The topic of U.S. mortgage debt is a significant one, as it represents a substantial portion of the country's overall debt. As of the latest data available, the total outstanding mortgage debt in the United States stands at approximately $12 trillion. This figure has been steadily increasing over the years, driven by factors such as rising home prices, low interest rates, and increased borrowing by homeowners. The size of the mortgage debt market has implications for the broader economy, influencing everything from consumer spending to the stability of the financial system. Understanding the scale and trends in mortgage debt is crucial for policymakers, economists, and individuals alike, as it can impact decisions related to housing, investment, and economic policy.

Explore related products

$14.12 $22.99

What You'll Learn

![]()

Total Mortgage Debt Outstanding

The total mortgage debt outstanding in the United States is a staggering figure that reflects the scale of the country's housing market and the reliance on credit for homeownership. As of the latest data available, the total mortgage debt outstanding stands at approximately $11.5 trillion. This number represents the cumulative amount of money borrowed by homeowners through mortgages, including both purchase mortgages and refinance loans.

To put this figure into perspective, it's worth noting that the total mortgage debt outstanding has more than doubled since the turn of the century. In 2000, the figure stood at around $4.9 trillion, meaning that it has increased by more than $6.6 trillion over the past two decades. This growth can be attributed to a number of factors, including rising home prices, low interest rates, and changes in lending practices that have made it easier for people to borrow larger amounts of money.

The total mortgage debt outstanding is not only a reflection of the housing market, but also an indicator of the overall health of the economy. When mortgage debt levels are high, it can be a sign of a booming housing market and a strong economy. However, it can also be a cause for concern, as high levels of debt can make households more vulnerable to economic shocks and can contribute to financial instability.

One of the key drivers of the increase in total mortgage debt outstanding has been the trend towards larger mortgage balances. The average mortgage balance has increased significantly over the past two decades, from around $100,000 in 2000 to more than $200,000 today. This increase can be attributed to a number of factors, including rising home prices, larger loan sizes, and the growing popularity of jumbo loans.

The distribution of mortgage debt across different types of loans is also worth noting. The majority of mortgage debt is held in the form of conventional loans, which are loans that are not insured or guaranteed by the government. However, a significant portion of mortgage debt is also held in the form of government-backed loans, such as FHA loans and VA loans. These loans are designed to make homeownership more accessible to certain groups of borrowers, such as first-time homebuyers and veterans.

In conclusion, the total mortgage debt outstanding in the United States is a complex and multifaceted issue that reflects a range of economic and social factors. While it is a sign of a strong housing market and a growing economy, it also raises concerns about the sustainability of high levels of debt and the potential for financial instability. As such, it is an important topic for policymakers, lenders, and homeowners alike to understand and monitor.

Exploring the Size and Scope of Texas's Residential Mortgage Industry

You may want to see also

Explore related products

![]()

Mortgage Debt by Loan Type (Conventional, FHA, VA, etc.)

Conventional loans dominate the mortgage landscape, accounting for the majority of outstanding mortgage debt in the United States. These loans are not insured or guaranteed by the government and typically require a minimum down payment of 3%. They are popular among borrowers with strong credit scores and stable incomes. FHA loans, on the other hand, are insured by the Federal Housing Administration and are designed to help first-time homebuyers and those with lower credit scores. They require a minimum down payment of 3.5% and have more lenient credit requirements. VA loans, available to veterans and active-duty military personnel, are guaranteed by the Department of Veterans Affairs and offer zero down payment options. USDA loans, aimed at rural borrowers, are guaranteed by the United States Department of Agriculture and also offer zero down payment options.

The distribution of mortgage debt by loan type has significant implications for the housing market and the economy as a whole. Conventional loans, being the largest share of mortgage debt, are closely monitored by lenders and policymakers. Changes in conventional loan interest rates can have a ripple effect on the entire housing market. FHA loans, while smaller in share, play a crucial role in promoting homeownership among underserved populations. VA and USDA loans, though niche, are important for supporting specific segments of the population, such as veterans and rural residents.

One unique aspect of mortgage debt by loan type is the varying levels of risk associated with each type. Conventional loans are generally considered less risky due to the higher credit standards and larger down payments required. FHA loans, however, carry a higher risk due to the lower credit requirements and smaller down payments. VA and USDA loans also carry a higher risk due to the zero down payment options and more lenient credit requirements. Lenders and policymakers must carefully manage these risks to ensure the stability of the housing market.

In recent years, there has been a shift in the composition of mortgage debt by loan type. The share of conventional loans has decreased, while the share of FHA, VA, and USDA loans has increased. This shift is likely due to changes in the housing market, such as rising home prices and increasing interest rates, which have made it more difficult for borrowers to qualify for conventional loans. As a result, more borrowers are turning to government-insured and guaranteed loans, which offer more favorable terms.

Understanding the breakdown of mortgage debt by loan type is essential for anyone involved in the housing market, from lenders and policymakers to borrowers and real estate agents. Each loan type has its own unique characteristics, risks, and benefits, and a thorough understanding of these factors is necessary to make informed decisions. By analyzing the distribution of mortgage debt by loan type, we can gain insights into the health of the housing market and the economy as a whole.

Exploring the Size and Scope of the Mortgage-Backed Securities Market

You may want to see also

Explore related products

![]()

Mortgage Debt by Region (Northeast, Midwest, South, West)

The distribution of mortgage debt across different regions of the United States reveals significant disparities, reflecting varying economic conditions, housing markets, and demographic trends. In the Northeast, for instance, mortgage debt tends to be higher due to the region's high cost of living and expensive housing market. States like New York and Massachusetts have some of the highest median home prices in the country, which naturally leads to larger mortgage balances.

In contrast, the Midwest generally has lower mortgage debt levels. This region is characterized by more affordable housing and a lower cost of living, which results in smaller mortgage balances. States such as Ohio and Indiana have median home prices that are significantly lower than those in the Northeast, contributing to the overall lower mortgage debt in the area.

The South presents a mixed picture when it comes to mortgage debt. While some states like Florida and Texas have experienced rapid growth in housing prices and mortgage debt, others in the region have more moderate levels. The diversity in economic conditions and housing markets within the South leads to a varied landscape of mortgage debt.

Out West, mortgage debt levels can vary widely depending on the state. California, with its notoriously high housing prices, has substantial mortgage debt, while states like Nevada and Arizona have seen fluctuations in their housing markets, impacting mortgage debt levels. The tech boom in states like Washington and Oregon has also driven up housing prices and, consequently, mortgage debt in those areas.

Understanding these regional differences is crucial for policymakers, lenders, and homeowners alike. It allows for targeted strategies to address housing affordability, manage mortgage debt, and promote sustainable homeownership across the country. By examining the unique characteristics of each region's mortgage debt landscape, more effective solutions can be developed to support the diverse needs of American homeowners.

Exploring the Spaciousness of Ruoff Mortgage's Venue: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Average Mortgage Balance per Borrower

The average mortgage balance per borrower in the United States provides a snapshot of the financial obligations homeowners carry. As of the latest data available, this figure stands at approximately $200,000. This amount reflects the principal balance owed on mortgages, excluding interest and other fees. It's important to note that this average can vary significantly based on factors such as the state in which the property is located, the type of mortgage, and the borrower's creditworthiness.

Analyzing the average mortgage balance per borrower can offer insights into broader economic trends. For instance, an increase in this average could indicate a rise in home prices or a shift towards larger loan amounts, possibly due to changes in lending standards or borrower preferences. Conversely, a decrease might suggest improvements in affordability or changes in the housing market dynamics.

To put this figure into perspective, it's useful to compare it with other economic indicators. For example, the average mortgage balance per borrower can be juxtaposed with median household income, the percentage of household income spent on housing, or the national debt. Such comparisons can help in understanding the relative burden of mortgage debt on borrowers and the overall economy.

Moreover, the average mortgage balance per borrower can have implications for monetary policy and financial stability. Central banks and regulatory bodies monitor this metric as part of their assessment of the housing market and its potential impact on the broader financial system. High levels of mortgage debt can increase the risk of default, particularly during economic downturns, which can have cascading effects on the financial sector.

In conclusion, the average mortgage balance per borrower is a key indicator that sheds light on the state of the housing market and the financial health of homeowners. By examining this metric closely, policymakers, economists, and financial analysts can gain valuable insights into economic conditions and make informed decisions.

Exploring the Scale and Impact of Movement Mortgage

You may want to see also

Explore related products

![]()

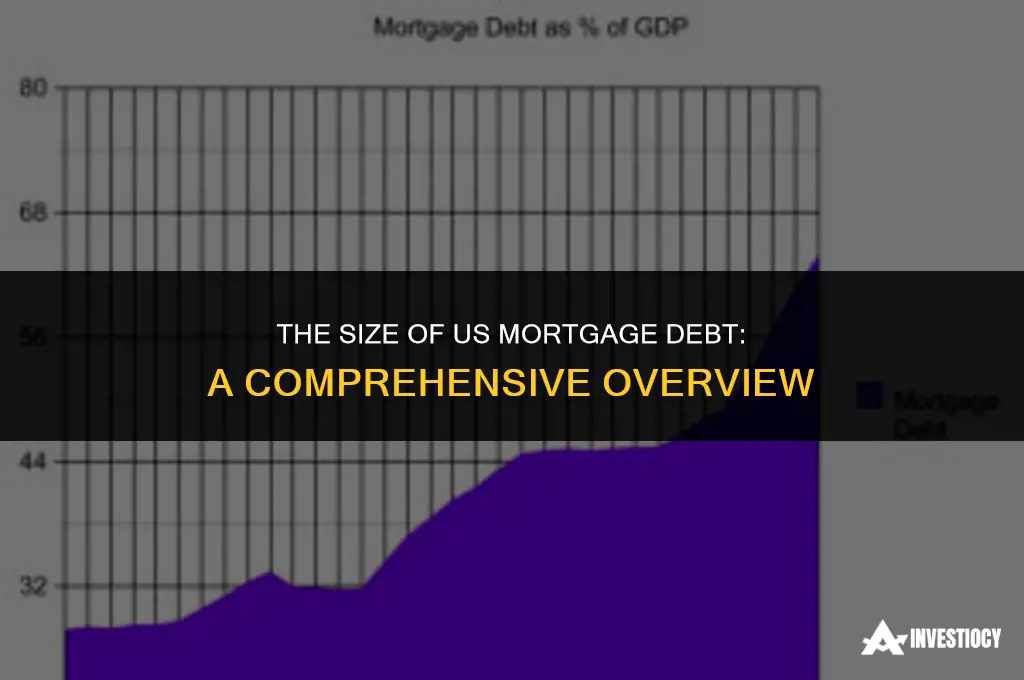

Mortgage Debt as a Percentage of GDP

The mortgage debt as a percentage of GDP is a critical indicator of the economic health and stability of a country. It provides insight into the level of indebtedness of households and the potential risks to the financial system. In the United States, mortgage debt has historically been a significant component of the overall debt landscape. As of the latest data available, mortgage debt in the U.S. stands at approximately $12 trillion, which is roughly 60% of the country's GDP. This figure is substantial and highlights the importance of the housing market to the overall economy.

One unique angle to consider when analyzing mortgage debt as a percentage of GDP is the impact of interest rates on this ratio. As interest rates rise, the cost of servicing mortgage debt increases, which can lead to a higher percentage of GDP being allocated to mortgage payments. This, in turn, can reduce disposable income for households and potentially dampen economic growth. Conversely, when interest rates fall, mortgage payments become more affordable, and households may have more money to spend on other goods and services, thereby stimulating economic activity.

Another important consideration is the distribution of mortgage debt across different segments of the population. If a large portion of mortgage debt is concentrated among a small percentage of households, it could indicate a higher risk of default and financial instability. On the other hand, if mortgage debt is more evenly distributed, it may suggest a more stable housing market and less risk to the overall economy.

In addition to these factors, it is also essential to consider the quality of mortgage loans when assessing the risks associated with mortgage debt as a percentage of GDP. Loans with higher credit scores and lower loan-to-value ratios are generally considered less risky, while loans with lower credit scores and higher loan-to-value ratios are more likely to default. The proportion of high-risk loans in the overall mortgage debt can provide valuable information about the potential for future defaults and the impact on the economy.

Overall, mortgage debt as a percentage of GDP is a complex and multifaceted issue that requires careful analysis and consideration of various factors. By examining the impact of interest rates, the distribution of mortgage debt, and the quality of mortgage loans, policymakers and economists can gain a better understanding of the risks and opportunities associated with this critical economic indicator.

Exploring the Vast Landscape of the Mortgage Industry

You may want to see also

Frequently asked questions

As of the latest data available, the total U.S. mortgage debt is approximately $12 trillion.

The size of U.S. mortgage debt is influenced by factors such as the number of homeowners, average home prices, interest rates, and the prevalence of refinancing.

The U.S. mortgage debt is one of the largest in the world, reflecting the country's substantial housing market and high homeownership rates.

High mortgage debt can have various economic implications, including increased financial vulnerability for households, potential impacts on consumer spending, and broader effects on the housing market and overall economy.