Chapter 7 bankruptcy, often referred to as liquidation bankruptcy, is a legal process that allows individuals and businesses to eliminate most of their unsecured debts. One common question that arises when considering Chapter 7 bankruptcy is whether it can wipe out loan deficiencies. Loan deficiencies occur when the value of collateral securing a loan is less than the amount owed on the loan. In a Chapter 7 bankruptcy, the debtor's assets are sold to pay off creditors, and any remaining unsecured debt is typically discharged. However, the treatment of loan deficiencies can be complex and depends on various factors, including the type of loan, the collateral involved, and the specific circumstances of the debtor.

| Characteristics | Values |

|---|---|

| Legal Process | Chapter 7 bankruptcy |

| Purpose | Liquidation of assets to pay off debts |

| Eligibility | Individuals, businesses, and corporations |

| Filing Requirements | Completion of credit counseling, filing of petition and schedules, payment of filing fee |

| Automatic Stay | Stops most collection actions against the debtor |

| Asset Liquidation | Non-exempt assets are sold by the trustee |

| Debt Discharge | Most unsecured debts are discharged |

| Exemptions | Certain assets like primary residence, vehicle, and retirement accounts are protected |

| Credit Impact | Significant negative impact on credit score |

| Duration | Typically 4-6 months from filing to discharge |

| Alternatives | Chapter 13 bankruptcy, debt consolidation, loan modification |

| Legal Representation | Highly recommended to have an attorney |

| Filing Fee | Varies by court, typically around $335 |

| Means Test | Determines eligibility based on income and expenses |

| Secured Debts | May need to be reaffirmed or paid in full |

| Tax Implications | Debts discharged may be considered taxable income |

Explore related products

What You'll Learn

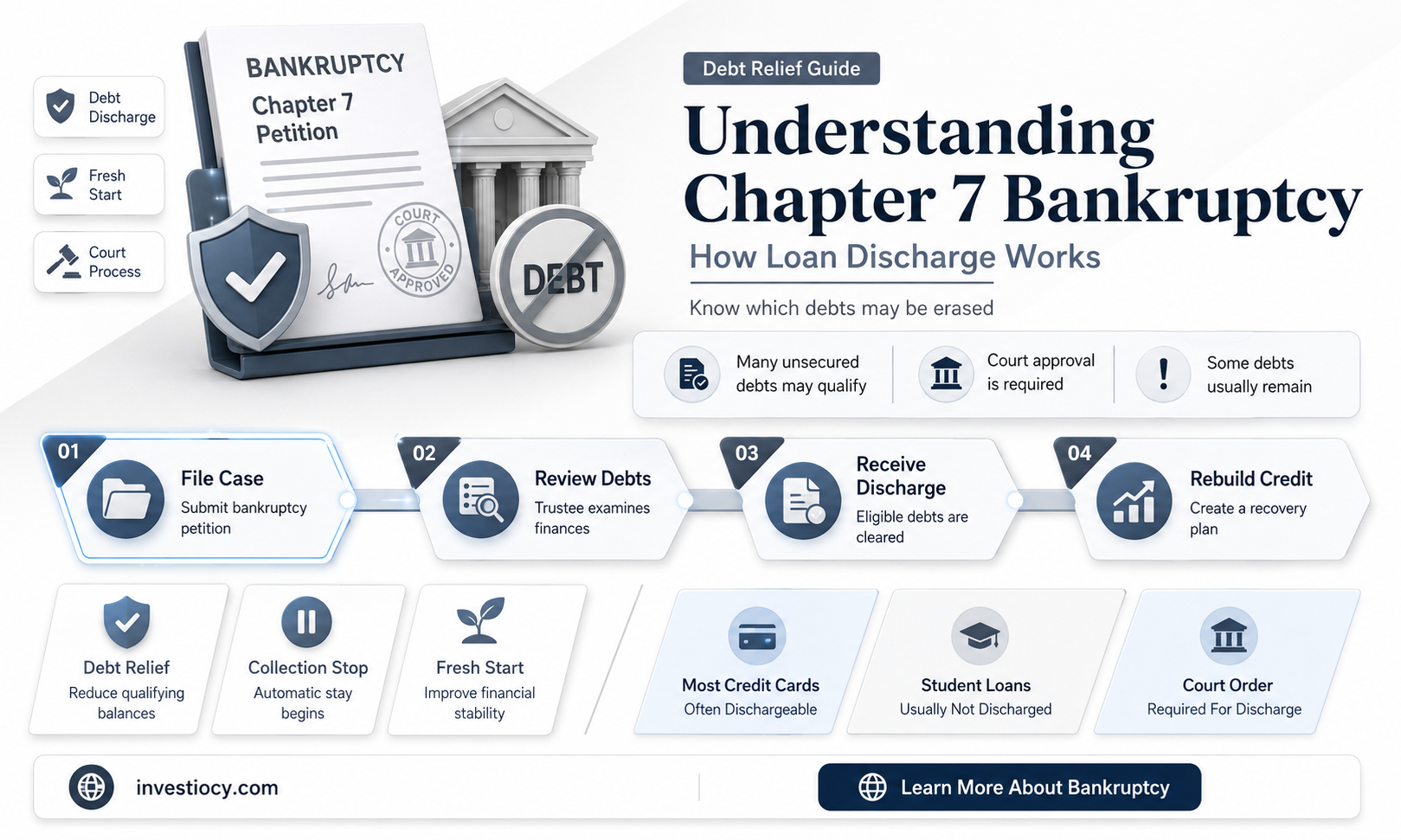

- Chapter 7 Bankruptcy: Provides a fresh start by discharging most debts, including loans

- Loan Discharge: Certain loans may be discharged, but criteria vary

- Secured vs. Unsecured Loans: Treatment differs; secured loans may require asset liquidation

- Student Loans: Generally not dischargeable, but exceptions exist

- Credit Impact: Bankruptcy affects credit scores, but loan discharge can provide financial relief

![]()

Chapter 7 Bankruptcy: Provides a fresh start by discharging most debts, including loans

Chapter 7 bankruptcy is often referred to as a "fresh start" bankruptcy because it allows debtors to discharge most of their unsecured debts, including loans, credit card balances, and medical bills. This type of bankruptcy is designed to give individuals a clean slate financially, free from the burden of overwhelming debt. However, it's important to note that not all debts can be discharged in Chapter 7 bankruptcy. Certain types of debts, such as student loans, child support, and alimony, are typically nondischargeable. Additionally, secured debts, like mortgages and car loans, may not be discharged unless the debtor surrenders the collateral.

One of the primary benefits of Chapter 7 bankruptcy is the speed at which it can be completed. Unlike Chapter 13 bankruptcy, which involves a repayment plan that can last several years, Chapter 7 bankruptcy can be completed in a matter of months. This makes it an attractive option for individuals who are facing significant financial hardship and need immediate relief from their debts. However, it's important to consider the long-term consequences of filing for Chapter 7 bankruptcy, as it can have a significant impact on one's credit score and ability to obtain credit in the future.

Before filing for Chapter 7 bankruptcy, debtors are required to complete a credit counseling course and pass a means test. The means test is designed to determine whether the debtor's income is below the median income for their state and family size. If the debtor's income is above the median, they may not be eligible to file for Chapter 7 bankruptcy. Additionally, debtors must disclose all of their assets and liabilities in their bankruptcy petition, and they may be required to attend a meeting of creditors.

In conclusion, Chapter 7 bankruptcy can provide a fresh start for individuals who are struggling with overwhelming debt. However, it's important to carefully consider the potential consequences and to ensure that all eligibility requirements are met before filing. Debtors should consult with a qualified bankruptcy attorney to determine whether Chapter 7 bankruptcy is the right option for their specific financial situation.

Exploring Chapel Hill Library's Wi-Fi Loan Services: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Loan Discharge: Certain loans may be discharged, but criteria vary

Certain loans can indeed be discharged under specific circumstances, but the criteria for discharge vary significantly depending on the type of loan and the borrower's situation. For instance, federal student loans may be discharged if the borrower becomes permanently disabled or if the school they attended closes permanently. Private student loans, however, are generally not dischargeable in bankruptcy unless the borrower can prove undue hardship.

In the context of Chapter 7 bankruptcy, the discharge of loans is a complex process. While Chapter 7 bankruptcy can wipe out many types of unsecured debt, it does not automatically discharge all loans. Secured loans, such as mortgages and car loans, typically require the debtor to either reaffirm the debt or surrender the collateral. Unsecured loans, like credit card debt and personal loans, are generally discharged, but this does not include student loans unless the debtor meets the aforementioned undue hardship criteria.

The undue hardship standard is particularly stringent. To qualify, the debtor must demonstrate that repaying the student loans would cause them significant financial distress, preventing them from maintaining a basic standard of living. This often involves showing that the debtor's income is insufficient to cover their necessary expenses and loan payments, and that this situation is likely to persist in the future.

Moreover, the discharge of loans in bankruptcy can have long-term implications for the debtor's credit score and financial stability. While bankruptcy can provide a fresh start, it also remains on the debtor's credit report for several years, potentially affecting their ability to obtain new credit or loans. Therefore, it is crucial for individuals considering bankruptcy to carefully weigh the potential benefits against the long-term consequences.

In summary, while certain loans can be discharged under specific circumstances, the process is not straightforward and requires careful consideration of the debtor's unique situation. Understanding the criteria for loan discharge and the implications of bankruptcy is essential for making informed financial decisions.

Navigating Bankruptcy: Can Chapter 7 Discharge Your Student Loans?

You may want to see also

Explore related products

![]()

Secured vs. Unsecured Loans: Treatment differs; secured loans may require asset liquidation

In the realm of bankruptcy, particularly Chapter 7, the distinction between secured and unsecured loans is paramount. Secured loans, which are backed by collateral such as a home or vehicle, are treated differently from unsecured loans, like credit card debt or personal loans. One of the key differences lies in the potential requirement for asset liquidation in secured loans.

When a debtor files for Chapter 7 bankruptcy, they may be required to liquidate certain assets to pay off secured creditors. This process can involve selling the collateral that secures the loan, such as a house or car. The proceeds from the sale are then used to repay the secured debt. However, unsecured loans do not have this liquidation requirement, as they are not backed by any specific asset.

The treatment of secured and unsecured loans in Chapter 7 bankruptcy can have significant implications for debtors. For those with secured loans, the possibility of losing assets can be a major concern. On the other hand, unsecured loans may be discharged more easily, as they do not have the same level of protection for creditors. Debtors must carefully consider these differences when deciding whether to file for bankruptcy and how to manage their debts.

In conclusion, the distinction between secured and unsecured loans is a critical aspect of Chapter 7 bankruptcy. Secured loans may require asset liquidation, while unsecured loans do not. This difference can have a substantial impact on debtors' financial situations and decisions regarding bankruptcy.

Navigating Title Loans: Insights from Chapter 128

You may want to see also

Explore related products

![]()

Student Loans: Generally not dischargeable, but exceptions exist

Student loans are generally not dischargeable in bankruptcy, but there are exceptions to this rule. One such exception is if the debtor can prove that repaying the student loans would cause undue hardship. This is a high bar to meet, but it is possible in certain circumstances. For example, if a debtor is disabled and unable to work, or if they have a large number of dependents and a low income, they may be able to demonstrate undue hardship.

Another exception is if the student loans are not federally guaranteed. Private student loans may be dischargeable in bankruptcy, depending on the specific terms of the loan and the bankruptcy laws in the debtor's state. It is important to note that the discharge of private student loans is not automatic, and the debtor must still file a petition with the bankruptcy court to have the loans discharged.

In addition to these exceptions, there are also programs available that can help debtors manage their student loan debt. For example, income-driven repayment plans can lower monthly payments based on the debtor's income and family size. Public service loan forgiveness programs can also help debtors who work in certain public service fields, such as teaching or nursing, to have their student loans forgiven after a certain number of years of service.

It is important for debtors to understand their options when it comes to student loan debt and bankruptcy. While student loans are generally not dischargeable, there are exceptions and programs available that can help debtors manage their debt and avoid default. Debtors should consult with a bankruptcy attorney to discuss their specific situation and determine the best course of action.

Exploring Cashfloat: A Comprehensive Guide to US Loan Services

You may want to see also

Explore related products

![]()

Credit Impact: Bankruptcy affects credit scores, but loan discharge can provide financial relief

Bankruptcy can have a significant impact on an individual's credit score, often leading to a substantial drop. This is because bankruptcy is considered a major derogatory mark on a credit report, indicating to lenders that the individual has had difficulty managing their debts. The extent of the impact can vary depending on the type of bankruptcy filed, with Chapter 7 bankruptcy typically having a more severe effect than Chapter 13.

Chapter 7 bankruptcy involves the liquidation of assets to pay off debts, and it can result in a credit score drop of 200 to 300 points or more. This is because it indicates a complete inability to repay debts, which can make lenders wary of extending credit in the future. However, the impact of Chapter 7 bankruptcy on credit scores is not permanent. Over time, as the individual rebuilds their credit history through responsible financial management, their score can gradually improve.

One of the primary benefits of filing for Chapter 7 bankruptcy is the potential for loan discharge. This means that certain unsecured debts, such as credit card balances and personal loans, can be completely eliminated, providing significant financial relief. While this may seem like a straightforward solution to debt problems, it's important to consider the long-term consequences on creditworthiness.

Rebuilding credit after a Chapter 7 bankruptcy can be challenging, but it is possible. Individuals can start by obtaining a secured credit card or a credit-builder loan, which can help establish a positive payment history. It's also crucial to monitor credit reports for errors and to dispute any inaccuracies that may be negatively impacting the credit score.

In conclusion, while Chapter 7 bankruptcy can have a detrimental effect on credit scores, it can also provide a fresh start for individuals struggling with overwhelming debt. By understanding the impact of bankruptcy on credit and taking proactive steps to rebuild credit history, individuals can work towards financial recovery and improved creditworthiness over time.

Exploring Loan Modification Options with Cenlar: A Comprehensive Guide

You may want to see also

Frequently asked questions

Chapter 7 bankruptcy can discharge many types of unsecured debts, such as credit card debt and personal loans. However, certain loans, like student loans, are generally not dischargeable unless you can prove undue hardship.

Filing for Chapter 7 bankruptcy will likely have a significant negative impact on your credit score. It can drop your score by several hundred points and remain on your credit report for up to 10 years.

In Chapter 7 bankruptcy, you may be able to keep certain assets that are considered exempt. These can include your primary residence, vehicle, and retirement accounts, among others. However, non-exempt assets may be sold to pay off creditors.

Yes, there is a waiting period. You must wait at least eight years from the date of your previous Chapter 7 bankruptcy discharge before you can file for Chapter 7 again.