally, you must have a vested balance in the plan, which means you have a certain amount of money that you are entitled to receive upon retirement. The exact vesting requirements may vary depending on your specific plan, so it's important to check with your plan administrator for details.

Another key eligibility criterion is your creditworthiness. Mutual of America will likely perform a credit check to determine your ability to repay the loan. This may include reviewing your credit score, payment history, and debt-to-income ratio. If you have a poor credit history or high levels of debt, you may be denied a loan or offered less favorable terms.

The amount you can borrow against your retirement savings is also subject to certain limits. Typically, you can borrow up to 50% of your vested balance, up to a maximum of $50,000. However, this limit may vary depending on your specific plan and circumstances. It's important to note that borrowing against your retirement savings can have significant implications for your long-term financial security, so it's essential to carefully consider the potential risks and benefits before taking out a loan.

In terms of repayment, you will typically have a set period of time, usually 5-10 years, to repay the loan in full. The interest rate on the loan will depend on market conditions and your creditworthiness, but it's generally lower than the interest rate on other types of loans. It's important to make timely payments on your loan to avoid penalties and to ensure that you don't negatively impact your retirement savings.

Finally, it's worth noting that there may be certain restrictions on how you can use the funds from a retirement loan. For example, you may not be able to use the funds for certain types of expenses, such as gambling or illegal activities. Additionally, you may be required to provide documentation to support your loan application, such as proof of income or expenses.

In conclusion, while Mutual of America does allow loans against retirement savings, there are several important eligibility criteria that you must meet. It's essential to carefully review these criteria and to consider the potential risks and benefits before taking out a loan against your retirement savings.

Navigating Loan Options in Michigan: What You Need to Know

You may want to see also

Explore related products

![]()

Interest rates and repayment terms for loans against retirement savings

Loans against retirement savings, such as those offered by Mutual of America, come with specific interest rates and repayment terms that borrowers must understand. The interest rate for these loans is typically lower than that of unsecured loans, as the retirement savings serve as collateral. However, it's crucial to note that the interest rate can vary based on the borrower's creditworthiness, the amount of the loan, and the current market conditions.

Repayment terms for loans against retirement savings are generally more flexible than those of traditional loans. Borrowers can often choose from various repayment schedules, including monthly, quarterly, or annual payments. The repayment period can range from a few years to several decades, depending on the borrower's age, income, and the loan amount. It's important to carefully consider the repayment terms to ensure that they align with the borrower's financial situation and goals.

One unique aspect of loans against retirement savings is that the borrower is essentially paying interest on their own money. This is because the loan is secured by the borrower's retirement savings, which means that the interest paid on the loan is, in effect, reducing the overall growth of the retirement account. As such, it's essential to weigh the benefits of taking out a loan against retirement savings against the potential long-term impact on the borrower's retirement funds.

When considering a loan against retirement savings, borrowers should also be aware of any potential penalties or fees associated with early repayment. Some loans may have prepayment penalties, which can add to the overall cost of the loan if the borrower decides to pay it off early. Additionally, borrowers should consider the tax implications of taking out a loan against retirement savings, as the interest paid on the loan may not be tax-deductible.

In conclusion, loans against retirement savings can be a viable option for borrowers who need access to funds, but it's crucial to carefully consider the interest rates, repayment terms, and potential long-term impact on retirement savings. Borrowers should also be aware of any penalties or fees associated with early repayment and the tax implications of taking out such a loan. By understanding these factors, borrowers can make informed decisions about whether a loan against retirement savings is the right choice for their financial situation.

Unlocking the Potential: How MSHDA Loans Can Fulfill Your $7,500 Dream

You may want to see also

Explore related products

![]()

Impact of loans on retirement account balances and future earnings

Taking a loan against your retirement savings can have significant implications for your financial future. While it may provide immediate access to funds, it's crucial to understand the long-term impact on your retirement account balances and future earnings. When you borrow from your retirement account, you're essentially reducing the amount of money that can grow over time through investments. This can lead to a substantial decrease in your retirement savings, as the loaned amount is no longer earning returns.

Moreover, the interest you pay on the loan may be lower than the potential investment returns you could have earned if the funds remained in your retirement account. This opportunity cost can further diminish your future earnings. Additionally, if you're unable to repay the loan, it may be considered a taxable distribution, resulting in penalties and taxes that could significantly reduce your retirement savings.

It's also important to consider the impact of loan repayments on your cash flow. While you're repaying the loan, you'll have less disposable income, which could affect your ability to save for other financial goals or cover unexpected expenses. Furthermore, if you're nearing retirement age, taking a loan may reduce your ability to maintain your desired standard of living during your golden years.

Before considering a loan against your retirement savings, it's essential to explore alternative options, such as personal loans or home equity loans, which may have less impact on your long-term financial security. If you do decide to take a loan from your retirement account, make sure you understand the terms and conditions, including the repayment schedule, interest rate, and any potential penalties or fees.

In conclusion, while taking a loan against your retirement savings may provide short-term financial relief, it's crucial to carefully weigh the long-term impact on your retirement account balances and future earnings. Consider alternative options and consult with a financial advisor to make an informed decision that aligns with your overall financial goals.

Exploring the Benefits: Does Mudra Loan Offer a Subsidy?

You may want to see also

Explore related products

![]()

Alternatives to loans: exploring other financial assistance options

While loans against retirement savings can be a viable option for some, they're not the only financial assistance avenue worth exploring. In fact, there are several alternatives that can provide similar benefits without the potential drawbacks of dipping into your retirement funds. One such option is a home equity loan or line of credit, which allows you to borrow against the value of your home. This can be particularly advantageous for those with significant equity built up, as it often comes with lower interest rates and more favorable terms than a retirement loan.

Another alternative to consider is a personal loan from a bank or credit union. These loans are typically unsecured, meaning you don't need to put up any collateral, and can be used for a variety of purposes. While the interest rates may be higher than those of a retirement loan, they can still be more competitive than credit card rates, making them a viable option for consolidating debt or covering unexpected expenses.

For those with a strong credit history, a balance transfer credit card could also be a useful tool. These cards often come with promotional periods of 0% interest, allowing you to transfer existing debt and pay it off without accruing additional interest charges. Just be mindful of the balance transfer fees and the interest rate that applies after the promotional period ends.

If you're a homeowner, you might also consider a reverse mortgage. This type of loan allows you to convert a portion of your home's equity into cash, which can be used for any purpose. The loan is repaid when you sell the home, move out, or pass away. While reverse mortgages can provide a valuable source of income, they do come with certain risks and complexities, so it's essential to carefully weigh the pros and cons before proceeding.

Finally, for those with access to a 401(k) or similar retirement plan, a hardship withdrawal might be an option. This allows you to withdraw funds from your retirement account for certain qualified expenses, such as medical bills or the purchase of a primary residence. However, it's important to note that hardship withdrawals are subject to taxes and penalties, and should only be considered as a last resort.

In conclusion, while loans against retirement savings can be a useful financial tool, they're not the only option available. By exploring alternatives such as home equity loans, personal loans, balance transfer credit cards, reverse mortgages, and hardship withdrawals, you can find the best solution for your unique financial situation.

Exploring MSHDA's Loan Programs: Is the 203k Loan Included?

You may want to see also

Explore related products

![]()

Steps to apply for a loan against Mutual of America retirement savings

To apply for a loan against your Mutual of America retirement savings, you must first meet certain eligibility criteria. Typically, this includes being at least 59½ years old, having a vested account balance, and not having any outstanding loans or withdrawals in the past 12 months. Once you've confirmed your eligibility, you can proceed with the application process.

The application process for a loan against your Mutual of America retirement savings involves several steps. First, you'll need to gather the necessary documentation, which may include proof of identity, income verification, and account statements. Next, you'll need to fill out the loan application form, which can be obtained from Mutual of America's website or by contacting their customer service department. Be sure to read the terms and conditions carefully before submitting your application.

After submitting your application, you'll need to wait for Mutual of America to review and approve it. This process can take several weeks, so be patient. If your application is approved, you'll receive a loan agreement that outlines the terms of the loan, including the interest rate, repayment schedule, and any fees associated with the loan.

Before taking out a loan against your retirement savings, it's important to consider the potential risks and consequences. Borrowing from your retirement account can reduce your overall savings and impact your ability to retire comfortably. Additionally, if you're unable to repay the loan, you may face penalties and taxes. It's always a good idea to consult with a financial advisor before making any major financial decisions.

In conclusion, applying for a loan against your Mutual of America retirement savings can be a viable option in certain situations, but it's important to carefully consider the risks and consequences before proceeding. By following the steps outlined above and consulting with a financial advisor, you can make an informed decision about whether a loan against your retirement savings is right for you.

Navigating Loan Dynamics: The Impact of Multiple Buyers Explained

You may want to see also

Frequently asked questions

Yes, Mutual of America does allow loans against retirement savings. Participants in their retirement plans can apply for loans, which are essentially borrowing from their own retirement accounts.

To be eligible for a retirement loan from Mutual of America, you must be an active participant in their retirement plan and have a vested account balance. Specific eligibility criteria may vary, so it's best to check with Mutual of America directly for the most up-to-date information.

The amount you can borrow from your retirement savings with Mutual of America depends on your vested account balance and other factors. Typically, you can borrow up to 50% of your vested balance, but there may be minimum and maximum loan amounts. Contact Mutual of America for specific details.

Interest rates and repayment terms for retirement loans from Mutual of America vary based on the specific loan program and your individual circumstances. Generally, the interest rate is based on the prime rate plus a margin, and repayment terms can range from a few years to over a decade. It's important to review the loan agreement carefully to understand all the terms and conditions.

Taking a loan from your retirement savings with Mutual of America may have tax implications and potential penalties. For example, if you fail to repay the loan within the specified time frame, it may be considered a taxable distribution, and you could face a 10% early withdrawal penalty if you're under age 59 1/2. Additionally, interest paid on the loan may not be tax-deductible. It's advisable to consult with a tax professional to fully understand the implications before taking a retirement loan.