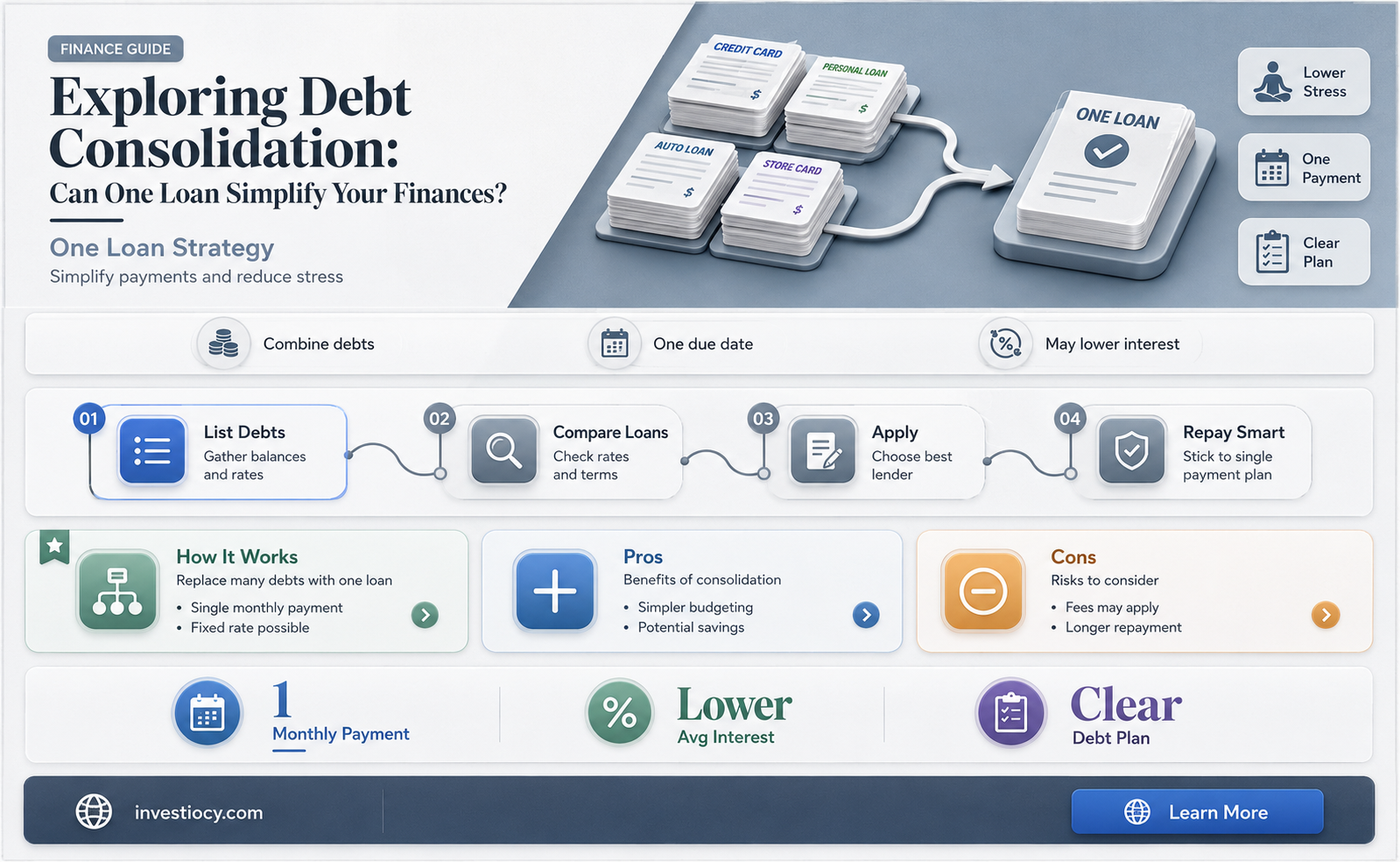

Consolidation loans are a financial tool that allows individuals to combine multiple debts into a single, more manageable loan. This can be particularly helpful for those juggling several high-interest debts, such as credit card balances or personal loans. By consolidating these debts, borrowers can often secure a lower interest rate and simplify their repayment process. However, the availability and terms of consolidation loans can vary depending on the lender and the borrower's creditworthiness. It's essential to carefully evaluate the terms and conditions of any consolidation loan offer to ensure it aligns with one's financial goals and capabilities.

| Characteristics | Values |

|---|---|

| Loan Type | Consolidation Loan |

| Purpose | To combine multiple debts into a single loan |

| Interest Rate | Varies, typically lower than credit card rates |

| Loan Term | Can range from 2 to 7 years |

| Loan Amount | Depends on the total debt being consolidated |

| Monthly Payment | Fixed, based on loan amount and interest rate |

| Credit Score | May require a minimum score, varies by lender |

| Collateral | Unsecured or secured (varies by loan type) |

| Fees | Origination fees, late fees, prepayment fees (varies by lender) |

| Benefits | Lower monthly payments, single payment, potential credit score improvement |

| Risks | Risk of extending debt repayment period, potential for higher total interest paid |

| Eligibility | Must have multiple debts, meet credit score and income requirements |

| Application | Online, phone, or in-person (varies by lender) |

| Approval Time | Can take several days to weeks |

| Disbursement | Funds disbursed directly to creditors or to the borrower |

| Repayment | Monthly payments, automatic or manual (varies by lender) |

| Customer Support | Varies by lender, typically includes online and phone support |

Explore related products

What You'll Learn

![]()

What is a consolidation loan?

A consolidation loan is a financial tool designed to simplify debt management by combining multiple debts into a single loan with one monthly payment. This type of loan can be particularly beneficial for individuals juggling several high-interest debts, such as credit card balances, personal loans, or medical bills. By consolidating these debts, borrowers can potentially lower their overall interest rate, reduce their monthly payment amount, and streamline their financial obligations.

OneMain Financial, a lending company, offers consolidation loans as part of its suite of financial services. These loans are typically unsecured, meaning they do not require collateral such as a home or vehicle. Instead, approval is based on the borrower's creditworthiness and ability to repay the loan. OneMain's consolidation loans can range from $1,500 to $20,000, with repayment terms varying from 24 to 60 months. Interest rates are fixed, providing borrowers with predictable monthly payments.

The process of obtaining a consolidation loan from OneMain involves several steps. First, potential borrowers must apply for the loan, either online or in person at a OneMain branch. The application will require personal and financial information, including income, employment history, and existing debts. Once approved, the borrower will receive the loan funds, which can then be used to pay off the outstanding debts. OneMain will then manage the repayment of the consolidation loan, reporting payments to the credit bureaus.

Consolidation loans can have a significant impact on a borrower's credit score. By paying off multiple debts and reducing the overall debt-to-income ratio, individuals may see an improvement in their creditworthiness. However, it is essential to make timely payments on the consolidation loan to avoid further damaging credit. Additionally, borrowers should be cautious not to accumulate new debt while paying off the consolidation loan, as this could negate the benefits of debt consolidation.

In summary, a consolidation loan from OneMain Financial can be a valuable tool for individuals looking to simplify their debt management and potentially improve their financial situation. By understanding the loan terms, application process, and potential impact on credit, borrowers can make informed decisions about whether a consolidation loan is right for them.

Exploring the Benefits and Drawbacks of 401(k) Loans in America

You may want to see also

Explore related products

![]()

Benefits of consolidation loans

Consolidation loans offer several benefits that can significantly improve an individual's financial situation. One of the primary advantages is the simplification of debt management. By consolidating multiple debts into a single loan, borrowers can streamline their monthly payments, reducing the likelihood of missed payments and late fees. This can be particularly beneficial for those juggling several high-interest debts, such as credit card balances, personal loans, or medical bills.

Another key benefit is the potential for lower interest rates. Consolidation loans often come with more favorable terms than the original debts, including reduced interest rates. This can lead to substantial savings over the life of the loan, as well as a faster path to debt repayment. For example, if an individual has multiple credit cards with interest rates ranging from 18% to 24%, a consolidation loan with an interest rate of 10% could significantly lower their overall interest burden.

Additionally, consolidation loans can help improve credit scores. By paying off multiple debts and consolidating them into a single loan, borrowers can reduce their credit utilization ratio, which is a critical factor in determining credit scores. A lower credit utilization ratio can lead to an increase in credit scores, making it easier to secure future loans or credit cards with favorable terms.

Furthermore, consolidation loans can provide a sense of relief and reduce financial stress. The burden of managing multiple debts can be overwhelming, leading to anxiety and sleepless nights. Consolidating these debts into a single, manageable payment can alleviate this stress, allowing individuals to focus on other aspects of their lives.

Lastly, consolidation loans can offer flexibility in repayment terms. Borrowers can often choose from various repayment options, such as fixed-rate or variable-rate loans, as well as different loan terms. This flexibility can help individuals tailor their loan to their specific financial situation and goals, ensuring that they can comfortably meet their repayment obligations.

In conclusion, consolidation loans can provide numerous benefits, including simplified debt management, lower interest rates, improved credit scores, reduced financial stress, and flexible repayment terms. These advantages make consolidation loans an attractive option for those looking to take control of their finances and achieve a more stable financial future.

Exploring OnDeck's Role in Startup Financing: Loan Options Unveiled

You may want to see also

![]()

Types of consolidation loans

There are several types of consolidation loans available, each tailored to meet specific financial needs and circumstances. One common type is the secured consolidation loan, which requires collateral such as a home or vehicle to secure the loan. This option often offers lower interest rates and higher borrowing limits, making it suitable for individuals with significant debt or those looking to consolidate larger amounts.

Another type is the unsecured consolidation loan, which does not require collateral. These loans are typically based on the borrower's creditworthiness and may have higher interest rates compared to secured loans. Unsecured consolidation loans are ideal for those who do not own assets to use as collateral or prefer not to risk their assets.

For individuals with high-interest credit card debt, a balance transfer consolidation loan can be an effective option. This type of loan allows borrowers to transfer their existing credit card balances to a new loan with a lower interest rate, potentially saving money on interest charges and simplifying debt repayment.

Additionally, there are specialized consolidation loans designed for specific purposes, such as student loan consolidation or debt consolidation for veterans. These loans often have unique features and benefits tailored to the needs of the target demographic.

When considering a consolidation loan, it's essential to evaluate the different types available and choose the one that best aligns with your financial goals and situation. Factors to consider include interest rates, repayment terms, borrowing limits, and any associated fees or penalties. By selecting the right type of consolidation loan, you can effectively manage your debt and work towards a more stable financial future.

Exploring Loan Modification Options with Ocwen: A Comprehensive Guide

You may want to see also

![]()

How to qualify for a consolidation loan

Qualifying for a consolidation loan involves meeting specific criteria set by the lender. Typically, this includes having a steady income, a good credit score, and a manageable debt-to-income ratio. Lenders may also require collateral, such as a home or vehicle, to secure the loan. It's important to note that each lender has its own set of requirements, so it's essential to shop around and compare options to find the best fit for your financial situation.

To improve your chances of qualifying for a consolidation loan, it's crucial to review your credit report and address any errors or discrepancies. Paying down existing debts and avoiding new ones can also help improve your debt-to-income ratio, making you a more attractive candidate for a consolidation loan. Additionally, having a co-signer with a strong credit score can increase your likelihood of approval.

When applying for a consolidation loan, be prepared to provide detailed information about your income, expenses, and debts. This may include pay stubs, tax returns, and bank statements. It's also important to have a clear understanding of the loan terms, including the interest rate, repayment period, and any fees associated with the loan.

In some cases, a consolidation loan may not be the best option for managing debt. For example, if you have a high debt-to-income ratio or a poor credit score, you may not qualify for a loan with favorable terms. In these situations, it may be more beneficial to explore alternative debt management strategies, such as debt settlement or credit counseling.

Ultimately, qualifying for a consolidation loan requires careful consideration of your financial situation and a thorough understanding of the lender's requirements. By taking the time to research and prepare, you can increase your chances of securing a loan that helps you achieve your financial goals.

Exploring Title Loan Options in Ohio: What You Need to Know

You may want to see also

![]()

Alternatives to consolidation loans

If you're considering a consolidation loan but aren't sure if OneMain Financial is the right lender for you, there are several alternatives to explore. These options can help you manage your debt more effectively and potentially save money on interest and fees.

One alternative is a balance transfer credit card. This type of card allows you to transfer your existing debt onto a new card with a lower interest rate, often 0% for a promotional period. This can give you time to pay off your debt without accruing additional interest. However, be aware of balance transfer fees, which can range from 3% to 5% of the transferred amount.

Another option is a personal loan from a different lender. Personal loans are unsecured loans that can be used for any purpose, including debt consolidation. They often have lower interest rates than credit cards and can provide a fixed monthly payment and repayment term. You can use a personal loan calculator to estimate your monthly payments and total interest costs.

If you're struggling to make ends meet, a debt management plan (DMP) might be a good option. A DMP is a program offered by credit counseling agencies that helps you create a budget and negotiate lower interest rates and fees with your creditors. You'll make a single monthly payment to the credit counseling agency, which will then distribute the funds to your creditors.

For homeowners, a home equity loan or line of credit can be a viable alternative to a consolidation loan. These types of loans allow you to borrow against the equity in your home, often at a lower interest rate than unsecured loans. However, be cautious, as you're putting your home at risk if you can't make the payments.

Finally, if you're dealing with a small amount of debt, you might consider the snowball method or the avalanche method for paying off your debt. The snowball method involves paying off your smallest debt first, while the avalanche method focuses on paying off the debt with the highest interest rate first. Both methods can be effective, but the avalanche method can save you more money on interest in the long run.

Exploring OnDeck's Loan Ownership: A Detailed Analysis

You may want to see also

Frequently asked questions

A consolidation loan is a type of loan that allows you to combine multiple debts into a single loan with a lower interest rate and a longer repayment term.

A consolidation loan works by paying off your existing debts with the loan amount, then you repay the loan over time with a single monthly payment.

The benefits of a consolidation loan include a lower interest rate, a longer repayment term, and the convenience of a single monthly payment.

The drawbacks of a consolidation loan include the possibility of a higher total interest cost over the life of the loan, and the risk of falling behind on payments if you're not careful.

A consolidation loan may be right for you if you have multiple debts with high interest rates, and you're struggling to make your monthly payments. However, it's important to carefully consider the pros and cons before making a decision.