Jared Vennett, a financial expert and author, delves into the complexities of modern mortgages in his latest work. He begins by explaining how the traditional mortgage model has evolved over time, giving rise to new types of mortgages that cater to different financial needs and circumstances. Vennett highlights the importance of understanding the intricacies of these modern mortgages, as they can significantly impact a borrower's financial stability and long-term wealth. He emphasizes the need for consumers to be well-informed about the various options available, including fixed-rate and adjustable-rate mortgages, as well as the implications of factors such as interest rates, loan terms, and credit scores. By providing a comprehensive overview of modern mortgages, Vennett aims to empower readers to make informed decisions about their home financing and navigate the often confusing world of mortgage lending with confidence.

Explore related products

What You'll Learn

- Historical Context: Jared Vennett explains how mortgages have evolved over time, providing a historical perspective

- Types of Mortgages: He details various mortgage types, such as fixed-rate, adjustable-rate, and interest-only mortgages

- Mortgage Process: Vennett outlines the steps involved in obtaining a mortgage, from application to closing

- Economic Impact: He discusses how mortgages influence the economy, including their role in financial crises

- Future Trends: Jared Vennett speculates on future trends in the mortgage industry, considering technological and regulatory changes

![]()

Historical Context: Jared Vennett explains how mortgages have evolved over time, providing a historical perspective

Jared Vennett delves into the historical evolution of mortgages, tracing their roots back to ancient civilizations. He explains that the concept of borrowing money to purchase property dates back to the Babylonians and Romans, who used various forms of credit to finance land acquisitions. Vennett highlights how these early mortgage systems laid the groundwork for modern lending practices.

Vennett then fast-forwards to the Middle Ages, where he discusses the emergence of interest-based lending and the role of Jewish moneylenders in shaping European financial systems. He notes that the Catholic Church's prohibition on usury led to the development of alternative lending mechanisms, such as the "long lease" system in England, which allowed borrowers to lease property for extended periods in exchange for regular payments.

The author also examines the impact of the Industrial Revolution on mortgage lending, explaining how the rise of urbanization and the growth of the middle class created a demand for homeownership. This led to the development of new financial institutions, such as building societies and savings banks, which offered mortgages to aspiring homeowners. Vennett emphasizes the importance of these innovations in making homeownership more accessible to the general population.

In the 20th century, Vennett discusses the transformative effect of government policies on the mortgage industry. He cites the creation of the Federal Housing Administration (FHA) in the United States as a key example, noting how the FHA's mortgage insurance programs helped to standardize lending practices and reduce the risk of default. This, in turn, led to a significant increase in homeownership rates and the growth of the suburban housing market.

Finally, Vennett brings the discussion up to the present day, highlighting the impact of technological advancements and globalization on the mortgage industry. He explains how the rise of online lending platforms and fintech companies has made it easier for borrowers to access mortgage information and apply for loans. Additionally, he notes how the increasing interconnectedness of global financial markets has led to a greater variety of mortgage products and more competitive interest rates.

Throughout his historical analysis, Vennett emphasizes the importance of understanding the evolution of mortgages in order to appreciate the complexities of modern lending practices. By providing this historical context, he aims to help readers better navigate the current mortgage landscape and make informed decisions about their own homeownership journeys.

Understanding Inflation's Effect on Your Mortgage Costs

You may want to see also

Explore related products

![]()

Types of Mortgages: He details various mortgage types, such as fixed-rate, adjustable-rate, and interest-only mortgages

Jared Vennett explains modern mortgages by detailing various types, such as fixed-rate, adjustable-rate, and interest-only mortgages. He emphasizes that understanding these types is crucial for making informed decisions when purchasing a home. Vennett notes that fixed-rate mortgages offer stability with consistent monthly payments, making them ideal for those who prefer predictability. On the other hand, adjustable-rate mortgages can provide lower initial interest rates but may increase over time, which can be risky if interest rates rise significantly. Interest-only mortgages, while allowing for lower initial payments, require careful management as they do not build equity in the home.

Vennett also discusses the importance of considering the length of the mortgage term, such as 15-year versus 30-year mortgages. He explains that shorter terms typically have higher monthly payments but result in lower overall interest costs and faster equity buildup. In contrast, longer terms offer lower monthly payments but higher total interest costs. Vennett advises potential homebuyers to carefully evaluate their financial situation and long-term goals when choosing a mortgage term.

Additionally, Vennett touches on specialized mortgage options, such as FHA loans, VA loans, and jumbo loans. He explains that FHA loans are designed for first-time homebuyers with lower credit scores, offering more lenient qualification requirements. VA loans, available to veterans and active military personnel, provide favorable terms and often do not require a down payment. Jumbo loans, intended for high-value properties, typically have stricter qualification criteria and higher interest rates. Vennett stresses the importance of exploring these options to find the best fit for individual circumstances.

Throughout his explanation, Vennett emphasizes the need for thorough research and comparison shopping when selecting a mortgage. He recommends consulting with multiple lenders to obtain competitive rates and terms. Vennett also advises considering the impact of additional fees, such as closing costs and private mortgage insurance, on the overall cost of the mortgage. By taking a comprehensive approach to understanding and evaluating different mortgage types, Vennett believes that homebuyers can make more informed decisions and achieve their homeownership goals.

Liberation from Debt: The Joy of a Mortgage-Free Life

You may want to see also

Explore related products

$4.95 $14.95

![]()

Mortgage Process: Vennett outlines the steps involved in obtaining a mortgage, from application to closing

Jared Vennett explains the modern mortgage process as a series of intricate steps that require careful navigation. He begins by emphasizing the importance of preparation before even starting the application process. This includes reviewing one's credit score, gathering necessary financial documents, and understanding the different types of mortgages available. Vennett advises potential homebuyers to get pre-approved for a mortgage to gain a clear understanding of their budget and to make their offer more attractive to sellers.

Once pre-approved, Vennett outlines the formal application process, which involves submitting detailed financial information to the lender. This step is critical, as it determines the loan amount and interest rate the borrower will receive. Vennett stresses the importance of accuracy and completeness in the application to avoid delays or rejection.

After the application is submitted, the lender will order an appraisal of the property to ensure its value aligns with the loan amount. Vennett explains that this step is crucial for both the lender and the borrower, as it prevents overpaying for a property. He also notes that the appraisal can sometimes lead to negotiations between the buyer and seller if the property is valued lower than expected.

Following the appraisal, the lender will review the application and make a decision on the loan. If approved, the borrower will receive a loan commitment letter outlining the terms of the mortgage. Vennett highlights the importance of carefully reviewing this document to understand all the terms and conditions of the loan.

The final step in the mortgage process, according to Vennett, is the closing. This is where the borrower signs the final loan documents and receives the keys to their new home. Vennett explains that the closing process can be lengthy and complex, involving various parties such as the lender, attorney, and title company. He advises borrowers to be patient and prepared for any last-minute issues that may arise.

Throughout the mortgage process, Vennett emphasizes the importance of staying informed and proactive. By understanding each step and being prepared for potential challenges, borrowers can increase their chances of a smooth and successful mortgage experience.

Explore related products

![]()

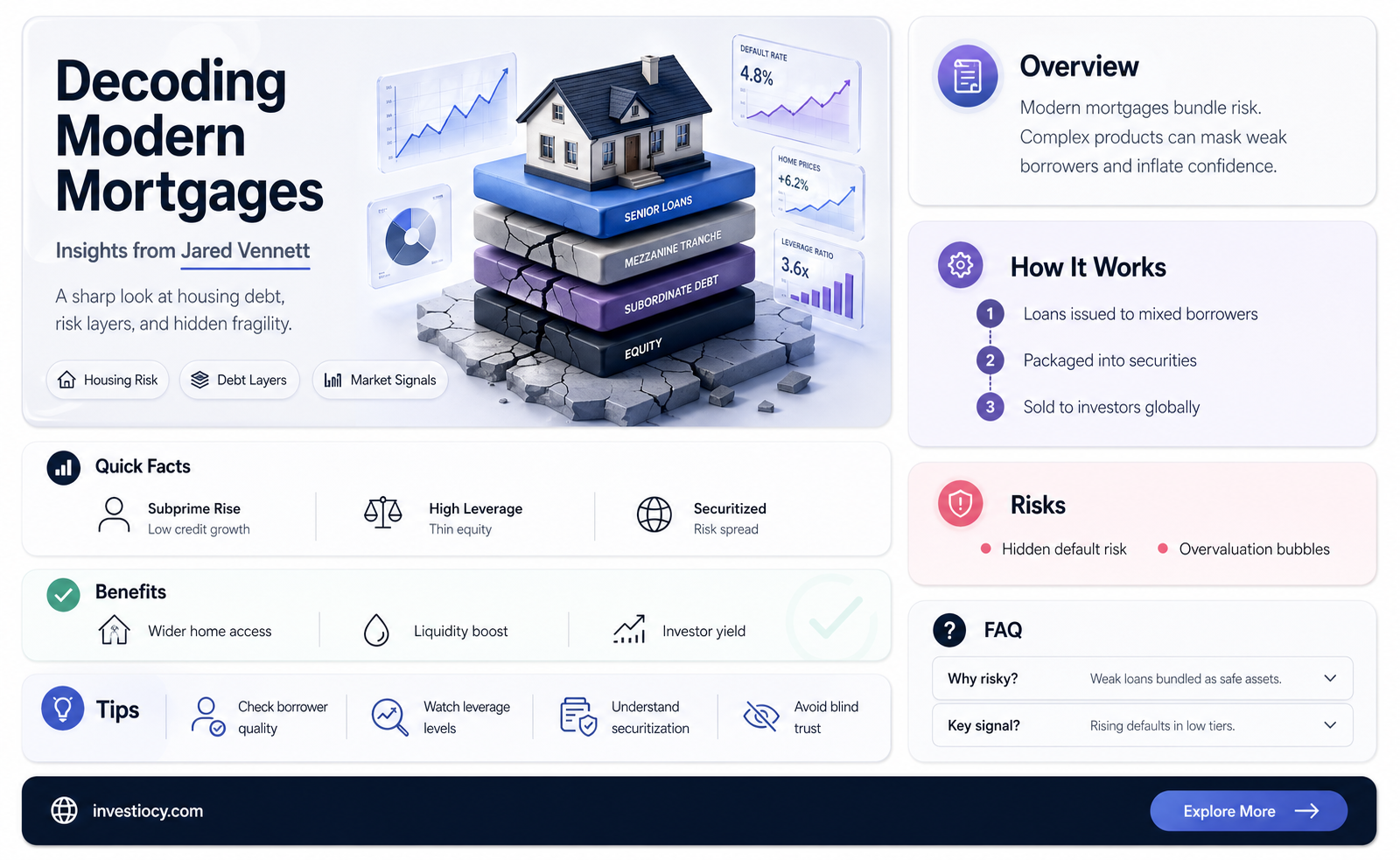

Economic Impact: He discusses how mortgages influence the economy, including their role in financial crises

Jared Vennett delves into the profound economic impact of mortgages, particularly their role in financial crises. He explains that mortgages are a critical component of the housing market, which in turn is a significant driver of economic growth. When the housing market booms, it stimulates construction, real estate, and related industries, creating jobs and boosting consumer spending. However, this boom can also lead to a bubble, where housing prices become inflated and unsustainable.

Vennett highlights the dangers of predatory lending and the proliferation of subprime mortgages, which were major contributors to the 2008 financial crisis. These risky loans, often with adjustable interest rates and minimal down payments, were marketed to borrowers who couldn't afford them. When interest rates rose and housing prices fell, many homeowners defaulted on their mortgages, leading to a cascade of foreclosures and a severe contraction in the housing market.

The crisis had far-reaching consequences, including a global recession, widespread job losses, and a significant decline in consumer wealth. Vennett argues that the crisis was exacerbated by the complex financial instruments that were built on top of these risky mortgages, such as mortgage-backed securities and collateralized debt obligations. These instruments allowed banks and investors to spread the risk of mortgage defaults, but they also amplified the losses when the crisis hit.

Vennett emphasizes the need for regulatory reforms to prevent such crises in the future. He advocates for stricter lending standards, greater transparency in the mortgage market, and more robust risk management practices. By addressing these issues, Vennett believes that mortgages can continue to play a vital role in the economy without posing a systemic risk.

![]()

Future Trends: Jared Vennett speculates on future trends in the mortgage industry, considering technological and regulatory changes

Jared Vennett envisions a mortgage industry transformed by technological advancements and regulatory shifts. He predicts that the future will see a significant increase in the use of digital platforms for mortgage applications and processing. This shift will not only streamline the process but also enhance the customer experience by providing real-time updates and personalized service.

One of the key technological trends Vennett identifies is the rise of artificial intelligence (AI) and machine learning in mortgage underwriting. These technologies will enable lenders to analyze vast amounts of data more efficiently, leading to more accurate risk assessments and potentially lower interest rates for borrowers. Additionally, blockchain technology is expected to play a crucial role in improving the security and transparency of mortgage transactions.

From a regulatory perspective, Vennett anticipates that there will be a continued focus on consumer protection and financial stability. This may lead to stricter lending standards and more robust oversight of mortgage servicers. However, he also believes that regulators will recognize the benefits of technological innovation and work to create an environment that encourages its adoption.

Vennett's predictions for the future of the mortgage industry are both exciting and challenging. While technological advancements promise to make mortgages more accessible and affordable, they also raise important questions about privacy, security, and the role of human interaction in the lending process. As the industry evolves, it will be crucial for lenders, regulators, and consumers to work together to ensure that these changes benefit all parties involved.

Frequently asked questions

Jared Vennett explains that modern mortgages have become overly complex due to the bundling and securitization of loans, making it difficult for even experts to fully understand all the intricacies involved.

Jared Vennett highlights that the risks associated with modern mortgage practices include potential fraud, misrepresentation of risk, and the creation of a housing bubble due to the lack of transparency and oversight in the mortgage-backed securities market.

Jared Vennett suggests simplifying the mortgage process by increasing transparency, reducing the number of intermediaries involved, and implementing stricter regulations to ensure that all parties involved in the mortgage process are held accountable for their actions.