To introduce the topic how do I find my grace period for my mortgage, you could start with a paragraph that explains the concept of a grace period in the context of mortgages. A grace period is typically a short time frame after a mortgage payment is due during which the payment can be made without incurring late fees or penalties. This period is designed to provide borrowers with some flexibility in managing their finances. To find your grace period, you would need to refer to your mortgage contract or contact your lender directly, as the terms can vary depending on the specific loan agreement. It's important to understand and utilize this grace period effectively to avoid unnecessary charges and maintain a good credit standing.

| Characteristics | Values |

|---|---|

| Query Type | Mortgage Grace Period Inquiry |

| Language | English |

| Context | Financial Services, Homeownership |

| Intent | Seeking Information |

| Complexity | Moderate |

| Emotional Tone | Neutral |

| Urgency Level | Low to Moderate |

| Audience | Homeowner or Potential Homeowner |

| Required Knowledge | Basic understanding of mortgage terms |

| Potential Follow-up Questions | What is a grace period? How does it affect my credit score? What happens if I miss the grace period? |

| Possible Answers | Varies by lender, typically 10-15 days, affects credit score negatively if missed |

| Related Topics | Mortgage payments, credit score, loan terms |

| Suggested Resources | Lender's website, financial advisor, mortgage calculator |

| Actionable Steps | Contact lender, review loan documents, set up payment reminders |

| Resolution | Obtain specific grace period information from lender |

Explore related products

What You'll Learn

- Understanding Grace Periods: Learn what a mortgage grace period is and why it's important

- Reviewing Loan Documents: Find and read the specific terms related to your grace period

- Contacting Your Lender: Reach out to your mortgage lender to confirm the details of your grace period

- Calculating Grace Period End Date: Use your loan start date and grace period length to calculate the end date

- Making Timely Payments: Ensure you make payments before the grace period ends to avoid penalties

![]()

Understanding Grace Periods: Learn what a mortgage grace period is and why it's important

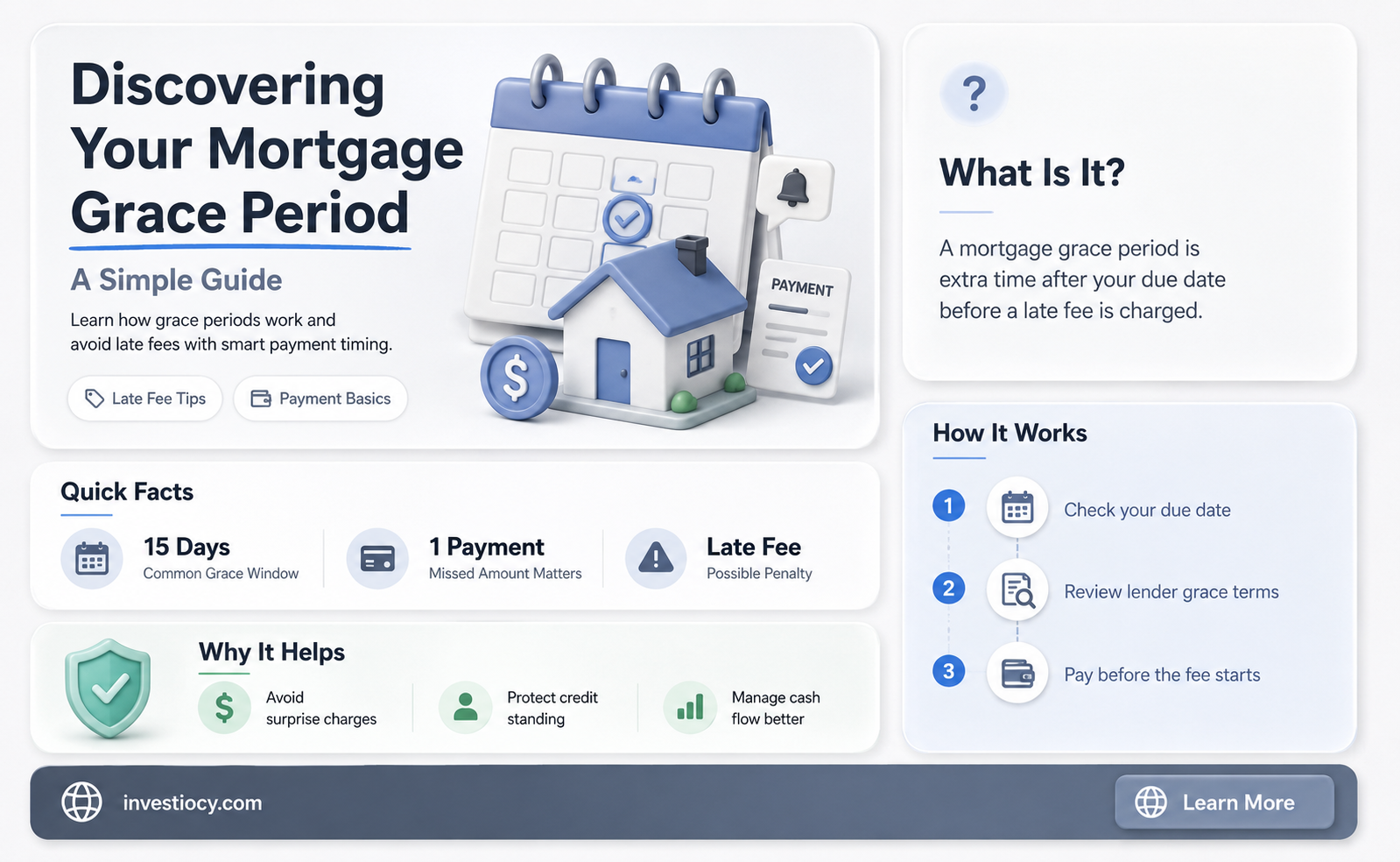

A mortgage grace period is a crucial aspect of homeownership that many borrowers may not fully understand. It refers to the time frame during which a borrower can make their mortgage payment after the due date without incurring late fees or penalties. This period is typically 15 days, but it can vary depending on the lender and the terms of the mortgage agreement.

Understanding your mortgage grace period is important for several reasons. First, it allows you to manage your finances more effectively. If you know you have a few extra days to make your payment, you can better plan your budget and avoid unnecessary stress. Second, it helps you avoid late fees, which can add up over time and increase the overall cost of your mortgage. Third, it can protect your credit score. Late payments can negatively impact your credit, making it more difficult to secure loans or credit cards in the future.

To find your grace period, you should review your mortgage agreement or contact your lender directly. The agreement will typically outline the terms of the grace period, including the length of time and any conditions or exceptions. If you're unsure about your grace period, it's better to err on the side of caution and make your payments on time to avoid any potential issues.

In addition to understanding your grace period, it's also important to be aware of any changes that may affect it. For example, if you refinance your mortgage or make changes to your payment schedule, your grace period may be impacted. By staying informed and proactive, you can ensure that you're always aware of your grace period and can make your payments accordingly.

Overall, understanding your mortgage grace period is a key part of responsible homeownership. By knowing the terms of your grace period and managing your payments effectively, you can avoid unnecessary fees and penalties, protect your credit score, and maintain a healthy financial situation.

Uncovering Your Past: A Guide to Finding Old Mortgage Account Numbers

You may want to see also

Explore related products

![Pardoned by Grace [DVD]](https://m.media-amazon.com/images/I/613jft-1OxL._AC_UY218_.jpg)

![]()

Reviewing Loan Documents: Find and read the specific terms related to your grace period

To determine your mortgage grace period, you'll need to review your loan documents carefully. The grace period is typically outlined in the promissory note or the loan agreement. Look for specific terms that mention a "grace period," "forbearance period," or any similar language that indicates a timeframe during which you can make payments without incurring late fees or penalties.

Start by examining the section of your loan documents that details the repayment terms. This is often found in the "Payment Provisions" or "Borrower's Obligations" section. Within this section, search for language that specifies a grace period, such as "The Borrower shall have a grace period of [number] days from the due date of each payment during which time no late charge shall be assessed."

If you're unable to find the grace period information in the repayment terms section, check other parts of your loan documents, such as the "Definitions" section or any addendums or riders that may have been attached to the original loan agreement. Sometimes, the grace period details might be included in a separate document, such as a "Grace Period Agreement" or "Forbearance Agreement," which would typically be signed at the same time as the main loan documents.

Once you've located the grace period information, read it carefully to understand the specific terms and conditions. Note the length of the grace period, any requirements or restrictions associated with it, and how it affects your overall repayment obligations. If you have any questions or concerns about the grace period terms, consider consulting with a mortgage professional or a legal advisor who can provide personalized guidance based on your unique situation.

Remember, understanding your grace period is crucial for managing your mortgage payments effectively and avoiding unnecessary fees or penalties. By taking the time to review your loan documents and familiarize yourself with the grace period terms, you can ensure that you're making informed decisions about your mortgage repayments.

Unlocking Opportunities: A Guide to Finding Assumable Mortgages

You may want to see also

Explore related products

![Amazing Grace[DVD]](https://m.media-amazon.com/images/I/71IMSN3kcGL._AC_UY218_.jpg)

![]()

Contacting Your Lender: Reach out to your mortgage lender to confirm the details of your grace period

To determine your mortgage grace period, one of the most direct approaches is to contact your lender. This involves reaching out to the customer service department of the financial institution that holds your mortgage. When you contact your lender, be prepared to provide your loan number and personal identification to ensure they can access your account information.

The process typically involves a phone call or an online inquiry through the lender's website. During this interaction, you can ask specific questions about your grace period, such as its duration, start date, and any conditions or fees associated with it. It's important to take notes during the conversation, including the name of the representative you speak with and the date and time of the call, in case you need to refer back to this information later.

If you're unsure about how to reach your lender, check your mortgage documents for contact information. Alternatively, you can usually find contact details on the lender's website or through a quick online search. When you initiate contact, be clear about your request and ask for confirmation of the details discussed, preferably in writing, to avoid any misunderstandings.

Remember that lenders are legally required to provide you with accurate information about your mortgage terms, including the grace period. By contacting your lender directly, you can ensure that you have the correct information and avoid any potential issues related to missed payments or misunderstandings about your mortgage obligations.

Discover Your Wells Fargo Mortgage Balance: A Simple Guide

You may want to see also

Explore related products

![Amazing Grace [DVD]](https://m.media-amazon.com/images/I/811BScW1i-L._AC_UY218_.jpg)

![]()

Calculating Grace Period End Date: Use your loan start date and grace period length to calculate the end date

To calculate the grace period end date for your mortgage, you'll need to know the loan start date and the length of the grace period. The loan start date is typically the date when the loan is disbursed or the date of the loan agreement. The grace period length is the amount of time you have before you're required to make your first payment.

Once you have this information, calculating the end date is straightforward. Simply add the grace period length to the loan start date. For example, if your loan start date is January 1, 2023, and your grace period is 3 months, your grace period end date would be April 1, 2023.

It's important to note that the grace period end date may not always fall on the same day of the month as the loan start date. If the grace period length is not a whole number of months, you'll need to calculate the end date by adding the remaining days to the last day of the month. For instance, if your loan start date is January 15, 2023, and your grace period is 2 months and 15 days, your grace period end date would be March 30, 2023.

To avoid any confusion, it's a good idea to double-check your calculations with your lender or mortgage servicer. They can provide you with the exact grace period end date and ensure that you're on track with your payments.

Remember, the grace period is a temporary reprieve from making payments, but it's not a forgiveness of the debt. Once the grace period ends, you'll be expected to make your regular payments on time to avoid penalties and potential foreclosure.

How to Locate Documents Confirming Your Mortgage Payoff

You may want to see also

![]()

Making Timely Payments: Ensure you make payments before the grace period ends to avoid penalties

To avoid penalties and maintain a good credit score, it's crucial to make mortgage payments on time. The grace period is a window of opportunity that allows borrowers to make payments without incurring late fees. Typically, this period ranges from 10 to 15 days after the due date, but it can vary depending on the lender and the terms of the mortgage agreement.

One effective strategy to ensure timely payments is to set up automatic transfers from your bank account. This way, you can guarantee that the payment will be made on time, even if you're away or preoccupied. Additionally, consider using a budgeting app or spreadsheet to track your expenses and allocate funds for your mortgage payment well in advance.

Another important aspect to consider is the impact of late payments on your credit score. A single late payment can significantly lower your score, making it more difficult to secure loans or credit cards in the future. By making payments on time, you can maintain a good credit score and enjoy better financial opportunities.

If you're unsure about the exact duration of your grace period, it's best to contact your lender directly. They can provide you with the necessary information and help you understand the terms of your mortgage agreement. Remember, it's always better to be proactive and informed when it comes to managing your finances.

Uncover Homeowner Mortgage Secrets: A Property Research Guide

You may want to see also

Frequently asked questions

To determine the length of your mortgage grace period, review your mortgage contract or loan agreement. This document should specify the grace period terms, including the duration and any conditions that apply.

Making a late payment during the grace period typically means you'll incur a late fee. However, it's important to note that the grace period is designed to provide a short extension for payment without negatively impacting your credit score.

Extending your mortgage grace period is generally not possible as it's a fixed term set by your lender. However, if you're experiencing financial difficulties, you may want to contact your lender to discuss potential options for payment assistance or loan modification.

Payments made during the grace period are not considered late and therefore should not negatively affect your credit score. However, if you make a payment after the grace period has ended, it may be reported as late and could impact your credit score.