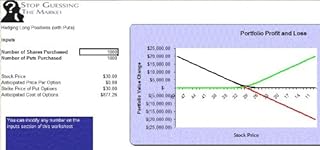

Shorting a mortgage bond involves taking a position that profits from a decline in the bond's price. This can be achieved through various strategies, such as borrowing the bond from a broker and selling it at the current market price, with the expectation of repurchasing it later at a lower price to return to the lender. Another method is to use derivatives, like options or futures, to gain exposure to the bond's price movements without physically holding the bond. Shorting mortgage bonds can be a complex and risky endeavor, as it requires a deep understanding of the bond market, interest rate dynamics, and the specific characteristics of mortgage-backed securities. Additionally, shorting can be subject to regulatory restrictions and may involve significant transaction costs and margin requirements.

Explore related products

![The Law of Railway Bonds and Mortgages in the United States of America. With Illustrative Cases from English and Colonial Courts 1897 [Leather Bound]](https://m.media-amazon.com/images/I/617DLHXyzlL._AC_UY218_.jpg)

What You'll Learn

- Understanding Mortgage Bonds: Basics of mortgage-backed securities and their role in the financial market

- Short Selling Fundamentals: Explanation of short selling, including borrowing shares and selling them in anticipation of a price drop

- Identifying Short Opportunities: Analyzing mortgage bond market trends and news to spot potential short selling opportunities

- Risks and Rewards: Evaluating the risks associated with shorting mortgage bonds, such as market volatility and potential losses

- Strategies and Techniques: Various approaches to shorting mortgage bonds, including using derivatives and exchange-traded funds (ETFs)

![]()

Understanding Mortgage Bonds: Basics of mortgage-backed securities and their role in the financial market

Mortgage bonds, also known as mortgage-backed securities (MBS), are financial instruments that represent an ownership interest in a pool of mortgages. These securities are created when a financial institution, such as a bank, bundles together a large number of mortgages and sells them to investors. The investors then receive payments based on the interest and principal repayments made by the homeowners.

The process of creating mortgage bonds involves several steps. First, a bank or other financial institution originates mortgages to homeowners. These mortgages are then pooled together based on certain criteria, such as the type of mortgage, the interest rate, and the creditworthiness of the borrowers. Once the pool is created, it is securitized, meaning that it is structured into a financial product that can be sold to investors. The resulting securities are backed by the cash flows from the underlying mortgages, which provide the collateral for the bonds.

Mortgage bonds play a significant role in the financial market by providing liquidity to the mortgage market. This liquidity allows banks to originate more mortgages, which in turn enables more people to purchase homes. Additionally, mortgage bonds offer investors a way to diversify their portfolios and earn income through the interest payments made by the borrowers.

There are different types of mortgage bonds, including pass-through securities, collateralized mortgage obligations (CMOs), and stripped mortgage-backed securities (SMBS). Pass-through securities are the simplest type, where the cash flows from the underlying mortgages are passed directly to the investors. CMOs are more complex, involving multiple tranches with varying levels of risk and return. SMBS are created by separating the interest and principal payments from the underlying mortgages, allowing investors to purchase specific components of the cash flow.

Understanding mortgage bonds is crucial for investors looking to enter the mortgage-backed securities market. It is important to grasp the basics of how these securities are created, structured, and traded, as well as the risks and rewards associated with them. This knowledge can help investors make informed decisions and navigate the complexities of the financial market.

Securing a Mortgage for Your Dependent: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Short Selling Fundamentals: Explanation of short selling, including borrowing shares and selling them in anticipation of a price drop

Short selling is a sophisticated investment strategy that involves borrowing shares of a stock or other security from a broker and selling them on the market with the anticipation that the price will decline. This allows the short seller to profit by repurchasing the shares at a lower price to return to the lender. While commonly associated with stocks, short selling can also be applied to mortgage bonds, though the process and considerations are somewhat different.

In the context of mortgage bonds, short selling involves borrowing the bonds from a broker or another investor and selling them on the market. The short seller expects the bond prices to fall, perhaps due to rising interest rates, changes in credit ratings, or other market conditions. Once the price drops, the short seller can buy back the bonds at the lower price, return them to the lender, and pocket the difference as profit.

One key aspect of short selling mortgage bonds is understanding the borrowing process. Unlike stocks, mortgage bonds are not typically held in a brokerage account and available for immediate borrowing. Instead, they may need to be sourced from other investors or financial institutions. This can involve negotiating loan terms, including interest rates and collateral requirements, which can add complexity to the short selling process.

Another important consideration is the risk involved. Short selling mortgage bonds can be highly risky, as bond prices can be volatile and may not always move in the anticipated direction. Additionally, if the short seller is unable to repurchase the bonds at a lower price, they may be forced to buy them back at a higher price, resulting in a loss. Furthermore, short sellers must be aware of potential regulatory restrictions and market conditions that could impact their ability to execute the strategy effectively.

Despite the risks, short selling mortgage bonds can be a valuable tool for investors looking to hedge against potential losses in their bond portfolios or to profit from market downturns. By understanding the fundamentals of short selling, including the borrowing process, market dynamics, and risk management, investors can make informed decisions about whether this strategy is right for them.

Navigating the Process of Releasing a Recorded Mortgage in New Jersey

You may want to see also

Explore related products

![]()

Identifying Short Opportunities: Analyzing mortgage bond market trends and news to spot potential short selling opportunities

Analyzing mortgage bond market trends and news is crucial for identifying potential short selling opportunities. One approach is to monitor economic indicators such as interest rates, housing market data, and inflation rates, as these can significantly impact the value of mortgage bonds. For instance, if interest rates are expected to rise, it may lead to a decrease in mortgage bond prices, presenting a short selling opportunity.

Another strategy is to keep an eye on news related to the mortgage industry, such as changes in lending regulations, shifts in consumer behavior, or developments in the housing market. These news items can provide insights into potential market movements and help traders anticipate changes in mortgage bond prices. For example, if there is news about a significant increase in foreclosures, it may indicate a weakening housing market, which could lead to lower mortgage bond prices.

Technical analysis can also be used to identify short selling opportunities in the mortgage bond market. By examining price charts and using indicators such as moving averages, relative strength index (RSI), and Bollinger Bands, traders can spot potential trend reversals or price breakouts that may signal a short selling opportunity. For instance, if the price of a mortgage bond breaks below a key support level, it may indicate a potential downward trend, making it a candidate for short selling.

In addition to these methods, traders can also use fundamental analysis to evaluate the creditworthiness of mortgage bond issuers. By examining factors such as the issuer's financial health, credit ratings, and debt-to-equity ratios, traders can identify potential risks that may lead to a decrease in mortgage bond prices. For example, if an issuer has a high debt-to-equity ratio and is facing financial difficulties, it may be more likely to default on its mortgage bond payments, presenting a short selling opportunity.

When identifying short opportunities in the mortgage bond market, it is essential to consider the overall market sentiment and positioning. By understanding the prevailing market sentiment and the positioning of other traders, traders can better anticipate potential market movements and make more informed short selling decisions. For instance, if the market sentiment is bullish on mortgage bonds, it may be more challenging to find short selling opportunities, as most traders may be looking to buy rather than sell.

In conclusion, identifying short opportunities in the mortgage bond market requires a combination of technical, fundamental, and sentiment analysis. By monitoring economic indicators, news, and market trends, and by evaluating the creditworthiness of mortgage bond issuers, traders can spot potential short selling opportunities and make informed trading decisions.

Navigating the Process: Removing a Deceased Person from a Mortgage

You may want to see also

Explore related products

![]()

Risks and Rewards: Evaluating the risks associated with shorting mortgage bonds, such as market volatility and potential losses

Shorting mortgage bonds involves a unique set of risks that investors must carefully evaluate before entering into such a position. One of the primary risks associated with shorting mortgage bonds is market volatility. Mortgage bonds are sensitive to changes in interest rates, and sudden shifts in the market can lead to significant price fluctuations. Investors who are short mortgage bonds may find themselves facing substantial losses if the market moves against them.

Another risk to consider is the potential for unlimited losses. When an investor shorts a mortgage bond, they are essentially betting that the bond's price will decrease. However, if the bond's price increases instead, the investor may be forced to buy back the bond at a higher price, resulting in a loss. Unlike other types of investments, such as stocks, where losses are typically limited to the initial investment, shorting mortgage bonds can result in losses that exceed the initial investment.

In addition to market volatility and potential losses, investors must also consider the impact of prepayment risk on their short positions. Mortgage bonds are subject to prepayment risk, which means that the borrower can choose to pay off the loan early. If a borrower prepays their mortgage, the bond's price will increase, potentially resulting in losses for investors who are short the bond.

To mitigate these risks, investors can employ various strategies, such as hedging their positions or setting stop-loss orders. Hedging involves taking a position in a related asset that will offset losses in the event that the market moves against the investor. Stop-loss orders, on the other hand, are instructions to sell a security at a predetermined price, which can help limit losses if the market moves against the investor.

Despite the risks associated with shorting mortgage bonds, there are also potential rewards for investors who are able to successfully navigate the market. Shorting mortgage bonds can provide investors with an opportunity to profit from declining bond prices, which can be particularly lucrative during periods of economic downturn or rising interest rates. Additionally, shorting mortgage bonds can serve as a diversification strategy, allowing investors to reduce their exposure to the bond market and potentially improve their overall portfolio performance.

In conclusion, shorting mortgage bonds involves a complex interplay of risks and rewards. Investors must carefully evaluate the potential risks associated with market volatility, unlimited losses, and prepayment risk before entering into a short position. However, for those who are able to successfully manage these risks, shorting mortgage bonds can provide an opportunity to profit from declining bond prices and diversify their investment portfolios.

Missouri Mortgage Recording: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Strategies and Techniques: Various approaches to shorting mortgage bonds, including using derivatives and exchange-traded funds (ETFs)

Shorting mortgage bonds can be achieved through various strategies and techniques, each with its own set of risks and rewards. One approach is to use derivatives, such as mortgage-backed securities (MBS) futures or options. These financial instruments allow investors to bet against the performance of mortgage bonds without directly owning them. For example, an investor could sell (short) MBS futures contracts, which would obligate them to deliver the underlying mortgage bonds at a predetermined price and date. If the price of mortgage bonds falls, the investor can buy back the futures contracts at a lower price, realizing a profit.

Another strategy for shorting mortgage bonds is through the use of exchange-traded funds (ETFs). ETFs are baskets of securities that trade on stock exchanges, and there are several ETFs specifically designed to track the performance of mortgage bonds. An investor could short sell shares of a mortgage bond ETF, which would involve borrowing shares from a broker and selling them on the market. The investor would then aim to buy back the shares at a lower price to return to the broker, pocketing the difference as profit.

It's important to note that shorting mortgage bonds carries significant risks, including the potential for unlimited losses if the price of mortgage bonds rises instead of falls. Additionally, shorting can be complex and may require a deep understanding of financial markets and instruments. Investors should carefully consider their risk tolerance and investment goals before engaging in shorting strategies.

When using derivatives or ETFs to short mortgage bonds, investors should also be aware of the specific characteristics and risks associated with each instrument. For example, MBS futures and options can be highly leveraged, meaning that a small change in the underlying mortgage bond price can result in a large change in the value of the derivative. Similarly, ETFs may have fees and expenses that can eat into investment returns, and they may not always track the performance of the underlying mortgage bonds perfectly.

In conclusion, shorting mortgage bonds can be a viable investment strategy for those who believe that mortgage bond prices will fall. However, it's crucial to understand the various approaches and their associated risks before engaging in such strategies. Investors should consult with a financial advisor and conduct thorough research to determine if shorting mortgage bonds is appropriate for their investment portfolio.

Unlocking Your Illinois Home: A Guide to Mortgage Release

You may want to see also

Frequently asked questions

Shorting a mortgage bond involves borrowing the bond from a broker and selling it at the current market price with the expectation that its price will fall in the future. The investor can then buy the bond back at a lower price to return to the broker, profiting from the difference.

To initiate a short position in a mortgage bond, an investor must first borrow the bond from a broker. This is typically done through a margin account. Once the bond is borrowed, the investor sells it at the current market price.

Shorting a mortgage bond carries several risks. If the bond's price increases instead of decreases, the investor will incur a loss. Additionally, there is the risk of a short squeeze, where a sudden increase in demand for the bond forces the investor to buy it back at a higher price.

To close a short position in a mortgage bond, the investor must buy the bond back at the current market price and return it to the broker. The profit or loss is realized at the point of closing the position.

Several factors can influence the price of a mortgage bond, including interest rates, the creditworthiness of the issuer, the demand for the bond, and the overall health of the economy. Changes in these factors can impact the bond's price, affecting the outcome of a short position.