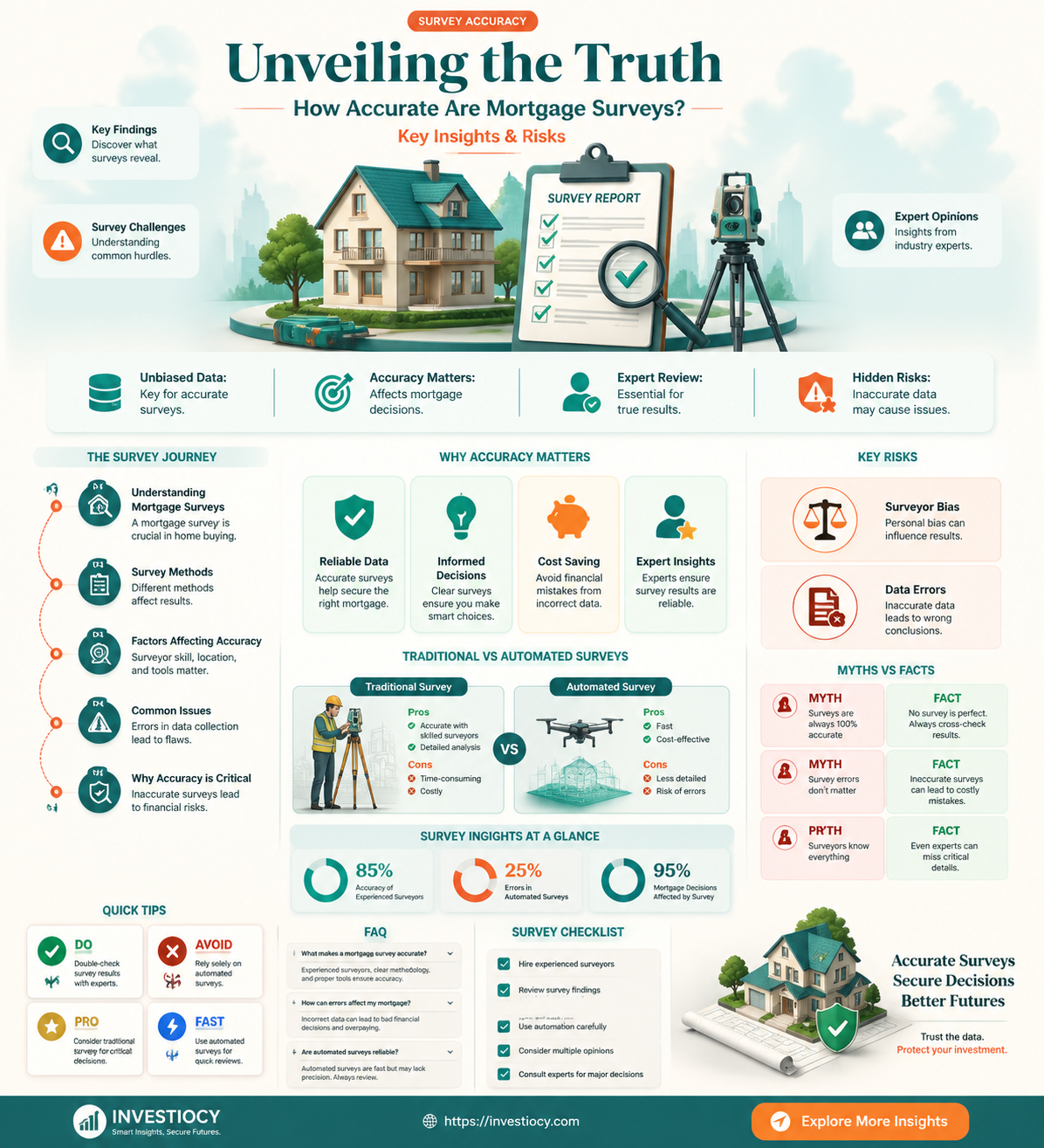

Mortgage surveys play a crucial role in the home buying process, providing lenders with valuable information about the property's value and condition. However, the accuracy of these surveys can vary depending on several factors, including the surveyor's expertise, the complexity of the property, and the specific requirements of the lender. In this paragraph, we will delve into the intricacies of mortgage surveys, exploring the methods used to conduct them, the potential sources of error, and the steps that can be taken to ensure their reliability. By understanding the nuances of mortgage surveys, prospective homebuyers can make informed decisions and navigate the often-complex world of real estate with greater confidence.

Explore related products

What You'll Learn

- Types of Surveys: Understand the different types of mortgage surveys available and their specific purposes

- Survey Costs: Explore the cost implications of various mortgage surveys and how they impact overall mortgage expenses

- Accuracy Levels: Evaluate the accuracy levels of different survey methods and technologies used in mortgage assessments

- Legal Requirements: Review the legal requirements and regulations surrounding mortgage surveys in different jurisdictions

- Impact on Mortgage Approval: Analyze how the results of mortgage surveys can influence the approval process and terms of a mortgage

![]()

Types of Surveys: Understand the different types of mortgage surveys available and their specific purposes

Mortgage surveys are crucial in the homebuying process, providing valuable information about the property's boundaries, condition, and potential issues. There are several types of mortgage surveys, each serving a specific purpose and offering varying levels of detail and accuracy. Understanding these types is essential for homebuyers to make informed decisions and ensure they are getting the most appropriate survey for their needs.

One common type of mortgage survey is the property boundary survey. This survey focuses on establishing the exact boundaries of the property, including the location of fences, walls, and other structures. It is particularly important for properties with unclear or disputed boundaries, as it can help prevent future legal issues and ensure that the buyer is aware of the property's true size and shape.

Another type of mortgage survey is the home inspection survey. This survey is more comprehensive and includes an evaluation of the property's overall condition, including the structure, roof, plumbing, electrical systems, and more. Home inspection surveys are typically required by lenders to ensure that the property is in good condition and worth the investment. They can also help buyers identify potential issues that may need to be addressed before closing on the property.

In addition to these two main types of surveys, there are also specialized surveys that may be required depending on the property's location and characteristics. For example, properties in flood-prone areas may require a flood zone survey, while properties with septic systems may need a septic inspection. These specialized surveys provide additional information that can help buyers make informed decisions and avoid potential risks.

When choosing a mortgage survey, it is important to consider the specific needs of the property and the level of detail required. Homebuyers should work with a qualified surveyor who can recommend the most appropriate type of survey based on the property's characteristics and the buyer's goals. By understanding the different types of mortgage surveys available and their specific purposes, homebuyers can ensure that they are getting the most accurate and comprehensive information about their potential new home.

Explore related products

![]()

Survey Costs: Explore the cost implications of various mortgage surveys and how they impact overall mortgage expenses

The cost of mortgage surveys can significantly impact the overall expenses associated with obtaining a mortgage. Lenders often require surveys to assess the property's value and condition, which can vary widely in cost depending on the type of survey and the property's location. For instance, a basic property valuation survey might cost a few hundred dollars, while a more comprehensive survey that includes structural assessments could cost several thousand dollars. These costs are typically borne by the borrower and can add up quickly, especially for first-time homebuyers who may not be prepared for the additional expenses.

One way to manage survey costs is to shop around for the best deal. Just as with mortgage rates, survey costs can vary between providers, so it's worth getting quotes from several different companies. Additionally, some lenders may offer discounted survey rates as part of their mortgage package, so it's important to inquire about any potential savings when comparing mortgage offers.

Another factor to consider is the potential for additional costs if the survey reveals issues with the property. For example, if the survey identifies structural problems or environmental hazards, the lender may require further inspections or repairs, which can add to the overall cost of the mortgage. In some cases, these additional costs may be negotiable, so it's important to carefully review the survey results and discuss any concerns with the lender.

Ultimately, understanding the cost implications of mortgage surveys is crucial for borrowers to make informed decisions about their mortgage options. By factoring in the potential costs of surveys and any additional expenses that may arise, borrowers can better budget for their new home and avoid unexpected financial surprises.

Explore related products

![]()

Accuracy Levels: Evaluate the accuracy levels of different survey methods and technologies used in mortgage assessments

The accuracy of mortgage surveys is paramount in ensuring that lenders have a reliable assessment of a property's value and condition. Different survey methods and technologies can yield varying levels of accuracy, and it's crucial to evaluate these to make informed decisions. Traditional survey methods, such as physical inspections by certified surveyors, are known for their high accuracy but can be time-consuming and costly. In contrast, modern technologies like automated valuation models (AVMs) and remote sensing can provide quicker and more cost-effective assessments, but their accuracy may vary depending on the quality of the data and algorithms used.

One key factor affecting the accuracy of mortgage surveys is the level of detail captured. Physical inspections allow for a thorough examination of the property, including its structural integrity, interior and exterior condition, and any potential issues that may not be visible in photographs or digital models. AVMs, on the other hand, rely on historical data and market trends to estimate property values, which may not always reflect the current condition or unique features of a specific property. Remote sensing technologies, such as satellite imagery and drones, can provide valuable insights into a property's surroundings and potential environmental risks, but they may not be able to capture the same level of detail as a physical inspection.

Another important consideration is the expertise and qualifications of the individuals conducting the surveys. Certified surveyors undergo rigorous training and are subject to strict professional standards, ensuring that their assessments are accurate and reliable. In contrast, AVMs and remote sensing technologies may not require the same level of human expertise, which can lead to potential errors or inaccuracies in the assessments. It's essential for lenders to carefully evaluate the qualifications and track record of any survey provider to ensure that they are receiving accurate and reliable information.

In addition to the survey method and technology used, the accuracy of mortgage surveys can also be influenced by external factors such as market conditions and regulatory requirements. For example, in a rapidly changing real estate market, AVMs may struggle to keep up with the latest trends and fluctuations in property values. Similarly, regulatory requirements may dictate the level of detail and accuracy required in mortgage surveys, which can impact the choice of survey method and technology.

To ensure the highest level of accuracy in mortgage surveys, lenders should consider a combination of survey methods and technologies. A physical inspection by a certified surveyor can provide a detailed and accurate assessment of the property's condition, while AVMs and remote sensing technologies can offer valuable insights into market trends and environmental também factors. By leveraging the strengths of each method, lenders can obtain a more comprehensive and accurate picture of the property, ultimately leading to more informed lending decisions.

Explore related products

![]()

Legal Requirements: Review the legal requirements and regulations surrounding mortgage surveys in different jurisdictions

Mortgage surveys are subject to a variety of legal requirements and regulations that can vary significantly depending on the jurisdiction. In the United States, for example, the Federal Housing Administration (FHA) has specific guidelines for mortgage surveys, which include requirements for the surveyor's qualifications, the scope of the survey, and the accuracy of the survey results. These guidelines are designed to ensure that mortgage surveys are conducted in a consistent and reliable manner, and that they provide an accurate representation of the property being surveyed.

In addition to federal guidelines, many states have their own laws and regulations governing mortgage surveys. These state laws may impose additional requirements on surveyors, such as licensing and registration, and may also specify certain standards for the conduct of mortgage surveys. For example, some states may require surveyors to use specific equipment or methods, or to provide certain types of information in their survey reports.

In other countries, the legal requirements for mortgage surveys may be different. In the United Kingdom, for instance, mortgage surveys are typically conducted by chartered surveyors who are regulated by the Royal Institution of Chartered Surveyors (RICS). The RICS has its own set of standards and guidelines for mortgage surveys, which are designed to ensure that surveyors provide accurate and reliable information to lenders and borrowers.

One of the key aspects of mortgage survey regulations is the requirement for accuracy. In most jurisdictions, surveyors are required to provide accurate and reliable information about the property being surveyed. This includes information about the property's boundaries, size, and condition, as well as any potential issues or defects that may affect its value or suitability for lending purposes. Surveyors who fail to provide accurate information may be subject to legal penalties, including fines or even criminal charges.

Another important aspect of mortgage survey regulations is the requirement for transparency. Surveyors are typically required to disclose any conflicts of interest or potential biases that may affect their survey results. This is designed to ensure that lenders and borrowers have confidence in the accuracy and reliability of the survey information, and that they are not misled by any hidden agendas or financial incentives.

In conclusion, the legal requirements and regulations surrounding mortgage surveys are complex and varied, and can have a significant impact on the accuracy and reliability of survey results. Surveyors must be aware of these requirements and must take steps to ensure that they comply with all applicable laws and regulations. This includes obtaining the necessary qualifications and licenses, using appropriate equipment and methods, and providing accurate and transparent information in their survey reports. By doing so, surveyors can help to ensure that mortgage surveys are conducted in a consistent and reliable manner, and that they provide valuable information to lenders and borrowers alike.

Explore related products

![]()

Impact on Mortgage Approval: Analyze how the results of mortgage surveys can influence the approval process and terms of a mortgage

Mortgage surveys play a crucial role in the mortgage approval process, as they provide lenders with valuable insights into the borrower's financial situation and creditworthiness. The results of these surveys can significantly influence the approval process and terms of a mortgage, making it essential for borrowers to understand their importance.

One of the primary ways mortgage surveys impact mortgage approval is by assessing the borrower's credit score. Lenders use credit scores to determine the borrower's ability to repay the loan, and a high credit score can lead to more favorable loan terms, such as lower interest rates and higher loan amounts. Conversely, a low credit score may result in higher interest rates, lower loan amounts, or even loan denial.

In addition to credit scores, mortgage surveys also evaluate the borrower's debt-to-income ratio, employment history, and assets. These factors help lenders determine the borrower's financial stability and ability to manage mortgage payments. For instance, a borrower with a high debt-to-income ratio may be considered a higher risk, leading to less favorable loan terms or denial.

Furthermore, mortgage surveys can also impact the approval process by identifying potential red flags, such as discrepancies in income or employment history. These red flags may prompt lenders to request additional documentation or conduct further investigations, potentially delaying the approval process.

To mitigate the impact of mortgage surveys on mortgage approval, borrowers should ensure they provide accurate and complete information. This includes reviewing their credit reports for errors, gathering necessary documentation, and being transparent about their financial situation. By doing so, borrowers can increase their chances of obtaining favorable loan terms and a smooth approval process.

In conclusion, mortgage surveys are a critical component of the mortgage approval process, and their results can significantly influence the terms of a mortgage. Borrowers should understand the importance of these surveys and take steps to ensure they provide accurate and complete information to increase their chances of obtaining favorable loan terms.

Frequently asked questions

Mortgage surveys are generally quite accurate in determining property values as they are conducted by professional surveyors who use standardized methods and consider various factors such as location, size, condition, and comparable sales in the area.

Yes, mortgage surveys can also be used for other purposes such as assessing the condition of the property, identifying potential issues or hazards, and providing information for property maintenance and improvement plans.

Factors that can affect the accuracy of a mortgage survey include the quality of the data used, the expertise and experience of the surveyor, the condition of the property at the time of the survey, and any changes in the property or surrounding area that may have occurred since the survey was conducted.

![NMLS Study Guide 2026-2027 - 5 Full-Length Practice Tests, SAFE MLO Exam Prep Secrets Book for the Mortgage Loan Originator Exam: [4th Edition]](https://m.media-amazon.com/images/I/717iHac5CwL._AC_UL320_.jpg)