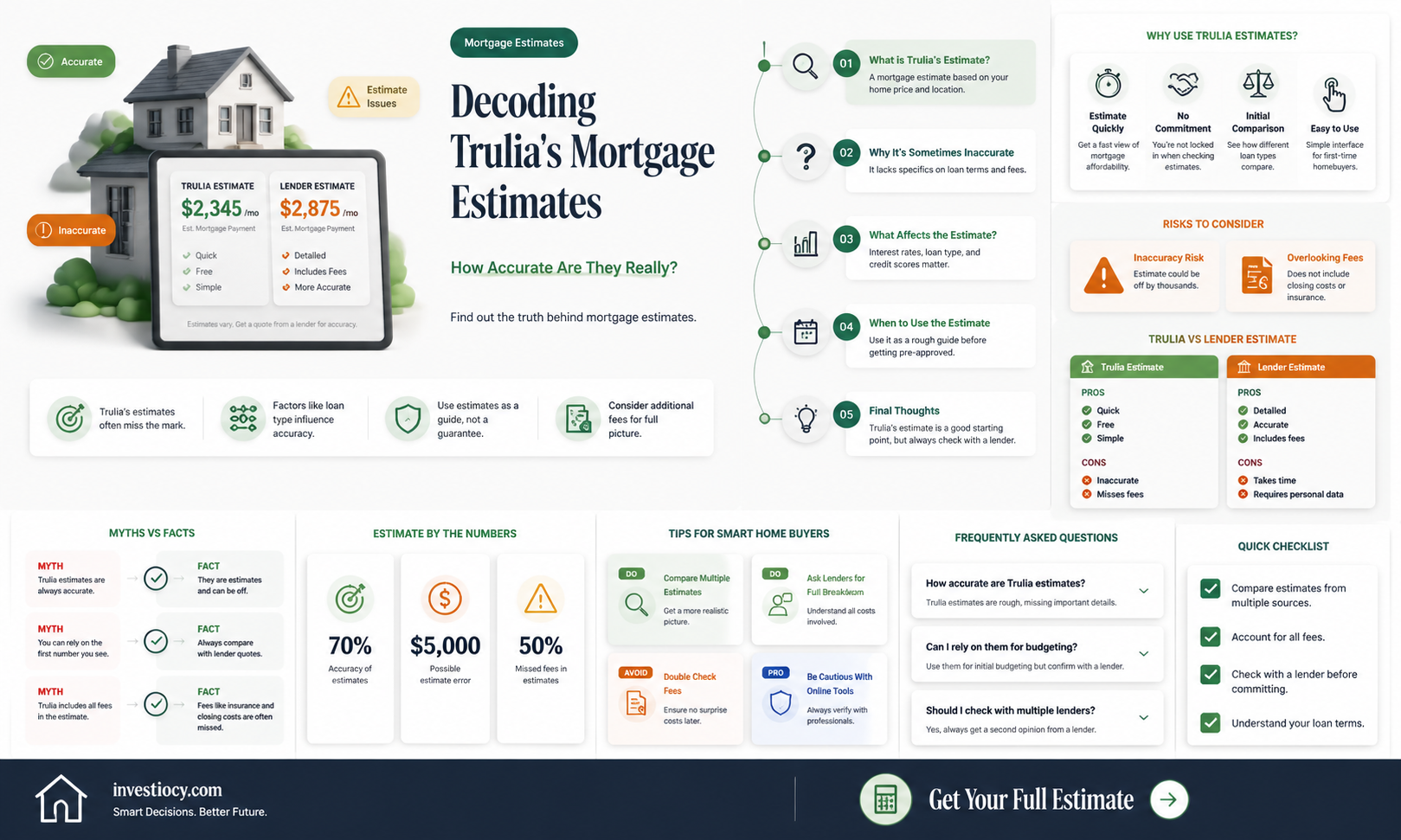

Trulia, a popular real estate website, offers mortgage estimates to help potential homebuyers understand their financing options. However, the accuracy of these estimates can vary based on several factors. Trulia's mortgage calculator takes into account the home price, down payment, loan term, and interest rate to provide an estimated monthly payment. While this can be a useful starting point, it's essential to consider that these estimates may not reflect the final mortgage amount due to fluctuations in interest rates, changes in credit scores, and additional fees or taxes. Furthermore, Trulia's estimates do not account for factors like property taxes, homeowners insurance, or HOA fees, which can significantly impact the overall cost of homeownership. Therefore, while Trulia's mortgage estimates can provide a general idea of what to expect, it's crucial for homebuyers to consult with a lender or financial advisor for a more accurate assessment of their mortgage options.

Explore related products

What You'll Learn

- Factors Influencing Estimates: Understand how credit score, debt-to-income ratio, and loan type affect mortgage estimates

- Comparison with Competitors: Analyze how Trulia's estimates compare to those from other mortgage lenders

- User Reviews and Ratings: Explore customer feedback on Trulia's mortgage estimates to gauge reliability

- Estimate Calculation Methodology: Delve into the methods and algorithms Trulia uses to generate mortgage estimates

- Potential Hidden Costs: Identify any additional fees or costs that might not be included in Trulia's initial estimates

![]()

Factors Influencing Estimates: Understand how credit score, debt-to-income ratio, and loan type affect mortgage estimates

Credit score plays a pivotal role in determining mortgage estimates. A higher credit score typically qualifies borrowers for lower interest rates, which can significantly reduce the overall cost of a mortgage. Conversely, a lower credit score may result in higher interest rates, increasing the financial burden on the borrower. For instance, a borrower with a credit score of 750 might secure a 30-year fixed mortgage at 3.5%, while a borrower with a score of 650 might only qualify for a rate of 4.5%. This difference can amount to thousands of dollars over the life of the loan.

Debt-to-income ratio is another critical factor influencing mortgage estimates. Lenders use this ratio to assess a borrower's ability to manage their monthly payments. A lower debt-to-income ratio indicates that a borrower has less debt relative to their income, making them a more attractive candidate for a mortgage. For example, a borrower with a debt-to-income ratio of 30% may be offered more favorable terms than a borrower with a ratio of 45%. It's essential for borrowers to understand this ratio and work towards reducing their debt to improve their chances of securing a better mortgage estimate.

Loan type also affects mortgage estimates. Different types of loans come with varying interest rates, terms, and eligibility criteria. For instance, FHA loans are designed for first-time homebuyers and offer lower down payment requirements, but they may come with higher interest rates compared to conventional loans. VA loans, available to veterans and active-duty military personnel, often provide more favorable terms, including lower interest rates and no down payment requirements. Borrowers should explore different loan types to find the one that best suits their financial situation and goals.

Understanding these factors can help borrowers navigate the mortgage estimation process more effectively. By improving their credit score, managing their debt-to-income ratio, and exploring different loan types, borrowers can increase their chances of securing a mortgage estimate that aligns with their financial objectives. It's crucial to approach this process with a clear understanding of these influencing factors to make informed decisions and avoid potential pitfalls.

Unveiling the Truth: How Accurate Are Mortgage Surveys?

You may want to see also

Explore related products

![]()

Comparison with Competitors: Analyze how Trulia's estimates compare to those from other mortgage lenders

Trulia's mortgage estimates are often compared to those from other major mortgage lenders to gauge their accuracy and competitiveness. When analyzing these comparisons, it's essential to consider the methodology each lender uses to generate their estimates, as well as the specific data points they consider. For instance, some lenders may factor in more comprehensive data sets, including credit scores, income levels, and property values, while others might rely on more general information.

One way to approach this comparison is to look at the average variance between Trulia's estimates and those from other lenders. This can be done by collecting a sample of mortgage estimates from Trulia and competing lenders for similar properties and borrowers. By calculating the average difference between these estimates, you can get a sense of how closely Trulia's numbers align with industry standards.

Another important aspect to consider is the transparency of each lender's estimation process. Some lenders may provide detailed breakdowns of how they arrived at their estimates, while others may be less forthcoming. Trulia, for example, is known for providing clear explanations of their methodology, which can help borrowers understand the basis for their estimates.

In addition to comparing the estimates themselves, it's also valuable to look at user reviews and ratings for each lender. This can give you insight into how satisfied borrowers are with the accuracy and reliability of the estimates they received. By considering both the quantitative data and qualitative feedback, you can form a more comprehensive picture of how Trulia's mortgage estimates compare to those from other lenders.

Ultimately, the accuracy of Trulia's mortgage estimates can only be fully assessed by comparing them to actual loan terms offered by lenders. Borrowers should always shop around and obtain multiple quotes to ensure they are getting the best possible deal. By doing so, they can better evaluate the accuracy and usefulness of Trulia's estimates in the context of their individual financial situations.

Explore related products

![]()

User Reviews and Ratings: Explore customer feedback on Trulia's mortgage estimates to gauge reliability

To gauge the reliability of Trulia's mortgage estimates, it's essential to delve into user reviews and ratings. These firsthand accounts provide invaluable insights into the accuracy and usefulness of the platform's financial projections. By examining the experiences of others, potential users can make informed decisions about whether to trust Trulia's mortgage estimates for their own financial planning.

When exploring user reviews, it's crucial to consider the overall sentiment and specific feedback provided. Look for patterns in the comments, such as recurring praises or complaints about the accuracy of the estimates. Pay attention to the context in which users are providing their feedback, as this can offer additional clues about the reliability of the estimates. For instance, users who have successfully secured mortgages based on Trulia's estimates may be more likely to provide positive feedback, while those who have encountered discrepancies may be more critical.

In addition to user reviews, it's beneficial to examine ratings from reputable sources, such as financial advisors or industry experts. These professionals can offer a more objective assessment of Trulia's mortgage estimates, taking into account factors such as the platform's methodology, data sources, and track record. By combining user reviews with expert ratings, potential users can gain a more comprehensive understanding of the accuracy and reliability of Trulia's mortgage estimates.

When evaluating the reliability of Trulia's mortgage estimates, it's also important to consider the platform's transparency and accountability. Look for information about how Trulia calculates its estimates, what data sources it uses, and how it addresses user concerns or complaints. A transparent and accountable platform is more likely to provide accurate and reliable estimates, as it has a vested interest in maintaining user trust and satisfaction.

Ultimately, the key to determining the accuracy of Trulia's mortgage estimates lies in a thorough examination of user reviews and ratings. By carefully considering the experiences and opinions of others, potential users can make informed decisions about whether to rely on Trulia's financial projections for their own mortgage planning.

Explore related products

![]()

Estimate Calculation Methodology: Delve into the methods and algorithms Trulia uses to generate mortgage estimates

Trulia's mortgage estimate calculation methodology is a complex process that involves several key steps. First, Trulia gathers data from a variety of sources, including public records, real estate listings, and financial institutions. This data is then used to create a comprehensive database of property values, mortgage rates, and other relevant information.

Next, Trulia uses a proprietary algorithm to analyze this data and generate mortgage estimates. This algorithm takes into account a number of factors, including the property's value, the borrower's credit score, and the current mortgage rates. The algorithm also considers the borrower's income and debt-to-income ratio, as well as other financial factors that may impact their ability to qualify for a mortgage.

Once the algorithm has generated a mortgage estimate, Trulia then applies a series of filters to refine the results. These filters are designed to ensure that the estimates are accurate and realistic, and that they take into account the unique characteristics of each property and borrower.

Finally, Trulia presents the mortgage estimates to users in a clear and easy-to-understand format. The estimates are typically displayed as a range of possible mortgage payments, rather than a single fixed amount. This allows users to get a better sense of the potential costs associated with a particular property and mortgage.

Overall, Trulia's mortgage estimate calculation methodology is a sophisticated process that involves the collection and analysis of a large amount of data. While the estimates are generally accurate, it's important for users to understand that they are based on a number of assumptions and may not reflect the actual costs of a mortgage.

Explore related products

![]()

Potential Hidden Costs: Identify any additional fees or costs that might not be included in Trulia's initial estimates

Trulia's mortgage estimates provide a useful starting point for prospective homebuyers, but it's essential to be aware of potential hidden costs that may not be included in these initial calculations. One significant cost that is often overlooked is the home inspection fee. A thorough home inspection is crucial to identify any structural issues or necessary repairs, and this service typically comes with a fee ranging from $300 to $500, depending on the size and location of the property.

Another hidden cost that can catch buyers off guard is the appraisal fee. Lenders often require a professional appraisal to ensure the property's value aligns with the purchase price. This fee can vary from $300 to $600, depending on the complexity of the appraisal and the location of the property. Additionally, if the appraisal value comes in lower than the purchase price, the buyer may need to pay for a second appraisal or renegotiate the terms of the sale, which can lead to additional costs and delays.

Closing costs are another area where hidden fees can lurk. While Trulia's estimates may include some closing costs, it's important to be aware of additional fees that may be tacked on, such as attorney fees, title insurance, and recording fees. These costs can vary significantly depending on the location and complexity of the transaction, so it's crucial to review the closing disclosure carefully to identify any unexpected charges.

Furthermore, buyers should be aware of potential costs associated with homeowners association (HOA) fees, property taxes, and insurance. While these costs may not be hidden in the traditional sense, they can be easily overlooked or underestimated when calculating the total cost of homeownership. HOA fees can range from a few hundred to several thousand dollars per year, depending on the community and amenities offered. Property taxes and insurance costs can also vary significantly based on the location and value of the property.

To avoid being caught off guard by hidden costs, it's essential for homebuyers to do their due diligence and research all potential fees associated with the purchase. This includes reviewing the closing disclosure, asking the lender about any additional costs, and researching local property taxes and HOA fees. By being proactive and informed, buyers can better prepare for the true cost of homeownership and avoid unexpected financial surprises down the road.

Frequently asked questions

Trulia's mortgage estimates are generally accurate as they are based on current market data and user-provided information. However, they should be used as a guideline rather than an exact figure, as actual rates can vary based on individual circumstances.

Factors that can affect the accuracy of Trulia's mortgage estimates include changes in interest rates, credit score variations, loan-to-value ratios, and other economic conditions. Additionally, the estimates assume a standard loan term and do not account for unique situations or special financing options.

While Trulia's mortgage estimates can be a helpful starting point, it's important to consult with a lender or financial advisor for a more personalized assessment. They can provide a more accurate estimate based on your specific financial situation and help you understand the terms and conditions of your loan.

To improve the accuracy of Trulia's mortgage estimates, you can input more detailed information about your finances, such as your credit score, income, and debt. Additionally, you can explore different loan types and terms to find the best fit for your needs.

Yes, Trulia's mortgage estimates are updated regularly to reflect changes in the market. However, it's always a good idea to check the date of the estimate and verify the information with a lender or financial advisor to ensure you have the most current and accurate information.