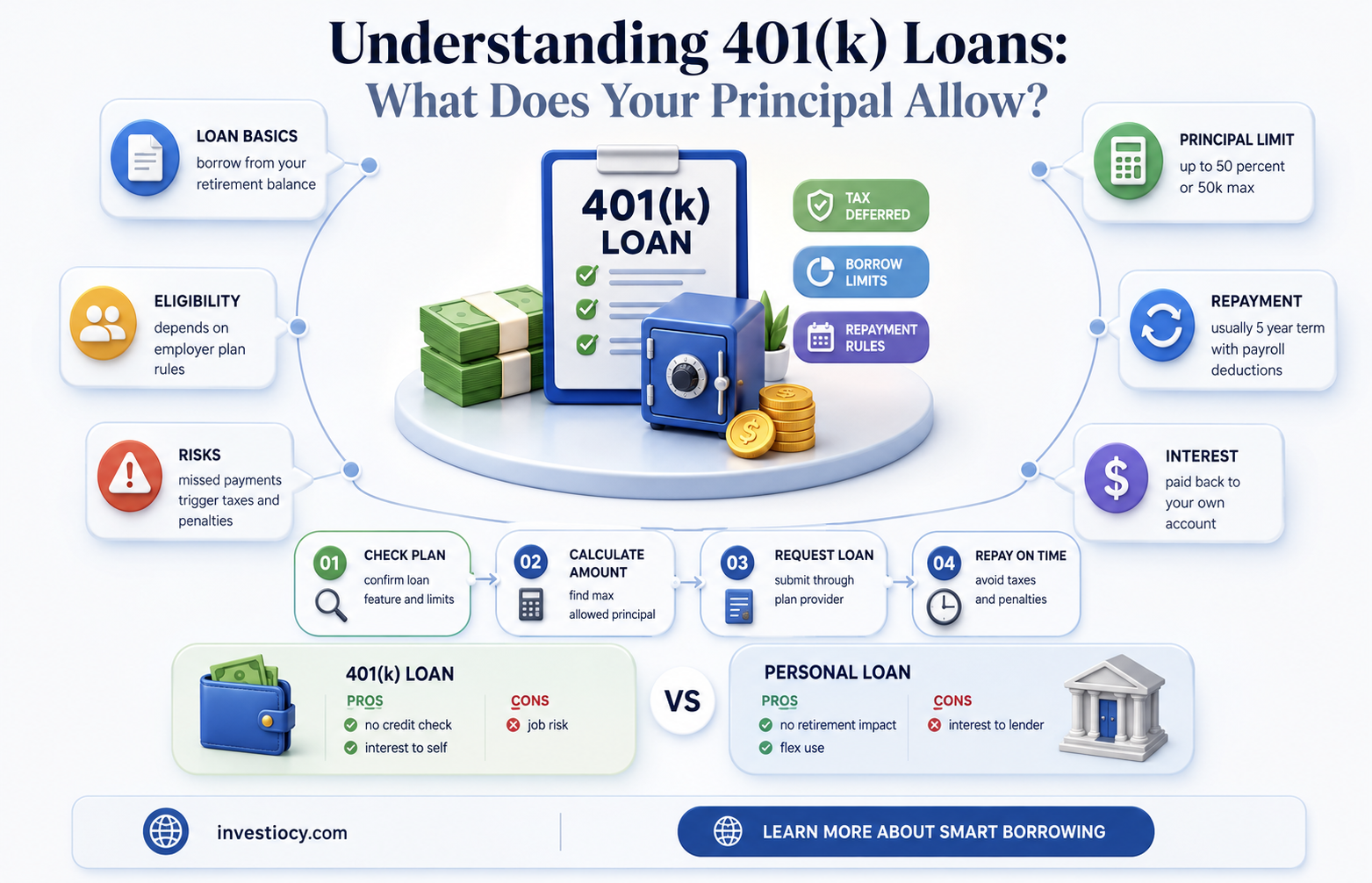

A 401(k) loan allows participants to borrow money from their retirement savings plan. This type of loan can be beneficial for those who need immediate funds for emergencies or other financial obligations. However, not all employers permit 401(k) loans, and the rules surrounding such loans can vary significantly from one plan to another. It is essential to consult with the plan administrator or human resources department to determine if 401(k) loans are allowed under the specific plan and to understand the terms and conditions associated with such loans.

Explore related products

$14.99

What You'll Learn

- Eligibility Criteria: Principal's guidelines on who can apply for a 401k loan

- Loan Limits: Maximum amount one can borrow from their 401k plan

- Interest Rates: The interest rates charged on 401k loans by Principal

- Repayment Terms: Conditions and timelines for repaying a 401k loan

- Impact on Retirement: How taking a 401k loan affects retirement savings and future financial planning

![]()

Eligibility Criteria: Principal's guidelines on who can apply for a 401k loan

To determine eligibility for a 401k loan, the principal typically considers several key factors. First and foremost, the applicant must be an active participant in the 401k plan, meaning they are currently contributing to the account. This ensures that the individual has a vested interest in the plan and is not merely seeking to exploit the loan feature without participating in the retirement savings aspect. Additionally, the principal may require that the applicant has reached a certain age or has been employed with the company for a minimum period to qualify for the loan. These criteria help to mitigate the risk of default and ensure that the loan is being used for its intended purpose.

Another important consideration is the applicant's creditworthiness. The principal may review the individual's credit history and score to assess their ability to repay the loan. A strong credit profile can increase the likelihood of approval and may also result in more favorable loan terms, such as a lower interest rate. Conversely, a poor credit history may lead to denial of the loan application or the imposition of stricter terms.

The principal may also impose limits on the amount that can be borrowed. This is typically based on the applicant's vested account balance, with the loan amount capped at a certain percentage of the total balance. This helps to prevent individuals from overextending themselves financially and ensures that they have sufficient funds remaining in their 401k account for retirement purposes.

Furthermore, the principal may require that the loan be used for a specific purpose, such as purchasing a primary residence, paying for education expenses, or covering medical costs. This helps to ensure that the loan is being used responsibly and for legitimate financial needs. The principal may also mandate that the applicant provide documentation to support the intended use of the loan funds.

In conclusion, the principal's guidelines for eligibility for a 401k loan are designed to balance the need for financial flexibility with the responsibility of ensuring that the loan is used prudently and repaid in a timely manner. By considering factors such as participation in the plan, creditworthiness, loan amount, and intended use, the principal can make informed decisions about who can apply for a 401k loan and under what terms.

Prequalification vs. Loan Approval: Understanding the Key Differences

You may want to see also

Explore related products

![]()

Loan Limits: Maximum amount one can borrow from their 401k plan

The maximum amount one can borrow from their 401k plan, commonly referred to as the loan limit, is a critical aspect to understand when considering a 401k loan. According to the IRS, the maximum loan amount is generally 50% of the vested account balance, up to a maximum of $50,000. However, it's essential to note that these limits can vary depending on the specific plan's provisions and the participant's individual circumstances.

For instance, some plans may allow for a higher loan limit, up to 100% of the vested balance, while others may impose lower limits or additional restrictions. Furthermore, the loan limit may be adjusted based on the participant's creditworthiness, repayment history, and other factors. Therefore, it's crucial to review the plan's documentation and consult with the plan administrator or a financial advisor to determine the exact loan limit applicable to a specific situation.

In addition to the loan limit, it's also important to consider the repayment terms and interest rates associated with a 401k loan. The repayment period typically ranges from 5 to 15 years, and the interest rate is often based on the prime rate plus a margin. Participants should carefully evaluate these terms to ensure that they can comfortably meet the repayment obligations and avoid potential penalties or tax consequences.

Moreover, it's worth noting that taking a 401k loan can have a significant impact on an individual's retirement savings. By borrowing from the plan, participants may reduce their overall retirement balance and potentially miss out on investment gains. Therefore, it's essential to weigh the benefits of a 401k loan against the potential long-term consequences and explore alternative financing options whenever possible.

In conclusion, understanding the loan limits and terms associated with a 401k loan is crucial for making informed financial decisions. Participants should carefully review their plan's provisions, consult with financial professionals, and consider the potential impact on their retirement savings before proceeding with a 401k loan.

Exploring Prime Choice Funding's No-Income Verification Loan Options

You may want to see also

Explore related products

![]()

Interest Rates: The interest rates charged on 401k loans by Principal

Principal Financial Group, a leading provider of retirement savings solutions, offers 401k loans to participants in certain plans. The interest rates charged on these loans are a critical aspect to consider for individuals thinking about borrowing from their retirement savings. Unlike some other financial institutions, Principal’s interest rates on 401k loans are typically competitive and designed to be in the best interest of the plan participants.

The interest rate on a 401k loan from Principal is generally based on the prime rate, which is the interest rate that banks charge to their most creditworthy customers. This rate can fluctuate over time in response to changes in the federal funds rate set by the Federal Reserve. Principal often adds a small margin to the prime rate to determine the final interest rate offered to borrowers. This margin helps cover the administrative costs associated with managing the loans.

One unique feature of Principal’s 401k loan interest rates is that they may offer a fixed rate option. This can provide borrowers with predictability and stability, knowing that their interest payments will remain the same throughout the life of the loan, regardless of changes in the prime rate. Fixed rates can be particularly advantageous in a rising interest rate environment, as they protect borrowers from increasing costs.

Another important consideration is the impact of interest rates on the overall cost of borrowing. Even a small difference in interest rates can significantly affect the amount of interest paid over the course of a loan. For example, if a borrower takes out a $50,000 loan at an interest rate of 4%, they will pay approximately $10,000 in interest over a 10-year repayment period. However, if the interest rate is 6%, the total interest paid would increase to around $15,000. Therefore, it is crucial for borrowers to carefully evaluate the interest rates offered by Principal and other lenders before deciding to take out a 401k loan.

In conclusion, Principal’s interest rates on 401k loans are an essential factor for plan participants to consider when thinking about borrowing from their retirement savings. By understanding how these rates are determined and the potential impact on the overall cost of borrowing, individuals can make more informed decisions about whether a 401k loan is right for them.

How Your Principal Influences Loan Approval: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Repayment Terms: Conditions and timelines for repaying a 401k loan

Repayment terms for a 401(k) loan are critical to understand as they dictate the conditions and timelines for returning the borrowed funds to your retirement account. Generally, these terms are designed to ensure that you repay the loan within a reasonable period, typically five years, although some plans may allow for longer repayment periods depending on the purpose of the loan.

The repayment process usually involves automatic payroll deductions, which are set up when you take out the loan. These deductions are taken from your paycheck before taxes are withheld, which can help you repay the loan more quickly and efficiently. It's important to note that if you leave your job or experience a reduction in pay, you may need to make alternative arrangements to continue making loan payments.

Interest rates on 401(k) loans are generally lower than those on other types of loans, such as credit cards or personal loans. However, it's essential to consider the impact of borrowing from your retirement savings, as you may miss out on potential investment gains while the funds are out of your account. Additionally, if you fail to repay the loan according to the terms, it may be considered a taxable distribution, which could result in penalties and taxes.

To avoid such consequences, it's crucial to carefully review the repayment terms and ensure that you can meet the obligations before taking out a 401(k) loan. If you're unsure about your ability to repay the loan, it may be wise to explore other financial options or consult with a financial advisor to discuss the potential risks and benefits.

In summary, understanding the repayment terms for a 401(k) loan is essential for making informed financial decisions. By carefully considering the conditions and timelines for repayment, you can ensure that you're able to return the borrowed funds to your retirement account while minimizing potential risks and penalties.

Unveiling the Truth: Does Prime Lending Sell Loans?

You may want to see also

Explore related products

![]()

Impact on Retirement: How taking a 401k loan affects retirement savings and future financial planning

Taking a 401(k) loan can have significant implications for your retirement savings and future financial planning. While it may provide a short-term solution for accessing funds, it's crucial to understand the long-term impact on your financial health. When you take a 401(k) loan, you are essentially borrowing from your future self, and this can lead to a reduction in the overall growth of your retirement account.

One of the primary concerns with 401(k) loans is the potential for a snowball effect on your savings. If you're not able to repay the loan promptly, you may find yourself taking out additional loans to cover the payments, leading to a cycle of debt within your retirement account. This can significantly deplete your savings over time, leaving you with less financial security in your golden years.

Furthermore, 401(k) loans often come with interest rates that, while lower than those of credit cards or personal loans, can still add up over time. This interest is typically paid back to your own account, but it does not contribute to the overall growth of your investments. Instead, it serves as a cost for accessing your own funds prematurely.

Another critical aspect to consider is the impact on your investment strategy. When you take a 401(k) loan, you may need to adjust your asset allocation to ensure you have sufficient liquidity to meet the loan payments. This could mean shifting funds from higher-growth investments to more conservative options, potentially limiting the long-term growth of your account.

In terms of future financial planning, taking a 401(k) loan can also affect your ability to save for other important goals, such as buying a home or funding your children's education. By tapping into your retirement savings, you may need to reevaluate your priorities and adjust your savings strategy to accommodate these other financial objectives.

In conclusion, while a 401(k) loan can provide a temporary financial solution, it's essential to carefully consider the long-term impact on your retirement savings and overall financial planning. By understanding the potential consequences and weighing the pros and cons, you can make a more informed decision about whether a 401(k) loan is the right choice for your financial situation.

Frequently asked questions

It depends on the specific principal and the terms of the 401k plan. Some principals may permit loans under certain conditions, while others may not allow them at all.

Common conditions include a minimum employment period, a maximum loan amount (often a percentage of the vested account balance), repayment terms (including interest rates), and the purpose of the loan (e.g., home purchase, education expenses).

The decision is usually based on the financial stability of the employee, the potential impact on the employee's retirement savings, and the administrative burden of managing the loan.

Taking a 401k loan can reduce the amount of money available for retirement, incur interest costs, and potentially lead to penalties if the loan is not repaid according to the terms. It's important to consider these implications carefully before deciding to take a loan.

Yes, there are several alternatives, such as personal loans, home equity loans, or credit cards. Each option has its own set of terms, interest rates, and repayment schedules, so it's advisable to compare them and choose the one that best fits your financial situation and needs.