The topic of whether a SAP warning affects sub and unsub loans is a complex one, involving intricate details of financial regulations and loan agreements. SAP warnings, typically issued by regulatory bodies, are designed to alert financial institutions to potential risks or non-compliance issues within their operations. These warnings can have far-reaching implications, impacting not only the institution's reputation but also its financial stability and ability to offer loans. In the context of sub and unsub loans, which are specialized financial products, a SAP warning could potentially lead to increased scrutiny, changes in loan terms, or even the discontinuation of these loan types. Understanding the relationship between SAP warnings and sub and unsub loans requires a deep dive into the regulatory framework governing these financial instruments, as well as an analysis of the potential consequences for both lenders and borrowers.

| Characteristics | Values |

|---|---|

| SAP Warning | A system alert indicating potential issues with loan processing |

| Affects | Both subscribed (sub) and unsubscribed (unsub) loans |

| Impact on Loans | May cause delays or require additional verification steps |

| Frequency | Occurs periodically, based on system updates or changes |

| Resolution | Typically requires intervention from IT or loan processing teams |

| Importance | High, as it can affect the timely disbursement of funds |

| Notification | Usually sent to loan officers or system administrators |

| Causes | Could be due to software glitches, data inconsistencies, or security concerns |

| Duration | Varies, but can last from a few hours to several days |

| Prevention | Regular system maintenance and updates can help minimize occurrences |

| Documentation | Detailed logs and reports are usually generated for each warning |

| Training | Staff training is essential to handle and resolve SAP warnings effectively |

| Compliance | Ensuring compliance with financial regulations is crucial to prevent such warnings |

| Costs | Can incur significant costs due to delayed loan processing and resource allocation |

| Customer Impact | May affect customer satisfaction and trust in the lending institution |

Explore related products

$19.95 $19.95

What You'll Learn

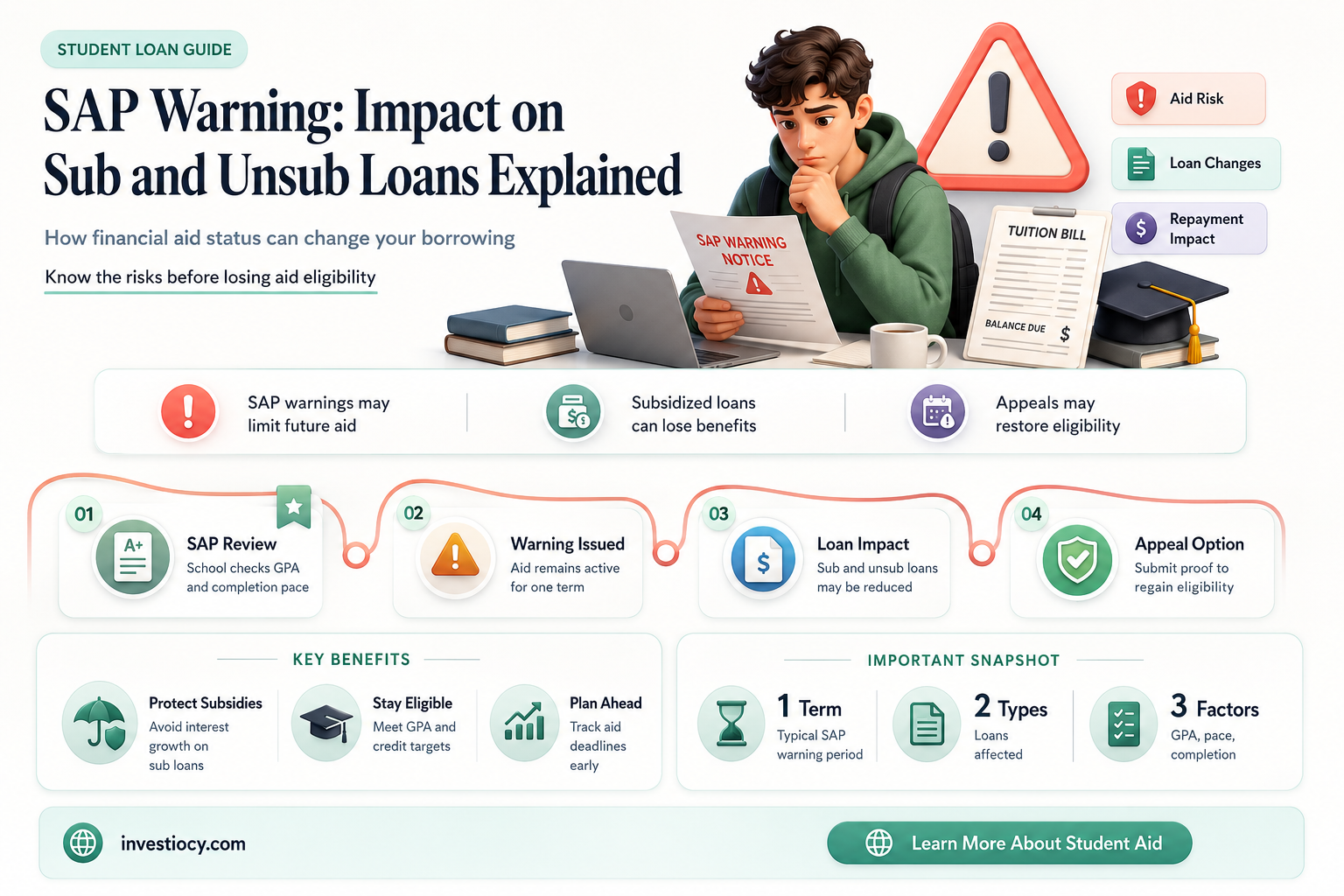

- Definition of SAP Warning: Understanding what constitutes a SAP warning and its implications on financial products

- Impact on Subsidized Loans: Analyzing how SAP warnings influence the terms and availability of subsidized loan options

- Effect on Unsubsidized Loans: Examining the changes in unsubsidized loan structures and interest rates following a SAP warning

- Credit Score Considerations: Discussing how SAP warnings might alter credit score requirements for both sub and unsub loans

- Lender and Borrower Perspectives: Insights into how lenders and borrowers navigate loan processes post-SAP warning issuance

![]()

Definition of SAP Warning: Understanding what constitutes a SAP warning and its implications on financial products

A SAP warning is a regulatory alert issued by financial authorities to inform investors about potential risks associated with a particular financial product or service. These warnings are typically based on identified patterns of misconduct, systemic issues, or emerging threats in the financial market. Understanding what constitutes a SAP warning is crucial for investors, as it can significantly impact their decision-making process regarding various financial products, including sub and unsub loans.

SAP warnings are generally issued by government agencies or regulatory bodies responsible for overseeing financial markets. They serve as a preventive measure to protect investors from potential harm and maintain market integrity. These warnings can cover a wide range of financial products, such as securities, derivatives, insurance policies, and loans. In the context of sub and unsub loans, a SAP warning may highlight risks related to predatory lending practices, unfair terms, or misleading marketing strategies.

The implications of a SAP warning on financial products can be far-reaching. For investors, it serves as a red flag, signaling the need for heightened caution and due diligence. It may prompt them to reconsider their investment decisions, seek additional information, or consult with financial advisors. For financial institutions, a SAP warning can lead to reputational damage, increased regulatory scrutiny, and potential legal consequences. It may also result in changes to their business practices, product offerings, or marketing strategies to address the identified risks.

In the case of sub and unsub loans, a SAP warning could have significant implications for both borrowers and lenders. Borrowers may need to be more vigilant about the terms and conditions of these loans, ensuring they understand the risks and potential consequences of default. Lenders, on the other hand, may need to reassess their underwriting criteria, disclosure practices, and collection methods to ensure compliance with regulatory requirements and avoid potential legal issues.

Overall, understanding the definition and implications of a SAP warning is essential for navigating the complex financial landscape. It empowers investors to make informed decisions, helps financial institutions mitigate risks, and contributes to the overall stability and integrity of the financial market. By staying informed about SAP warnings and their potential impact on various financial products, including sub and unsub loans, market participants can better protect themselves and make more prudent investment choices.

Exploring Santander's Loan Modification Options: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Impact on Subsidized Loans: Analyzing how SAP warnings influence the terms and availability of subsidized loan options

SAP warnings can significantly impact the landscape of subsidized loans. When a company receives a warning from SAP, it often triggers a review of the company's financial health and creditworthiness. This can lead to a reassessment of the terms and conditions of any existing subsidized loans, potentially resulting in higher interest rates or stricter repayment terms. In some cases, the availability of subsidized loans may be reduced or even eliminated if the company is deemed too high a risk.

One of the key factors influencing the impact of SAP warnings on subsidized loans is the severity of the warning itself. Minor infractions may result in a slap on the wrist and a requirement to implement corrective measures, while more serious violations could lead to a downgrade in the company's credit rating. This, in turn, can make it more difficult for the company to secure favorable loan terms.

Another important consideration is the company's overall financial position. If a company is already struggling financially, a SAP warning could be the final nail in the coffin, making it nearly impossible to secure any form of financing, subsidized or otherwise. On the other hand, a company with a strong financial foundation may be able to weather the storm and continue to access subsidized loans, albeit at potentially less favorable terms.

In addition to the direct impact on loan terms and availability, SAP warnings can also have indirect consequences. For example, a company that receives a warning may see its stock price decline, which can further erode its financial stability and make it more difficult to secure loans. Additionally, the negative publicity associated with a SAP warning can damage a company's reputation, making it less attractive to potential lenders.

To mitigate the impact of SAP warnings on subsidized loans, companies should take proactive steps to address any compliance issues and implement robust internal controls. This can help to demonstrate to lenders that the company is taking steps to rectify the situation and reduce the risk of future violations. Additionally, companies should maintain open lines of communication with their lenders, keeping them informed of any developments and working collaboratively to find solutions that benefit both parties.

In conclusion, SAP warnings can have a significant impact on the terms and availability of subsidized loans. Companies that receive such warnings should take immediate action to address the underlying issues and work with their lenders to find mutually beneficial solutions. By doing so, they can help to minimize the negative consequences of a SAP warning and maintain access to the financing they need to operate and grow.

Exploring Santander's Loan Options: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Effect on Unsubsidized Loans: Examining the changes in unsubsidized loan structures and interest rates following a SAP warning

Following a SAP warning, the landscape of unsubsidized loans undergoes significant transformations. Lenders, in response to the warning, may reassess their risk tolerance and adjust loan structures accordingly. This could lead to changes in interest rates, repayment terms, and eligibility criteria for unsubsidized loans. Borrowers may find themselves facing higher interest rates or more stringent qualification requirements, making it more challenging to secure an unsubsidized loan.

One potential effect of a SAP warning on unsubsidized loans is an increase in interest rates. Lenders may perceive a higher risk associated with lending after a SAP warning and, as a result, charge higher interest rates to compensate for this perceived risk. This could make unsubsidized loans more expensive for borrowers, potentially deterring some from pursuing this type of financing.

Another possible impact is a shift in loan structures. Lenders might opt for shorter repayment terms or require more frequent payments to mitigate the risk highlighted by the SAP warning. This could result in higher monthly payments for borrowers, affecting their cash flow and financial planning. Additionally, lenders may impose stricter eligibility criteria, such as higher credit score requirements or more substantial income verification, making it more difficult for some borrowers to qualify for unsubsidized loans.

The changes in unsubsidized loan structures and interest rates following a SAP warning can have broader implications for the financial market. Borrowers who are unable to secure unsubsidized loans may turn to other forms of financing, such as credit cards or personal loans, potentially increasing the demand for these alternatives. This shift in demand could lead to changes in the pricing and availability of other financial products, creating a ripple effect throughout the market.

In conclusion, a SAP warning can have a profound impact on the unsubsidized loan market, leading to changes in interest rates, loan structures, and eligibility criteria. Borrowers may face higher costs and more stringent qualification requirements, while lenders adjust their lending practices to manage perceived risks. These changes can have far-reaching consequences for the financial market as a whole, highlighting the importance of understanding the potential effects of a SAP warning on unsubsidized loans.

Exploring Santander's Bridging Loan Options: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Credit Score Considerations: Discussing how SAP warnings might alter credit score requirements for both sub and unsub loans

SAP warnings can significantly impact credit score requirements for both subsidized and unsubsidized loans. Typically, SAP warnings indicate potential issues with loan repayment, prompting lenders to reassess the creditworthiness of borrowers. This reassessment often leads to stricter credit score criteria, making it more challenging for individuals with SAP warnings to secure loans.

For subsidized loans, which are designed to assist borrowers with lower incomes, SAP warnings may result in a more rigorous evaluation of the borrower's financial situation. Lenders may require a higher credit score to mitigate the risk associated with the warning. Additionally, they might impose more stringent conditions, such as a co-signer or collateral, to ensure repayment.

In the case of unsubsidized loans, which are available to a broader range of borrowers, SAP warnings can still lead to increased scrutiny. Lenders may raise the minimum credit score requirement or adjust the loan terms to reflect the heightened risk. This could include higher interest rates or shorter repayment periods, making the loan more expensive for the borrower.

It's crucial for borrowers with SAP warnings to understand these implications and take proactive steps to improve their credit scores. This may involve disputing errors on their credit reports, paying bills on time, and reducing debt levels. By addressing the underlying issues that led to the SAP warning, borrowers can enhance their chances of securing favorable loan terms.

In summary, SAP warnings can alter credit score requirements for both subsidized and unsubsidized loans, leading to stricter criteria and potentially higher costs for borrowers. Understanding these implications and taking steps to improve creditworthiness can help mitigate the impact of SAP warnings on loan eligibility and terms.

Exploring Financial Features: Does SAP Include Loan Management?

You may want to see also

Explore related products

![]()

Lender and Borrower Perspectives: Insights into how lenders and borrowers navigate loan processes post-SAP warning issuance

Lenders and borrowers alike face a complex landscape when navigating loan processes after the issuance of an SAP warning. For lenders, the warning serves as a critical signal to reassess risk profiles and adjust lending strategies accordingly. This may involve tightening credit criteria, increasing interest rates, or even halting certain types of loans altogether. Borrowers, on the other hand, may find themselves in a precarious position, with reduced access to credit and potentially unfavorable terms.

One key challenge for lenders is balancing the need to mitigate risk with the desire to maintain a competitive edge. In the post-SAP warning environment, lenders must carefully evaluate each loan application, considering factors such as the borrower's credit history, debt-to-income ratio, and overall financial stability. This may lead to a more nuanced approach to lending, with lenders offering tailored solutions to borrowers based on their individual circumstances.

For borrowers, the SAP warning may serve as a wake-up call to reassess their financial situation and explore alternative lending options. This could involve seeking out non-traditional lenders, such as peer-to-peer lending platforms or credit unions, which may offer more favorable terms. Borrowers may also need to be more proactive in managing their credit, by monitoring their credit reports, disputing errors, and taking steps to improve their credit score.

In addition to these challenges, both lenders and borrowers must also navigate the regulatory landscape, which can be complex and ever-changing. Compliance with relevant laws and regulations is essential, and failure to do so can result in significant penalties. As such, it is crucial for both parties to stay informed about the latest regulatory developments and to ensure that their lending practices are in line with current requirements.

Ultimately, the SAP warning serves as a reminder of the importance of responsible lending and borrowing practices. By working together, lenders and borrowers can navigate the post-warning landscape and find mutually beneficial solutions that meet their financial needs while also mitigating risk.

Exploring the Impact of SAP on Unsubsidized Loan Dynamics

You may want to see also

Frequently asked questions

SAP warnings do not directly affect subscription loans as they are typically related to software compliance and licensing issues. Subscription loans are financial agreements separate from software usage rights.

No, SAP warnings are unrelated to unsubscribe loan terms. Unsubscribe loans are usually governed by financial agreements and regulations, not software compliance warnings.

SAP warnings themselves do not impose financial penalties that would affect loan repayments. However, if a company is found non-compliant with SAP licensing, it may face separate financial penalties from SAP, which could indirectly impact its financial situation and ability to repay loans.

SAP warnings do not influence the interest rates on subscription or unsubscribe loans. Interest rates are determined by financial institutions based on market conditions, creditworthiness, and other financial factors.

Companies should not be overly concerned about SAP warnings when applying for subscription or unsubscribe loans, as these warnings are unrelated to the loan application process. However, it is always advisable to ensure compliance with all software licenses to avoid any potential legal or financial issues.