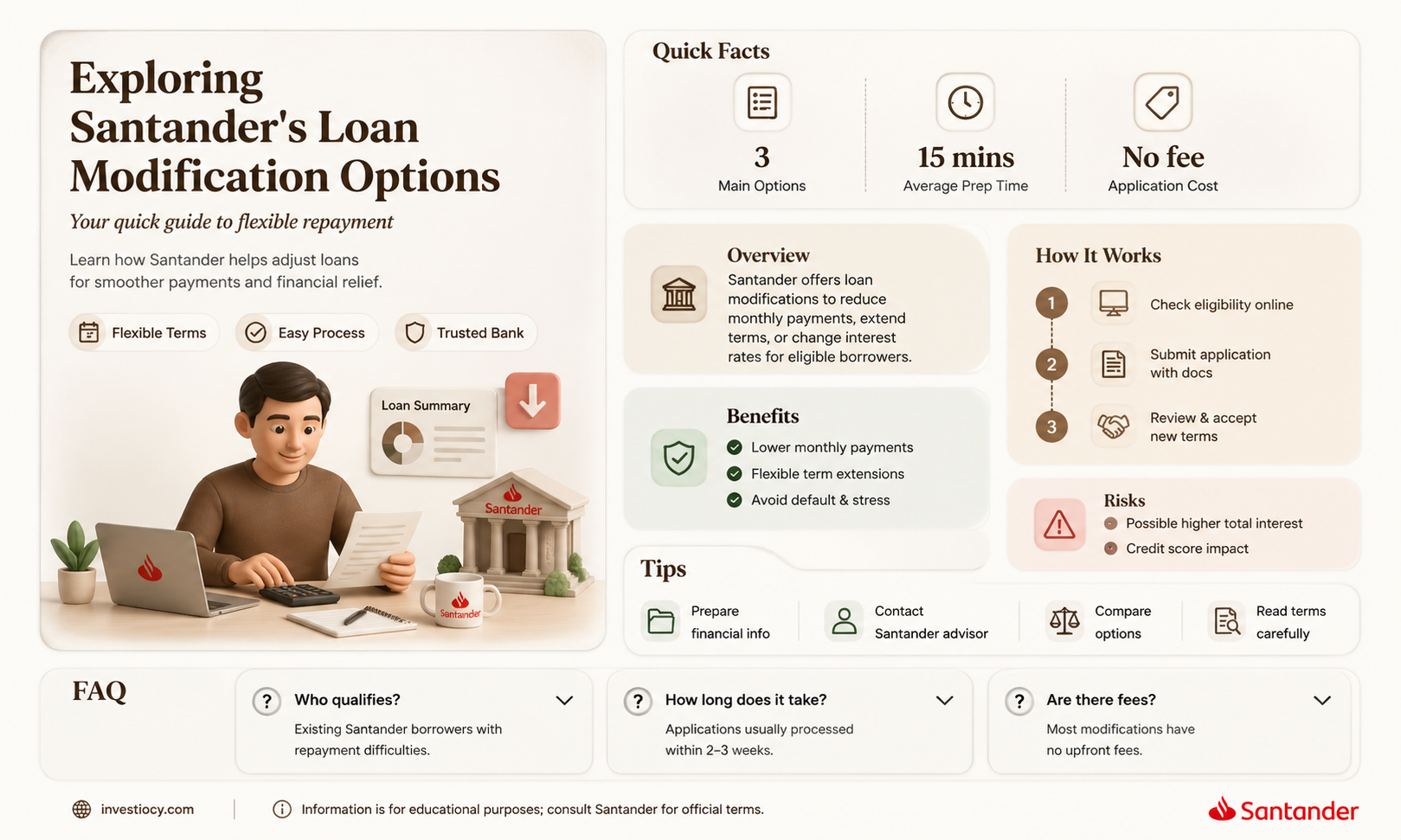

Santander, a prominent global banking group, offers a range of financial services including loan modifications. Loan modifications are changes made to the original terms of a loan, often to help borrowers who are struggling to make their payments. These modifications can include reducing the interest rate, extending the loan term, or changing the type of loan. Santander's approach to loan modifications varies by region and the specific circumstances of the borrower. In general, they aim to work with customers to find solutions that help them avoid default and maintain their creditworthiness. If you're a Santander customer facing financial difficulties, it's advisable to contact them directly to discuss potential loan modification options.

Explore related products

What You'll Learn

- Eligibility Criteria: Requirements homeowners must meet to qualify for a Santander loan modification

- Application Process: Steps involved in applying for a loan modification with Santander

- Types of Modifications: Different kinds of loan modifications Santander offers, such as rate changes or term extensions

- Benefits and Drawbacks: Advantages and potential downsides of modifying a loan with Santander

- Customer Reviews: Experiences and feedback from customers who have undergone loan modifications with Santander

![]()

Eligibility Criteria: Requirements homeowners must meet to qualify for a Santander loan modification

To qualify for a Santander loan modification, homeowners must meet specific eligibility criteria. These requirements are designed to ensure that the modification is feasible for both the borrower and the lender. The first key criterion is that the homeowner must be experiencing a financial hardship. This could include a reduction in income, an increase in expenses, or other financial challenges that make it difficult to keep up with the current mortgage payments.

In addition to demonstrating financial hardship, borrowers must also meet certain loan-to-value (LTV) ratio requirements. The LTV ratio is calculated by dividing the outstanding loan balance by the current market value of the property. Santander typically requires an LTV ratio of 80% or less for loan modifications. This means that the borrower must have at least 20% equity in the property.

Another important criterion is the borrower's credit history. While Santander may consider loan modifications for borrowers with less-than-perfect credit, a strong credit history can improve the chances of approval. Borrowers should be prepared to provide documentation of their credit history, including recent credit reports and scores.

Furthermore, Santander may require borrowers to complete a trial modification period before approving a permanent loan modification. During this trial period, the borrower must demonstrate their ability to make the modified payments on time and in full. This helps the lender assess the borrower's commitment to the new payment plan and their overall financial stability.

Lastly, borrowers must provide thorough documentation of their financial situation, including proof of income, expenses, and assets. This documentation helps Santander evaluate the borrower's eligibility for a loan modification and determine the appropriate terms of the modification.

In summary, to qualify for a Santander loan modification, homeowners must demonstrate financial hardship, meet specific LTV ratio requirements, have a strong credit history, successfully complete a trial modification period, and provide comprehensive financial documentation. By meeting these criteria, borrowers can increase their chances of obtaining a loan modification that helps them manage their mortgage payments more effectively.

Exploring Santander's Bridging Loan Options: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Application Process: Steps involved in applying for a loan modification with Santander

To initiate the loan modification process with Santander, borrowers must first gather all necessary documentation. This typically includes proof of income, such as pay stubs or tax returns, as well as evidence of financial hardship, like medical bills or job loss notices. Borrowers should also have their loan account information and a clear understanding of the type of modification they are seeking.

Once the required documents are collected, borrowers can reach out to Santander's customer service department to inquire about the loan modification process. A representative will likely guide them through the initial steps and provide information on the available modification options. Borrowers may be asked to submit their application and supporting documents electronically or via mail.

After submitting the application, borrowers should expect a review period during which Santander will evaluate their financial situation and determine their eligibility for a loan modification. This process may involve credit checks and verification of the provided documentation. Borrowers may be contacted by a loan modification specialist who will work with them to find a suitable solution.

If approved, borrowers will receive a loan modification agreement outlining the new terms of their loan. This agreement should be reviewed carefully, and borrowers should ensure they understand all changes before signing. Once the agreement is signed and returned, Santander will finalize the modification, and the new terms will take effect.

Throughout the process, borrowers should maintain open communication with Santander and respond promptly to any requests for additional information. Keeping track of submission dates and following up on the status of the application can also help ensure a smooth and timely process.

Exploring Santander's Loan Options: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Types of Modifications: Different kinds of loan modifications Santander offers, such as rate changes or term extensions

Santander offers various types of loan modifications to assist borrowers in managing their financial obligations. One common modification is a rate change, which can involve either a temporary or permanent adjustment to the interest rate on the loan. This can help borrowers who are struggling with high monthly payments or those who want to take advantage of lower market rates.

Another modification option is a term extension, which involves increasing the length of time the borrower has to repay the loan. This can result in lower monthly payments, making it more manageable for borrowers who are experiencing financial difficulties. However, it's important to note that extending the term of a loan may result in paying more interest over the life of the loan.

In addition to rate changes and term extensions, Santander may also offer other modification options such as principal forbearance or a balloon payment. Principal forbearance involves temporarily suspending or reducing the principal payments on the loan, while a balloon payment allows the borrower to make a large lump sum payment at the end of the loan term instead of regular monthly payments.

It's important for borrowers to carefully consider the pros and cons of each modification option before making a decision. While loan modifications can provide temporary relief, they may also have long-term financial implications. Borrowers should consult with a financial advisor or loan officer to determine the best course of action for their specific situation.

Explore related products

![]()

Benefits and Drawbacks: Advantages and potential downsides of modifying a loan with Santander

Modifying a loan with Santander can offer several benefits, particularly for borrowers facing financial difficulties. One significant advantage is the potential for lower monthly payments, which can provide immediate financial relief. This is especially helpful for those who have experienced a reduction in income or an increase in expenses. Additionally, loan modifications may extend the repayment term, giving borrowers more time to repay the debt and reducing the pressure of looming deadlines.

Another benefit of modifying a loan with Santander is the possibility of avoiding late fees and penalties. By restructuring the loan, borrowers can get back on track with their payments and prevent further financial strain caused by missed deadlines. Furthermore, loan modifications can sometimes result in a lower interest rate, which can save borrowers money over the long term and make the loan more manageable.

However, there are also potential drawbacks to consider when modifying a loan with Santander. One common disadvantage is the impact on the borrower's credit score. Loan modifications can sometimes be reported as a negative event on credit reports, which may lower the borrower's credit score and make it more difficult to obtain credit in the future. Additionally, extending the repayment term can result in paying more interest over the life of the loan, even if the monthly payments are lower.

Another potential downside is that loan modifications may not always be available or may come with certain conditions. Borrowers may need to demonstrate financial hardship or meet specific eligibility criteria to qualify for a loan modification. Furthermore, the process of applying for and obtaining a loan modification can be time-consuming and may require extensive documentation and paperwork.

In conclusion, while modifying a loan with Santander can offer significant benefits such as lower monthly payments and the avoidance of late fees, it is essential to weigh these advantages against the potential drawbacks, including the impact on credit scores and the possibility of paying more interest over time. Borrowers should carefully consider their financial situation and long-term goals before deciding whether a loan modification is the right option for them.

Explore related products

![]()

Customer Reviews: Experiences and feedback from customers who have undergone loan modifications with Santander

Santander has a mixed reputation when it comes to loan modifications, as evidenced by customer reviews and feedback. While some customers have reported positive experiences with the bank's loan modification process, others have expressed frustration and dissatisfaction.

One common complaint among customers is the lengthy and complicated application process. Many have reported that it took several months to complete the modification, with some even stating that they had to resubmit their application multiple times due to missing or incorrect documentation. This can be particularly frustrating for customers who are already struggling to make their loan payments and are seeking a modification to alleviate their financial burden.

On the other hand, some customers have praised Santander for their helpful and responsive customer service. They have reported that the bank's representatives were knowledgeable and patient, taking the time to explain the modification process and answer their questions. These positive experiences suggest that Santander is capable of providing good service to its customers, even in complex situations like loan modifications.

Another issue that has been raised by customers is the lack of transparency in the modification process. Some have reported that they were not informed about the status of their application or the criteria used to evaluate it, which can lead to uncertainty and anxiety. This lack of communication can make it difficult for customers to plan their finances and make informed decisions about their loan.

In conclusion, customer reviews of Santander's loan modification process reveal a mixed bag of experiences. While some customers have had positive interactions with the bank, others have faced challenges and frustrations. Santander would do well to address these issues by streamlining their application process, improving communication with customers, and ensuring that their representatives are equipped to provide helpful and accurate information. By doing so, they could improve their reputation and provide better service to their customers.

Frequently asked questions

Yes, Santander does offer loan modification options to help customers who are experiencing financial difficulties.

Santander provides modification options for various types of loans, including mortgages, personal loans, and auto loans.

To apply for a loan modification at Santander, you can contact their customer service department or visit a local branch to discuss your options and begin the application process.

Eligibility criteria for a loan modification at Santander may vary depending on the type of loan and the specific circumstances of the borrower. Generally, borrowers must demonstrate financial hardship and provide documentation to support their application.

The potential benefits of a loan modification at Santander include lower monthly payments, reduced interest rates, extended repayment terms, and avoiding foreclosure or repossession.