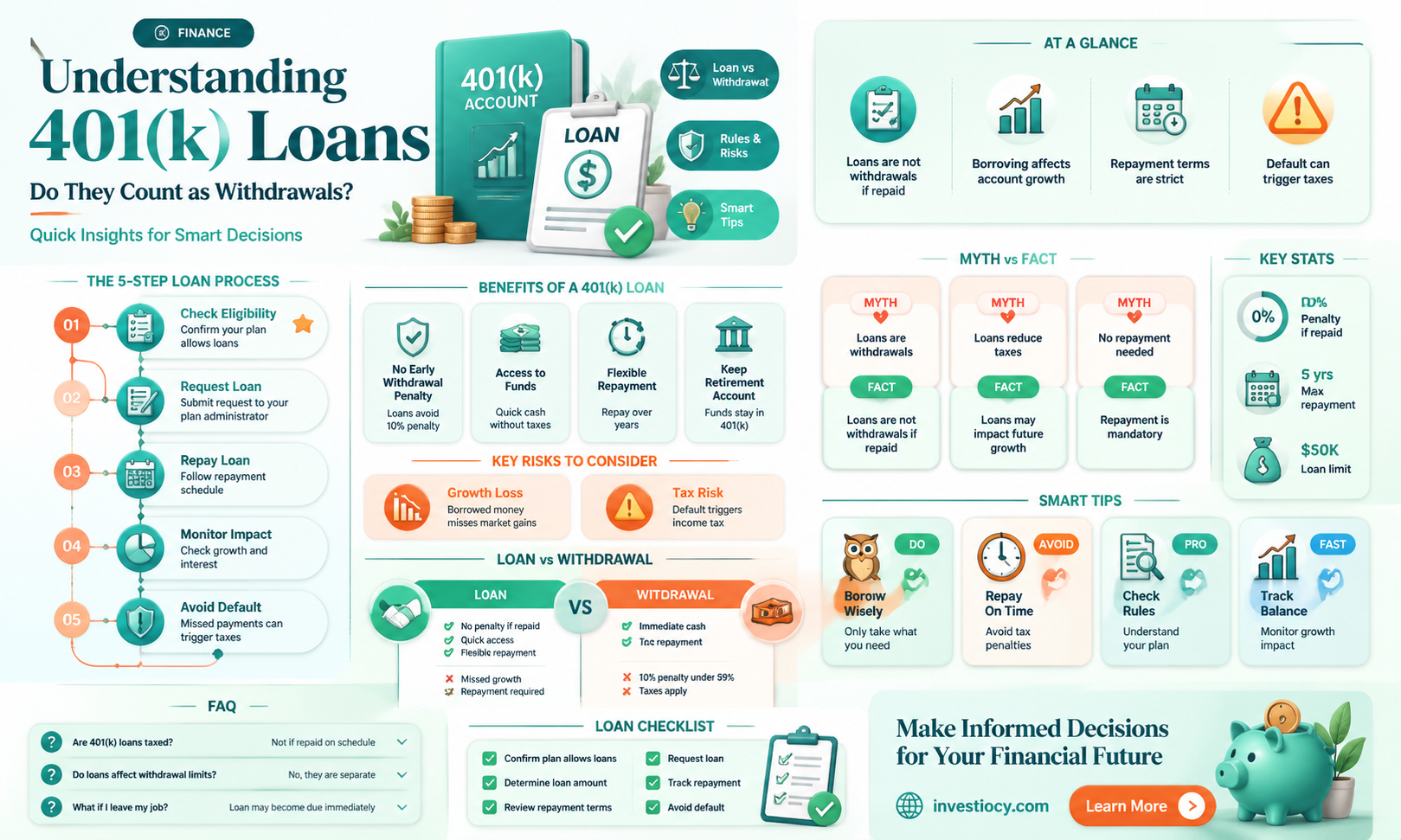

Taking a loan from a 401(k) plan is a common financial strategy for individuals who need access to funds for various purposes, such as home purchases, education expenses, or debt consolidation. However, it's essential to understand the implications of such a loan on one's retirement savings. While a 401(k) loan allows participants to borrow money from their own retirement accounts without incurring taxes or penalties, it does not constitute a withdrawal in the traditional sense. Instead, it's a temporary reduction in the account balance that must be repaid, typically through payroll deductions, within a specified period. This repayment process helps to restore the account balance over time, minimizing the long-term impact on retirement savings. Nonetheless, it's crucial to consider the potential consequences of reducing one's retirement funds, even temporarily, and to weigh the benefits of a 401(k) loan against other financial options.

| Characteristics | Values |

|---|---|

| Definition | A 401(k) loan is a type of withdrawal where you borrow money from your 401(k) account. |

| Interest Rates | Typically lower than personal loans or credit cards, often around 4-6%. |

| Repayment Terms | Usually 5 years or less, with payments deducted directly from your paycheck. |

| Impact on Retirement Savings | Reduces the amount of money in your 401(k) account, potentially affecting your retirement savings. |

| Tax Implications | Generally, no taxes are withheld when you take a 401(k) loan, but you may need to pay taxes on the loan amount if you don't repay it according to the terms. |

| Eligibility | Depends on your employer's plan rules, but most plans allow participants to borrow up to 50% of their vested account balance, up to a maximum of $50,000. |

| Application Process | Usually involves filling out a loan application form and providing proof of identity and income. |

| Approval Time | Can vary, but often takes a few days to a few weeks. |

| Fees | May include an origination fee, typically around 1-2% of the loan amount, and possibly an annual maintenance fee. |

| Prepayment Penalties | Rarely, but some plans may charge a penalty for paying off the loan early. |

| Default Consequences | If you default on the loan, the unpaid balance may be treated as a taxable distribution, and you may face penalties. |

| Alternatives | Other options for accessing retirement funds include 401(k) withdrawals, IRA loans, or personal loans. |

| Advantages | Can provide quick access to funds at a relatively low interest rate, and repayments can help rebuild your 401(k) balance. |

| Disadvantages | Reduces your retirement savings, may impact your credit score, and can lead to penalties if not repaid properly. |

| Considerations | Carefully review your employer's plan rules and consult with a financial advisor before taking a 401(k) loan. |

Explore related products

What You'll Learn

- Definition of 401(k) Loan: A loan taken from a 401(k) plan is considered a withdrawal, but with specific conditions

- Interest and Repayment: The loan accrues interest, which is repaid along with the principal, typically through payroll deductions

- Impact on Retirement Savings: Borrowing from a 401(k) reduces the amount available for retirement and may affect investment growth

- Tax Implications: Loans from 401(k) plans are generally tax-free if repaid on time, but penalties may apply for early withdrawal

- Alternatives to 401(k) Loans: Other options, such as personal loans or credit cards, may be considered to avoid impacting retirement savings

![]()

Definition of 401(k) Loan: A loan taken from a 401(k) plan is considered a withdrawal, but with specific conditions

A 401(k) loan is a financial mechanism that allows individuals to borrow money from their 401(k) retirement plan. This type of loan is considered a withdrawal from the plan, but it comes with specific conditions that differentiate it from a traditional withdrawal. Unlike regular withdrawals, which are typically subject to penalties and taxes, a 401(k) loan can be taken without incurring these charges, provided certain criteria are met.

One of the key conditions of a 401(k) loan is that it must be repaid within a specified period, usually five years. This repayment period can be extended if the loan is used to purchase a primary residence. The interest rate on a 401(k) loan is typically lower than that of a personal loan, as it is essentially borrowing from oneself. However, it's important to note that while the loan is outstanding, the borrowed funds are not earning investment returns, which can impact the overall growth of the retirement account.

Another unique aspect of a 401(k) loan is that it does not require a credit check, as the borrower is essentially lending to themselves. This can be advantageous for individuals with poor credit who may not qualify for a traditional loan. However, it's crucial to remember that defaulting on a 401(k) loan can have severe consequences, including penalties and taxes on the unpaid balance.

In summary, a 401(k) loan is a withdrawal from a retirement plan that is treated differently from regular withdrawals due to its specific conditions. It offers a way to access funds without incurring penalties and taxes, provided the loan is repaid within the designated timeframe. While it can be a useful financial tool, it's essential to understand the implications and responsibilities that come with borrowing from one's retirement savings.

The Impact of Loans on Your Net Worth: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Interest and Repayment: The loan accrues interest, which is repaid along with the principal, typically through payroll deductions

Taking a loan from a 401(k) plan involves borrowing money from your own retirement savings. This process is different from a traditional loan because you are essentially lending to yourself. One crucial aspect to consider is the interest and repayment structure of such loans.

The interest on a 401(k) loan typically accrues over time, similar to any other loan. However, the interest rate is often lower than what you might find with other types of loans, such as personal loans or credit cards. This is because the loan is secured by your retirement savings. The accrued interest is repaid along with the principal amount, usually through payroll deductions. This means that a portion of your paycheck will be automatically deducted to cover the loan repayment.

It's important to note that the repayment terms can vary depending on the specific 401(k) plan and the loan agreement. Some plans may offer more flexible repayment options, while others might have stricter terms. Additionally, if you leave your job or experience a hardship, the repayment terms might change, potentially requiring a lump-sum payment or accelerating the repayment schedule.

One unique aspect of 401(k) loans is that they do not count as withdrawals from your retirement account. This means that you can take a loan without incurring the early withdrawal penalty that typically applies if you take money out of your 401(k) before age 59½. However, it's essential to understand that while the loan itself is not a withdrawal, the money you borrow is no longer invested in your retirement savings, which could impact your long-term financial growth.

In summary, when considering a 401(k) loan, it's crucial to carefully review the interest and repayment terms to ensure that you can comfortably manage the payments and understand the potential impact on your retirement savings.

Understanding the Impact of Loans on Life Insurance Premiums

You may want to see also

Explore related products

![]()

Impact on Retirement Savings: Borrowing from a 401(k) reduces the amount available for retirement and may affect investment growth

Borrowing from a 401(k) plan can have significant implications for retirement savings. When an individual takes a loan from their 401(k), they are essentially reducing the amount of money that is available for retirement. This reduction can have a compounding effect over time, as the borrowed funds are no longer invested and growing. For example, if someone borrows $10,000 from their 401(k) at an interest rate of 4%, they will need to repay $10,400. However, if that same $10,000 had remained invested in the 401(k) plan, it could have grown to a much larger amount over time, depending on the investment returns.

The impact of borrowing from a 401(k) on retirement savings can be further exacerbated by the potential for reduced investment growth. When funds are withdrawn from a 401(k) plan, they are no longer able to benefit from the power of compounding returns. This can be particularly detrimental for individuals who are in the early stages of their careers, as they have less time for their investments to grow. Additionally, borrowing from a 401(k) can lead to a false sense of security, as individuals may feel that they have more money available for retirement than they actually do.

It is also important to consider the potential tax implications of borrowing from a 401(k). While the loan itself is not taxable, the interest paid on the loan may be. This can further reduce the overall amount of money that is available for retirement. Additionally, if an individual is unable to repay the loan, the outstanding balance may be treated as a taxable distribution, which can have significant tax consequences.

In conclusion, borrowing from a 401(k) plan can have a substantial impact on retirement savings, as it reduces the amount of money available for retirement and may affect investment growth. It is important for individuals to carefully consider the potential consequences of borrowing from their 401(k) before making a decision.

Explore related products

![]()

Tax Implications: Loans from 401(k) plans are generally tax-free if repaid on time, but penalties may apply for early withdrawal

Loans from 401(k) plans can be a valuable financial tool, but understanding their tax implications is crucial to avoid unexpected penalties. Generally, if you repay a 401(k) loan on time, the borrowed amount is not considered a taxable withdrawal. This means you won't owe income tax on the loan proceeds, and the interest you pay on the loan is typically tax-deductible. However, if you fail to repay the loan according to the plan's terms, the unpaid balance may be treated as an early withdrawal, subjecting you to income tax and potentially a 10% early withdrawal penalty.

To avoid these penalties, it's essential to follow the repayment schedule outlined in your 401(k) plan. Most plans require regular payments, often deducted directly from your paycheck. If you leave your job or experience a reduction in income, you may need to adjust your repayment strategy to ensure you don't default on the loan. In some cases, you may be able to roll over the loan balance to an IRA or another 401(k) plan to avoid early withdrawal penalties, but this should be done carefully to comply with IRS regulations.

It's also important to note that while 401(k) loans can be tax-free if repaid on time, they do reduce your retirement savings. The money you borrow is taken directly from your 401(k) account, which means it's no longer invested and earning returns. This can have a significant impact on your long-term retirement goals, especially if you're not able to repay the loan quickly. Therefore, while 401(k) loans can be a useful short-term financial solution, they should be used sparingly and with a clear understanding of their potential long-term consequences.

In summary, 401(k) loans can be tax-free if repaid on time, but they carry the risk of early withdrawal penalties if not managed properly. To avoid these penalties, it's crucial to adhere to the repayment schedule, consider the impact on your retirement savings, and explore alternative options if you're unable to repay the loan as planned. By understanding the tax implications and potential consequences of 401(k) loans, you can make informed decisions about your retirement finances.

![]()

Alternatives to 401(k) Loans: Other options, such as personal loans or credit cards, may be considered to avoid impacting retirement savings

Taking a loan from a 401(k) plan can seem like an attractive option when facing financial emergencies or needing funds for significant expenses. However, it's crucial to understand that such loans do indeed count as withdrawals, impacting retirement savings and potentially incurring penalties. To mitigate these effects, exploring alternative funding sources becomes essential. Personal loans and credit cards are viable options that can help avoid dipping into retirement funds. Personal loans typically offer fixed interest rates and repayment terms, making them a predictable and manageable choice. Credit cards, while providing more flexibility in terms of repayment, come with variable interest rates that can accumulate debt if not managed carefully. Both options, however, allow individuals to preserve their retirement savings, which is a critical aspect of long-term financial planning.

Another alternative to consider is a home equity loan or line of credit. For homeowners, this can be a cost-effective way to access funds, as these loans often come with lower interest rates compared to personal loans or credit cards. However, they require using one's home as collateral, which introduces an element of risk. Peer-to-peer lending platforms also present an innovative way to borrow money, often with competitive interest rates and flexible repayment terms. These platforms connect borrowers directly with lenders, cutting out traditional financial institutions and potentially offering more favorable conditions.

In addition to these borrowing options, individuals might consider other strategies to raise funds without impacting their retirement savings. Selling unused or unnecessary assets, such as electronics, furniture, or collectibles, can provide a quick influx of cash. Freelancing or taking on a part-time job can also generate additional income to cover expenses. For those with investments outside of their retirement accounts, liquidating some of these assets might be a preferable option to borrowing.

When evaluating these alternatives, it's important to consider the long-term implications of each choice. While borrowing options like personal loans, credit cards, and home equity loans can provide immediate financial relief, they also come with interest and repayment obligations that need to be carefully managed. Selling assets or taking on additional work might not be feasible for everyone, depending on their financial situation and personal circumstances. Ultimately, the key is to weigh the pros and cons of each alternative and choose the option that best aligns with one's financial goals and needs.

Frequently asked questions

No, taking a loan from your 401(k) does not count as a withdrawal. It is considered a loan against your retirement savings, which you are expected to repay with interest.

Potential consequences include reducing your retirement savings, incurring interest charges on the loan, and possibly affecting your investment growth. Additionally, if you leave your job, you may have to repay the loan within a short period or face penalties.

A 401(k) loan is not reported to the credit bureaus, so it does not directly impact your credit score. However, if you default on the loan, it could lead to a negative impact on your credit.

Repayment terms vary by plan but typically require repayment within five years through payroll deductions. Interest rates are usually based on the prime rate plus a margin, and the interest you pay goes back into your 401(k) account.

Yes, there is a limit. You can generally borrow up to 50% of your vested account balance, up to a maximum of $50,000. However, some plans may have different limits or restrictions.