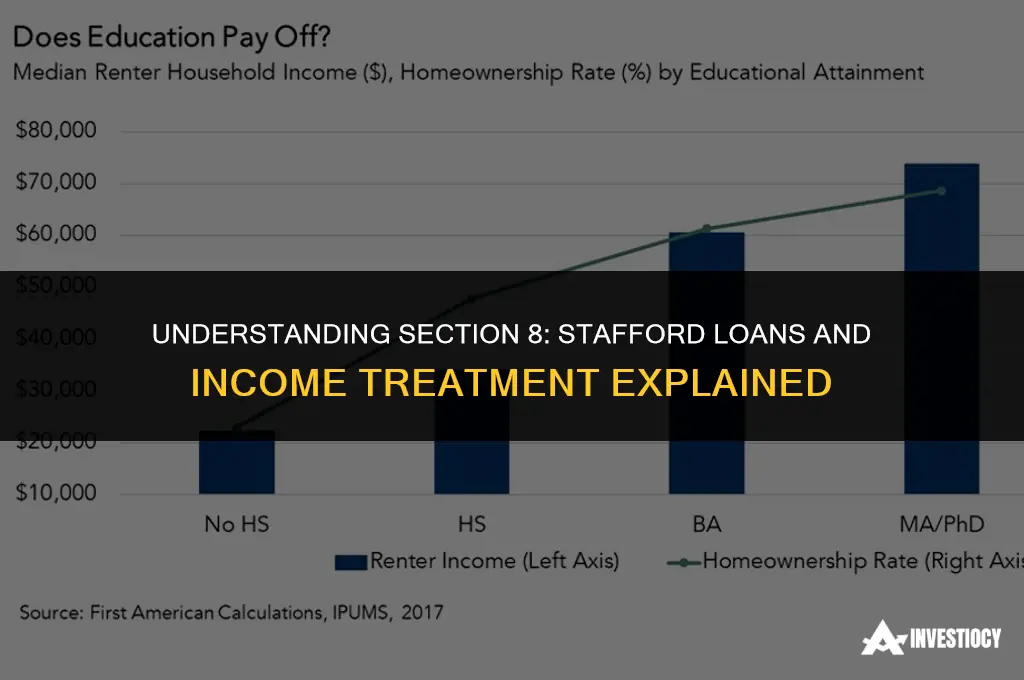

When examining the question of whether Section 8 treats Stafford loans as income, it's essential to understand the nuances of both Section 8 housing assistance and Stafford loans. Section 8, also known as the Housing Choice Voucher Program, is a federal initiative that provides rental assistance to low-income families, enabling them to afford decent housing. On the other hand, Stafford loans are a type of federal student loan designed to help students cover the cost of their education. The intersection of these two programs raises important questions about how financial aid for education impacts eligibility for housing assistance. Specifically, the inquiry into whether Stafford loans are considered income under Section 8 guidelines is a critical one, as it can significantly affect the ability of students and low-income individuals to secure affordable housing while pursuing their educational goals.

Explore related products

What You'll Learn

- Definition of Income: Understanding how Section 8 defines income is crucial for determining if Stafford loans are included

- Types of Financial Aid: Differentiating between grants, loans, and other forms of financial aid to see where Stafford loans fit

- Section 8 Income Calculation: How income is calculated under Section 8 rules and whether loan disbursements are counted

- Impact on Eligibility: Exploring how the inclusion or exclusion of Stafford loans as income affects eligibility for Section 8 benefits

- Policy Implications: Discussing the broader policy implications of treating Stafford loans as income under Section 8 guidelines

![]()

Definition of Income: Understanding how Section 8 defines income is crucial for determining if Stafford loans are included

Understanding how Section 8 defines income is crucial for determining if Stafford loans are included. Section 8 of the Housing Act of 1937, as amended, provides rental assistance to low-income families through the Section 8 Housing Choice Voucher Program. The definition of income under this program is broad and includes various sources of monetary compensation.

The program's definition of income is critical because it directly impacts the eligibility of applicants and the amount of rental assistance they can receive. Generally, income includes wages, salaries, commissions, bonuses, tips, and other forms of compensation for personal services. It also encompasses income from investments, such as interest, dividends, and capital gains, as well as income from businesses, partnerships, or sole proprietorships.

In the context of Stafford loans, which are a type of federal student loan, the question arises as to whether the proceeds from these loans are considered income under Section 8. Stafford loans are designed to help students cover the cost of higher education and are typically awarded based on financial need. Unlike grants, loans must be repaid, usually with interest, after the student graduates or leaves school.

To determine if Stafford loans are included as income under Section 8, one must carefully examine the program's regulations and guidelines. The U.S. Department of Housing and Urban Development (HUD), which administers the Section 8 program, provides detailed information on what constitutes income for eligibility purposes. According to HUD's guidelines, income includes all forms of compensation, regardless of whether it is taxable or nontaxable, and regardless of whether it is received in cash or in kind.

In conclusion, while Stafford loans are not typically considered income for tax purposes, they may be included as income under Section 8 of the Housing Act. This is because the definition of income under Section 8 is broader and encompasses various forms of monetary compensation, including loans. Therefore, individuals who receive Stafford loans and are applying for Section 8 rental assistance should be aware of this potential impact on their eligibility and the amount of assistance they can receive.

Exploring Scotland's Financial Relationship with the UK: Loan Insights

You may want to see also

Explore related products

![]()

Types of Financial Aid: Differentiating between grants, loans, and other forms of financial aid to see where Stafford loans fit

Financial aid for education comes in various forms, each with its own set of characteristics and implications. Grants, loans, and other forms of financial aid serve different purposes and have different impacts on a student's financial situation. Understanding these differences is crucial for navigating the complex landscape of educational financing and determining how each type of aid fits into one's overall financial strategy.

Grants are typically awarded based on financial need and do not require repayment. They are essentially gifts from the government or other organizations to help cover the cost of education. Loans, on the other hand, are borrowed funds that must be repaid with interest. They can be obtained from various sources, including the government, banks, and other financial institutions. Other forms of financial aid, such as scholarships and work-study programs, may have different eligibility criteria and requirements.

Stafford loans are a type of federal student loan that falls under the category of loans. They are designed to help students cover the cost of their education and are available to both undergraduate and graduate students. Stafford loans are typically awarded based on financial need, and the interest rates are generally lower than those of private loans. Repayment of Stafford loans begins after graduation or when the student drops below half-time enrollment.

In the context of Section 8 housing assistance, the treatment of Stafford loans as income can vary. Section 8 is a federal program that provides housing assistance to low-income families. The program is administered by local housing authorities, which have some discretion in determining how to treat different types of income. In some cases, Stafford loans may be considered as income for Section 8 purposes, which could affect a family's eligibility for housing assistance. However, in other cases, Stafford loans may be excluded from income calculations, depending on the specific policies of the local housing authority.

Understanding the nuances of how different types of financial aid are treated under various programs is essential for making informed decisions about educational financing. By differentiating between grants, loans, and other forms of financial aid, individuals can better navigate the complexities of the financial aid system and maximize their opportunities for securing the resources they need to achieve their educational goals.

Exploring SBI's Education Loan Options: No Collateral Required?

You may want to see also

Explore related products

![]()

Section 8 Income Calculation: How income is calculated under Section 8 rules and whether loan disbursements are counted

Under Section 8 of the Housing Act, income calculations are crucial for determining eligibility and rent subsidies. The process involves assessing various sources of income, including wages, salaries, and certain types of assistance. However, when it comes to student loans, such as Stafford loans, the treatment is nuanced.

Stafford loans, which are a form of federal student aid, are generally not considered income under Section 8 rules. This is because they are loans that must be repaid, rather than grants or scholarships that provide outright financial support. As a result, when calculating income for Section 8 purposes, loan disbursements are typically excluded.

It's important to note that while Stafford loans themselves are not counted as income, any interest accrued on these loans may be considered income if it is forgiven or discharged. This is because forgiven interest is essentially a form of financial benefit that increases the borrower's net worth.

In practice, this means that individuals who receive Stafford loans can still qualify for Section 8 assistance, as long as their other sources of income meet the program's requirements. This exclusion of loan disbursements from income calculations can be particularly beneficial for students and recent graduates who are struggling to make ends meet while repaying their loans.

To summarize, Section 8 income calculations do not include Stafford loan disbursements as income, but may consider forgiven interest as a form of financial benefit. This distinction is important for understanding how student loans impact eligibility for housing assistance programs.

Exploring Scotiabank's Consolidation Loan Options: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Impact on Eligibility: Exploring how the inclusion or exclusion of Stafford loans as income affects eligibility for Section 8 benefits

The impact of Stafford loans on eligibility for Section 8 benefits is a critical aspect to consider for individuals seeking housing assistance. Section 8, also known as the Housing Choice Voucher Program, provides aid to low-income families, the elderly, and the disabled to help them afford decent, safe, and sanitary housing in the private market. When determining eligibility, the program takes into account the applicant's income, which includes various sources such as wages, pensions, and certain types of loans.

Stafford loans, which are a form of federal student aid, can influence an individual's eligibility for Section 8 benefits. These loans are typically awarded based on financial need and can cover tuition, fees, room, and board. The key question is whether the income received from a Stafford loan is counted towards the total income when assessing eligibility for housing assistance. If the loan is considered income, it could potentially push an applicant over the income threshold, making them ineligible for Section 8 benefits.

To explore this further, it's essential to understand the specific guidelines set by the U.S. Department of Housing and Urban Development (HUD), which administers the Section 8 program. HUD has established clear criteria for what constitutes income and how it should be calculated. Generally, income includes any amounts received from employment, self-employment, welfare, social security, pensions, and other sources. However, there are certain exclusions and deductions that can be applied, such as medical expenses and child care costs.

In the case of Stafford loans, HUD has specific rules regarding how they are treated. According to HUD guidelines, Stafford loans are not considered income for the purposes of determining eligibility for Section 8 benefits. This means that the funds received from a Stafford loan do not need to be reported as income on the Section 8 application, and they will not affect the applicant's eligibility for housing assistance.

This exclusion is significant because it allows individuals who are pursuing higher education to access housing assistance without being penalized for receiving student aid. It recognizes the unique financial circumstances of students and ensures that they are not unfairly disadvantaged when seeking affordable housing. By understanding this aspect of the Section 8 program, applicants can better navigate the eligibility requirements and increase their chances of securing housing assistance.

Unlocking the Potential: Section 184 Loans and Rental Income

You may want to see also

Explore related products

![]()

Policy Implications: Discussing the broader policy implications of treating Stafford loans as income under Section 8 guidelines

Treating Stafford loans as income under Section 8 guidelines has significant policy implications that extend beyond the immediate financial calculations. One of the primary concerns is the potential disincentive for low-income students to pursue higher education. If their loans are counted as income, they may become ineligible for Section 8 housing assistance, which could force them to choose between affording their education and maintaining a roof over their heads. This could lead to a decrease in college enrollment rates among disadvantaged populations, exacerbating existing educational inequalities.

Furthermore, this policy could create a perverse incentive for students to take on more debt. If the income from loans is used to calculate Section 8 eligibility, students might be tempted to borrow more than they need in order to qualify for housing assistance. This could result in a higher overall debt burden for low-income students, making it more difficult for them to achieve financial stability after graduation.

The policy also raises questions about the fairness of treating different types of income equally. Stafford loans are intended to be a form of financial aid, not a source of income. By counting them as income, the policy could be seen as penalizing students for receiving the assistance they need to attend college. This could lead to a broader discussion about the definition of income and how different sources of funding should be treated under Section 8 guidelines.

In addition, the policy could have unintended consequences for the housing market. If students are forced to choose between education and housing, they may be more likely to seek out alternative housing arrangements, such as subletting or living in overcrowded conditions. This could lead to an increase in housing instability and a decrease in the overall quality of life for low-income students.

Ultimately, the policy implications of treating Stafford loans as income under Section 8 guidelines are complex and multifaceted. While the policy may be intended to ensure that students are not receiving duplicate benefits, it could have a range of unintended consequences that could ultimately harm the very populations it is meant to assist. As such, it is important to carefully consider the broader implications of this policy and to explore alternative approaches that could better support low-income students in their pursuit of higher education and stable housing.

How SAP Implementation Impacts Loan Processes and Financial Management

You may want to see also

Frequently asked questions

No, Section 8 does not treat Stafford loans as income. Stafford loans are considered educational loans and are generally not counted as income for Section 8 housing assistance purposes.

Section 8 determines income eligibility based on the household's gross income, which includes wages, salaries, tips, commissions, overtime, bonuses, and other forms of earned income. It also considers unearned income such as interest, dividends, and certain types of disability benefits. However, educational loans like Stafford loans are excluded from this calculation.

Under Section 8, most forms of financial assistance that provide cash or cash equivalents to the household are considered income. This includes welfare benefits, unemployment compensation, and certain types of disability benefits. However, educational loans, such as Stafford loans, are not considered income as they are intended for educational expenses rather than general household use.