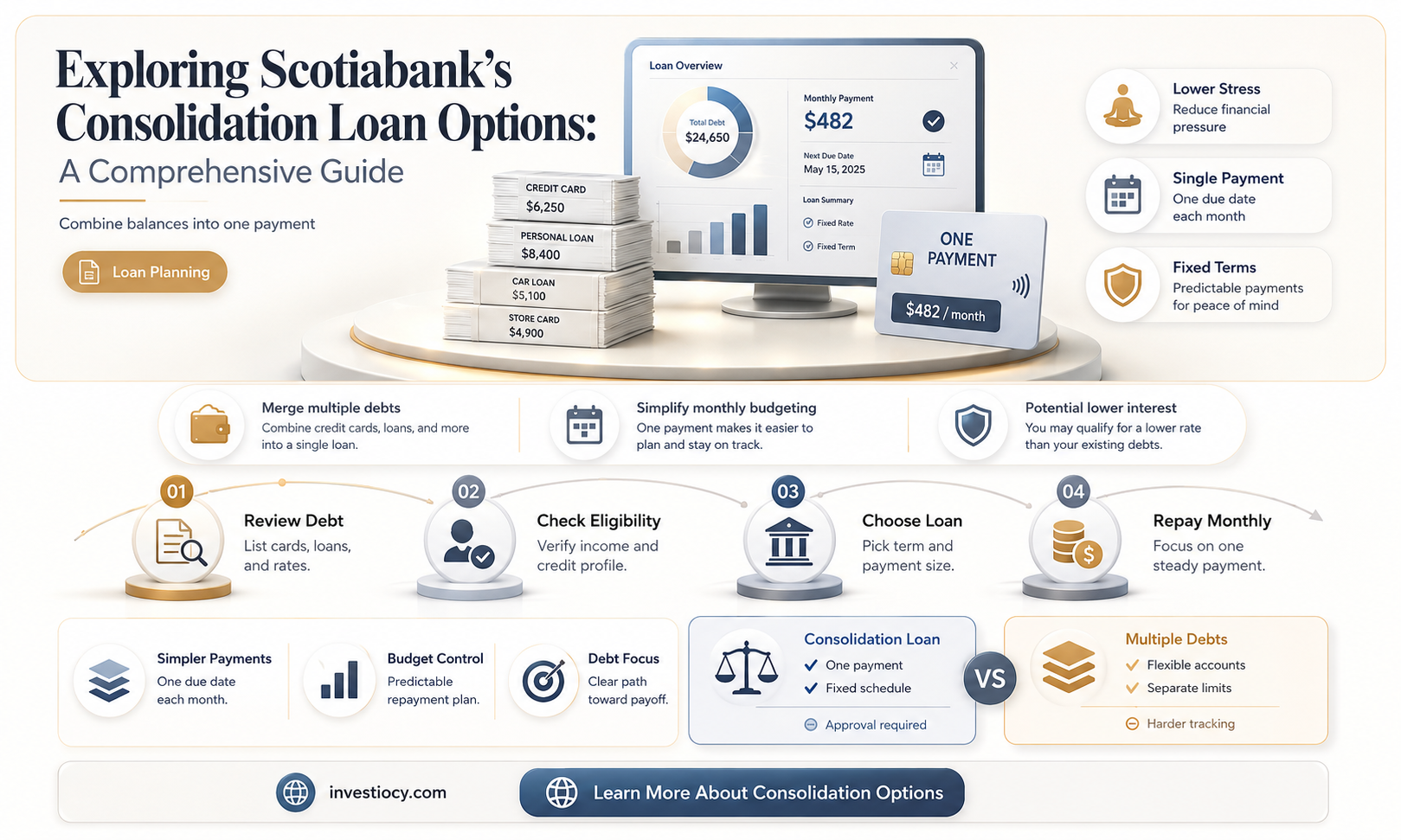

Scotiabank, one of Canada's major financial institutions, offers a variety of loan products to its customers. Among these, consolidation loans are a popular option for individuals looking to manage their debt more effectively. A consolidation loan allows borrowers to combine multiple debts into a single loan with one monthly payment, often at a lower interest rate. This can simplify financial management and potentially save money on interest charges. Scotiabank's consolidation loans are designed to help customers achieve financial stability by providing a clear path to pay off their debts.

| Characteristics | Values |

|---|---|

| Loan Type | Consolidation Loan |

| Lender | Scotiabank |

| Purpose | To combine multiple debts into a single loan |

| Interest Rate | Varies based on credit score and loan terms |

| Loan Term | Typically ranges from 1 to 7 years |

| Loan Amount | Depends on the total debt being consolidated |

| Fees | May include origination fees, late payment fees, and prepayment penalties |

| Credit Score | Minimum credit score requirements may apply |

| Repayment | Monthly payments over the loan term |

| Benefits | Simplifies debt management, potentially lower interest rates |

| Drawbacks | May extend the repayment period, possible fees and penalties |

| Eligibility | Must meet Scotiabank's lending criteria, including income and credit history |

| Application | Can be done online, in-person, or over the phone |

| Approval Time | Varies, but typically within a few business days |

| Funding Time | Funds are usually disbursed within a week of approval |

| Customer Service | Available through various channels including phone, email, and online chat |

| Additional Tools | Scotiabank may offer financial planning tools and resources |

Explore related products

What You'll Learn

- Scotiabank's Consolidation Loan Options: Exploring the types of consolidation loans offered by Scotiabank

- Eligibility Criteria: Understanding the requirements to qualify for a consolidation loan at Scotiabank

- Application Process: Step-by-step guide on how to apply for a consolidation loan with Scotiabank

- Interest Rates and Terms: Details on the interest rates, repayment terms, and any associated fees

- Benefits and Drawbacks: Analyzing the advantages and potential downsides of consolidating loans with Scotiabank

![]()

Scotiabank's Consolidation Loan Options: Exploring the types of consolidation loans offered by Scotiabank

Scotiabank offers several consolidation loan options to help customers manage their debt more effectively. One of the primary options is a personal loan, which can be used to consolidate various types of debt, including credit card balances, store cards, and other unsecured loans. These loans typically have fixed interest rates and terms, allowing borrowers to budget their monthly payments more easily.

Another option provided by Scotiabank is a home equity loan or line of credit. This type of loan leverages the equity in a borrower's home to secure a lower interest rate compared to unsecured personal loans. Home equity loans can be an attractive option for those with significant home equity and a need to consolidate larger amounts of debt.

For customers with multiple high-interest debts, Scotiabank also offers debt consolidation programs. These programs involve working with a financial advisor to create a tailored plan for paying off debts. The advisor may negotiate with creditors to reduce interest rates or waive fees, and the borrower makes a single monthly payment to the program rather than multiple payments to different creditors.

In addition to these options, Scotiabank provides educational resources and tools to help customers understand their debt and make informed decisions about consolidation. These resources include online calculators, budgeting guides, and one-on-one consultations with financial experts.

When considering a consolidation loan from Scotiabank, it's important for borrowers to carefully evaluate their financial situation and goals. They should consider factors such as their credit score, the total amount of debt they wish to consolidate, and their ability to make regular payments. By choosing the right consolidation option, borrowers can simplify their finances, reduce their monthly payments, and potentially save money on interest over time.

Unveiling the Truth: Does Schwab Loan Shares?

You may want to see also

Explore related products

$26.64

![]()

Eligibility Criteria: Understanding the requirements to qualify for a consolidation loan at Scotiabank

To qualify for a consolidation loan at Scotiabank, applicants must meet several key eligibility criteria. Firstly, a strong credit score is essential, as it demonstrates the borrower's ability to manage debt responsibly. Scotiabank typically looks for a credit score of at least 650, although higher scores may result in more favorable loan terms.

In addition to credit score, income stability is another crucial factor. Applicants must provide proof of a steady income, which can come from employment, self-employment, or other reliable sources. This ensures that the borrower has the means to repay the loan over the agreed-upon term.

Debt-to-income ratio is also a significant consideration. Scotiabank prefers applicants with a lower debt-to-income ratio, as this indicates a lower risk of default. To calculate this ratio, add up all monthly debt payments (including credit cards, loans, and mortgages) and divide by gross monthly income. A ratio of 36% or lower is generally considered acceptable.

Furthermore, Scotiabank may require collateral for larger consolidation loans. This could be in the form of a home, vehicle, or other valuable assets. Providing collateral can help secure the loan and may result in a lower interest rate.

Lastly, applicants must be at least 18 years old and a Canadian resident or non-resident with a valid work permit. They must also have a Scotiabank account or be willing to open one.

Understanding these eligibility criteria can help potential borrowers determine if they qualify for a consolidation loan at Scotiabank. It's essential to review these requirements carefully and ensure all necessary documentation is prepared before applying.

SAP Warning: Impact on Sub and Unsub Loans Explained

You may want to see also

Explore related products

![]()

Application Process: Step-by-step guide on how to apply for a consolidation loan with Scotiabank

To apply for a consolidation loan with Scotiabank, you'll need to follow a series of steps that ensure you meet the bank's requirements and understand the terms of the loan. Here's a step-by-step guide to help you navigate the application process smoothly.

First, gather all the necessary documents and information. This typically includes proof of income, such as pay stubs or tax returns, as well as identification documents like a driver's license or passport. You'll also need to provide details about your existing debts, including the total amount you wish to consolidate and the names of your current creditors.

Next, visit the Scotiabank website or a local branch to initiate the application process. You can either apply online or in person, depending on your preference. If you choose to apply online, you'll be guided through a series of questions and prompted to upload your supporting documents. If you prefer to apply in person, a Scotiabank representative will assist you with filling out the application and submitting the required paperwork.

Once your application is submitted, Scotiabank will review your information and conduct a credit check. This is a standard procedure to assess your creditworthiness and determine whether you qualify for the loan. If you're approved, Scotiabank will provide you with a loan offer outlining the terms, including the interest rate, repayment period, and any associated fees.

Before accepting the loan offer, it's crucial to review the terms carefully and ensure you understand the implications. Consider factors such as the total cost of the loan, the monthly payment amount, and any potential penalties for early repayment. If you have any questions or concerns, don't hesitate to reach out to Scotiabank for clarification.

Finally, if you decide to accept the loan offer, you'll need to sign the agreement and return it to Scotiabank. Once the bank receives your signed agreement, they will disburse the loan funds and begin the process of paying off your existing creditors. It's important to continue making payments on your debts until you receive confirmation that they have been paid in full.

By following these steps and providing accurate information, you can increase your chances of successfully applying for a consolidation loan with Scotiabank. Remember to be patient and thorough throughout the process, and don't hesitate to seek assistance if needed.

Exploring Santander's Bridging Loan Options: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Interest Rates and Terms: Details on the interest rates, repayment terms, and any associated fees

Scotiabank offers consolidation loans with competitive interest rates that vary based on the borrower's creditworthiness and the specific terms of the loan. The interest rates for these loans typically range from a low of around 5% to a high of approximately 20%, with the exact rate determined by the bank's underwriting criteria. Borrowers with excellent credit scores are more likely to qualify for the lower end of this range, while those with fair or poor credit may be offered higher rates.

The repayment terms for Scotiabank's consolidation loans are flexible, allowing borrowers to choose from a variety of payment schedules that best suit their financial situation. Loan terms can range from 1 to 7 years, with the option to make monthly, bi-weekly, or weekly payments. Borrowers can also choose to make additional payments or pay off the loan in full at any time without incurring prepayment penalties.

In addition to interest rates and repayment terms, Scotiabank's consolidation loans may come with certain fees. These can include an origination fee, which is typically a percentage of the loan amount, as well as late payment fees and NSF fees for returned payments. Borrowers should carefully review the loan agreement to understand all the fees associated with the loan and how they can be avoided.

One unique feature of Scotiabank's consolidation loans is the option to consolidate multiple types of debt, including credit card debt, personal loans, and lines of credit. This can help borrowers simplify their finances and potentially save money on interest charges. Additionally, Scotiabank offers a debt consolidation calculator on its website, which can help borrowers estimate their potential savings and determine if a consolidation loan is right for them.

Overall, Scotiabank's consolidation loans can be a valuable tool for borrowers looking to manage their debt more effectively. By understanding the interest rates, repayment terms, and associated fees, borrowers can make informed decisions about whether a consolidation loan is a good fit for their financial situation.

Exploring SBI's Education Loan Options: No Collateral Required?

You may want to see also

![]()

Benefits and Drawbacks: Analyzing the advantages and potential downsides of consolidating loans with Scotiabank

Consolidating loans with Scotiabank can offer several benefits, including simplified financial management and potential cost savings. By combining multiple debts into a single loan, borrowers can streamline their monthly payments, reducing the likelihood of missed payments and late fees. Additionally, Scotiabank may offer competitive interest rates, especially for those with good credit, which can lower the overall cost of borrowing.

However, there are also potential drawbacks to consider. Consolidating loans may result in a longer repayment period, which could increase the total amount paid in interest over time. Furthermore, if the new loan is secured by collateral, such as a home or vehicle, there is a risk of losing that asset if payments are not made as agreed. It's also important to note that consolidating loans does not address the underlying financial habits that led to debt accumulation in the first place, and without changes to spending and saving behaviors, borrowers may find themselves in debt again.

To maximize the benefits of consolidating loans with Scotiabank, it's crucial to carefully review the terms and conditions of the new loan, including the interest rate, repayment period, and any associated fees. Borrowers should also consider seeking financial counseling to develop a comprehensive plan for managing their debt and improving their overall financial health. By weighing the advantages and potential downsides, individuals can make an informed decision about whether consolidating loans with Scotiabank is the right choice for their financial situation.

Exploring the Impact of SAP on Unsubsidized Loan Dynamics

You may want to see also

Frequently asked questions

Yes, Scotiabank does offer consolidation loans. These loans are designed to help customers combine multiple debts into a single, more manageable payment.

A consolidation loan from Scotiabank can provide several benefits, including a lower interest rate, a single monthly payment, and the convenience of managing only one account. This can help simplify your finances and potentially save you money on interest charges.

To apply for a consolidation loan at Scotiabank, you can visit their website, call their customer service number, or visit a local branch. You will need to provide information about your current debts, income, and credit history.

To be eligible for a Scotiabank consolidation loan, you must have a good credit score, a steady income, and be a Canadian resident. You may also need to provide collateral, such as a home or vehicle, depending on the amount of the loan.

While a consolidation loan from Scotiabank can offer many benefits, there are also potential drawbacks to consider. These may include a longer repayment term, which could result in paying more interest over time, and the possibility of losing assets if you default on the loan. It's important to carefully review the terms and conditions before applying.