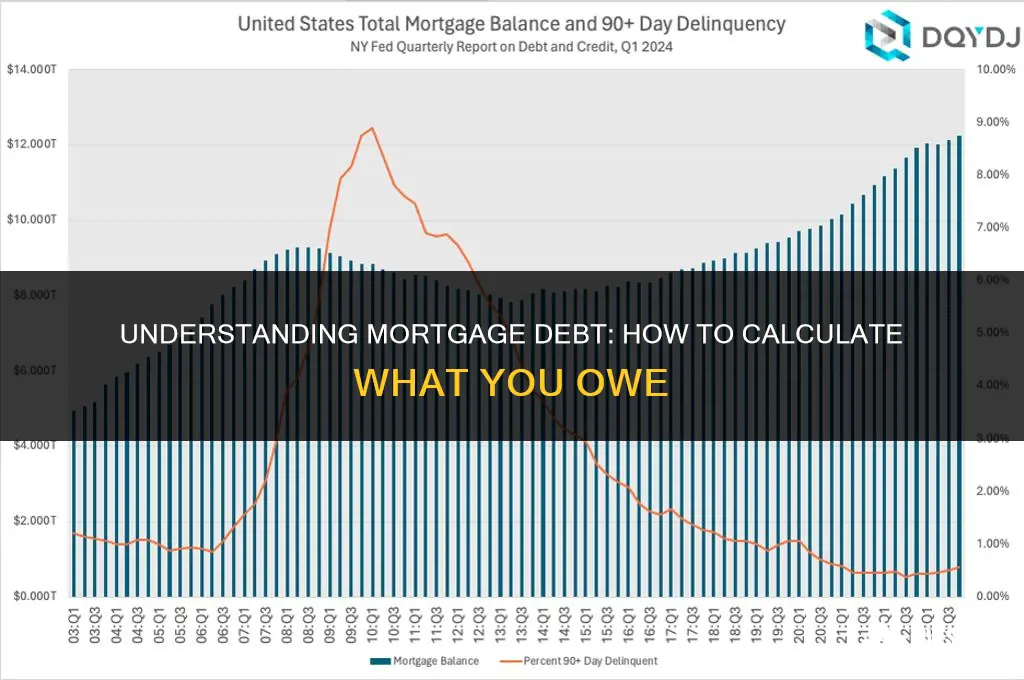

Understanding your mortgage balance is crucial for managing your homeownership journey. To determine how much you owe on your mortgage, you'll need to review your most recent mortgage statement or contact your lender directly. Your mortgage balance can fluctuate over time due to factors such as interest rates, payment schedules, and any additional fees or penalties. It's essential to stay informed about your outstanding balance to make informed decisions about refinancing, selling your property, or planning for the future.

Explore related products

What You'll Learn

![]()

Understanding your mortgage statement

Your mortgage statement is a crucial document that provides a detailed breakdown of your mortgage payments and outstanding balance. It's essential to understand this statement to ensure you're on track with your payments and to identify any potential issues early on. The statement typically includes information such as the payment due date, the amount due, the principal balance, the interest rate, and any escrow or impound amounts for taxes and insurance.

One key aspect of understanding your mortgage statement is recognizing how your payments are applied to your loan. Each payment is usually divided into two parts: the principal, which goes towards paying off the loan balance, and the interest, which is the cost of borrowing the money. Over time, the portion of your payment that goes towards the principal increases, while the interest portion decreases. This is known as amortization.

Another important element to look at is the escrow or impound section. This is where a portion of your payment is set aside to cover property taxes and homeowners insurance. The lender typically estimates these costs and adjusts your monthly payment accordingly. It's crucial to review this section to ensure that the estimates are accurate and that you're not overpaying or underpaying for these expenses.

Additionally, your mortgage statement may include information about any late fees or penalties, as well as any changes to your interest rate or payment terms. It's important to review these details carefully to avoid any surprises and to take action if necessary. For example, if you notice a sudden increase in your payment, it may be due to an adjustment in your escrow amount or a change in your interest rate.

To make the most of your mortgage statement, it's a good idea to set up a system for tracking your payments and reviewing the statement regularly. This can help you identify any discrepancies or issues early on and take steps to address them. You may also want to consider using online tools or apps that can help you analyze your mortgage statement and provide personalized advice.

In conclusion, understanding your mortgage statement is a critical part of managing your mortgage and ensuring that you're on track to pay off your loan. By reviewing the statement regularly and paying attention to the details, you can avoid potential problems and make informed decisions about your mortgage.

Simplifying Your Wells Fargo Mortgage Payment Process

You may want to see also

Explore related products

![]()

Calculating monthly payments

To calculate your monthly mortgage payments, you'll need to use a specific formula that takes into account the principal amount, interest rate, and loan term. The most common formula used is the amortization formula, which breaks down the payment into principal and interest components. Here's the formula:

M = P [ i(1 + i)^n ] / [ (1 + i)^n – 1]

Where:

M = monthly payment

P = principal amount (the initial amount borrowed)

I = monthly interest rate (annual interest rate divided by 12)

N = number of payments (loan term in months)

Let's say you've borrowed $200,000 at an annual interest rate of 4%. Your loan term is 30 years, which means you'll make 360 payments. First, you'd convert the annual interest rate to a monthly rate by dividing 4% by 12, which gives you 0.3333%. Then, you'd plug the numbers into the formula:

M = 200,000 [ 0.003333(1 + 0.003333)^360 ] / [ (1 + 0.003333)^360 – 1]

This calculation would give you a monthly payment of approximately $954.83.

It's important to note that this formula assumes a fixed interest rate and a fixed loan term. If your interest rate is adjustable or your loan term is not standard, you may need to use a different formula or consult with a financial advisor.

One common mistake people make when calculating their monthly payments is forgetting to account for other costs associated with homeownership, such as property taxes, homeowners insurance, and maintenance fees. These costs can add up quickly and should be factored into your overall budget when determining how much house you can afford.

Another important consideration is the impact of making extra payments on your mortgage. If you're able to make additional payments each month, you can significantly reduce the amount of interest you pay over the life of the loan and potentially pay off your mortgage early. However, it's crucial to check with your lender to ensure that there are no prepayment penalties associated with your loan.

In conclusion, calculating your monthly mortgage payments is a critical step in the homebuying process. By using the amortization formula and considering other costs associated with homeownership, you can make an informed decision about how much house you can afford and potentially save thousands of dollars over the life of your loan.

Celebrating Financial Freedom: How to Mark Your Mortgage as Paid Off

You may want to see also

Explore related products

![]()

Managing escrow accounts

An escrow account is a crucial component of your mortgage, designed to hold funds for property taxes and homeowners insurance. This account ensures that these expenses are paid on time, preventing potential penalties or loss of coverage. To manage your escrow account effectively, it's essential to understand how it works and how to monitor its activity.

The first step in managing your escrow account is to review your mortgage statement regularly. This statement will detail the amount of money being deposited into your escrow account each month, as well as any disbursements made for taxes or insurance. By keeping track of these transactions, you can ensure that your escrow account is being managed correctly and that there are no discrepancies.

Another important aspect of managing your escrow account is to anticipate changes in your property taxes or insurance premiums. If you receive a notice of a tax increase or a change in your insurance policy, contact your mortgage lender immediately to discuss how this will affect your escrow payments. Failure to do so could result in a shortage in your escrow account, which may lead to additional fees or penalties.

It's also a good idea to set aside extra funds in your escrow account if possible. This can help cover unexpected expenses, such as a sudden increase in property taxes or a claim on your homeowners insurance. Having a cushion in your escrow account can provide peace of mind and prevent financial stress.

Finally, if you're having trouble managing your escrow account or have questions about how it works, don't hesitate to reach out to your mortgage lender for assistance. They can provide guidance on how to make adjustments to your escrow payments or help you understand any changes to your account. By staying informed and proactive, you can ensure that your escrow account is well-managed and that you're prepared for any potential issues that may arise.

How to Make an Overpayment on Your Barclays Mortgage: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Refinancing options

Refinancing your mortgage can be a strategic move to manage your debt, especially if you're looking to lower your monthly payments or pay off your loan faster. One option to consider is a rate-and-term refinance, which allows you to change the interest rate and the length of your loan without altering the principal balance. This can be beneficial if interest rates have dropped since you initially took out your mortgage.

Another refinancing option is a cash-out refinance, where you borrow more than you owe on your current mortgage and receive the difference in cash. This can be useful for consolidating debt, making home improvements, or covering other expenses. However, it's important to note that this increases your principal balance and may result in higher monthly payments.

If you're struggling to make your mortgage payments, a loan modification might be a better option than refinancing. This involves changing the terms of your existing loan, such as the interest rate or payment schedule, to make it more affordable. Loan modifications are typically easier to qualify for than refinancing and can provide immediate relief.

When considering refinancing options, it's crucial to evaluate your financial situation and goals. Calculate the break-even point to determine how long it will take for the savings from a lower interest rate to offset the costs of refinancing. Additionally, consider the impact on your credit score, as applying for a new loan can result in a temporary dip.

In conclusion, refinancing options can provide various benefits, but it's essential to carefully weigh the pros and cons and choose the option that best aligns with your financial objectives.

Smart Strategies for Making Extra Mortgage Payments

You may want to see also

Explore related products

![NMLS Study Guide 2026-2027 - 5 Full-Length Practice Tests, SAFE MLO Exam Prep Secrets Book for the Mortgage Loan Originator Exam: [4th Edition]](https://m.media-amazon.com/images/I/717iHac5CwL._AC_UL320_.jpg)

![]()

Foreclosure prevention strategies

If you're facing the possibility of foreclosure, it's crucial to act quickly and explore all available options to save your home. One strategy is to contact your lender as soon as possible to discuss potential solutions. They may be willing to work with you on a loan modification, which could involve reducing your interest rate, extending your loan term, or even forgiving a portion of your debt. Another option is to look into government programs designed to help homeowners in distress. For example, the Home Affordable Modification Program (HAMP) offers financial assistance to eligible borrowers to help them avoid foreclosure.

In addition to these strategies, it's important to be aware of potential scams that target homeowners facing foreclosure. Some companies may claim to offer foreclosure prevention services, but instead, they may charge you fees for services that are available for free or even attempt to steal your home. Be cautious of any unsolicited offers and always verify the legitimacy of any company or individual you're working with.

One often overlooked strategy for preventing foreclosure is to explore the possibility of a short sale. In a short sale, you sell your home for less than the amount you owe on your mortgage, and the lender agrees to accept the proceeds as full payment. This can be a viable option if you're unable to make your mortgage payments and don't have the equity to refinance or modify your loan. However, it's important to note that a short sale can have a negative impact on your credit score and may not be the best option for everyone.

Another strategy to consider is filing for bankruptcy. While bankruptcy should be a last resort, it can provide a temporary reprieve from foreclosure proceedings and give you time to reorganize your finances. Depending on the type of bankruptcy you file, you may be able to keep your home and work out a plan to repay your mortgage debt. However, bankruptcy can have serious long-term consequences, including damage to your credit score and potential loss of assets, so it's essential to consult with a qualified bankruptcy attorney before making this decision.

Finally, if you're struggling to make your mortgage payments, it's important to prioritize your financial obligations and make smart decisions about where to allocate your resources. This may involve cutting back on non-essential expenses, seeking additional income, or working with a credit counselor to develop a budget and debt repayment plan. By taking proactive steps to address your financial challenges, you can increase your chances of avoiding foreclosure and keeping your home.

Unlocking the Paper Trail: A Guide to Obtaining Mortgage Lien Documents

You may want to see also

Frequently asked questions

To find out how much you owe on your mortgage, you can check your monthly mortgage statement, which typically includes the outstanding principal balance. You can also contact your mortgage lender directly to request this information.

Several factors can influence the amount you owe on your mortgage, including your original loan amount, interest rate, loan term, payment history, and any additional fees or charges. Making extra payments or refinancing your mortgage can also impact the outstanding balance.

To pay off your mortgage faster, you can consider making extra payments towards the principal, refinancing to a shorter loan term or lower interest rate, or utilizing a bi-weekly payment schedule. It's important to check with your lender for any prepayment penalties and to ensure that extra payments are applied correctly to your account.