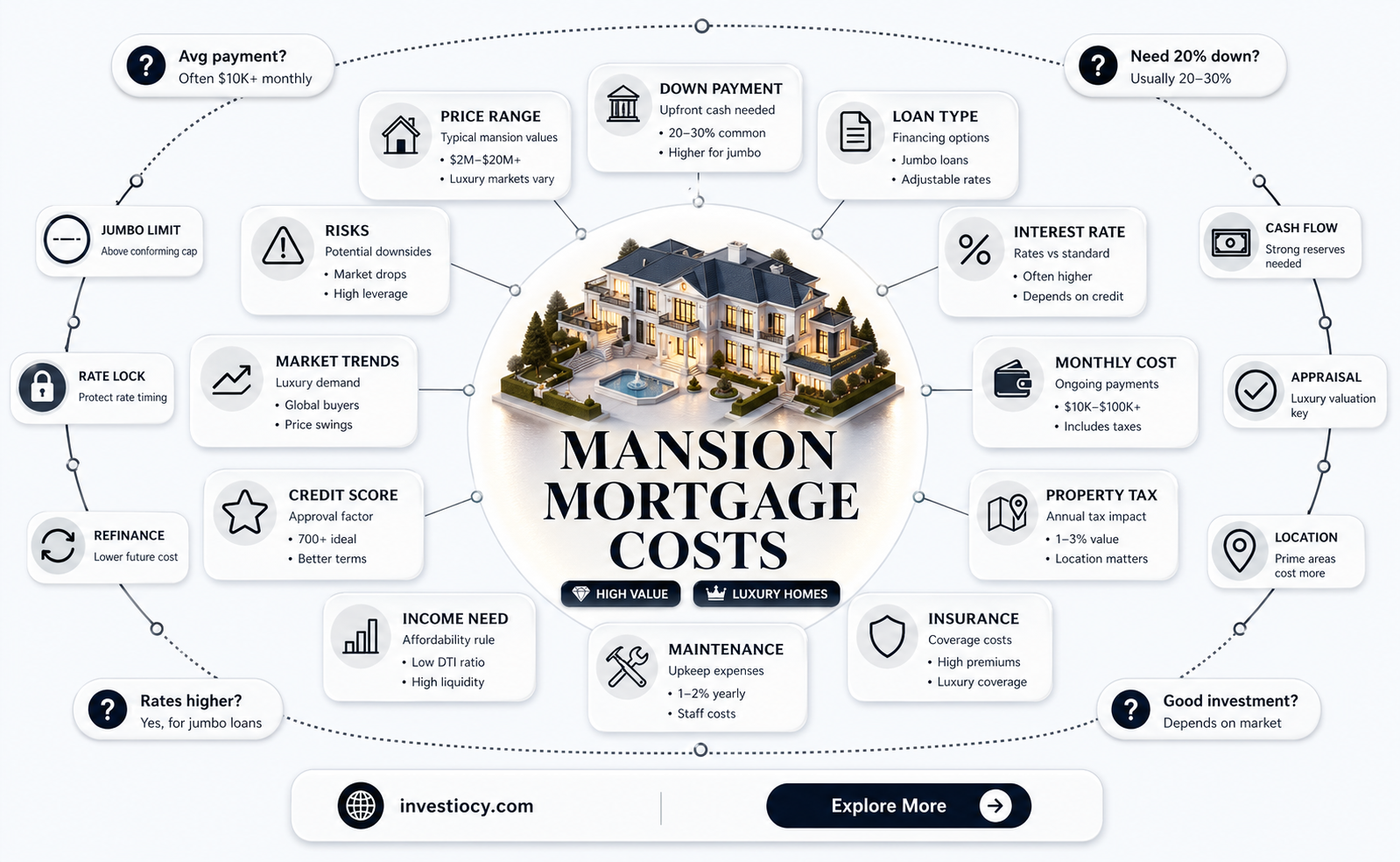

The average mortgage on a mansion can vary significantly depending on several factors, including the location, size, and amenities of the property, as well as the current interest rates and the buyer's financial situation. Typically, mansions are considered luxury properties and can range from a few million to tens of millions of dollars. As a result, the average mortgage on a mansion can be quite substantial, often requiring a large down payment and resulting in high monthly payments. For example, a $5 million mansion with a 20% down payment and a 30-year fixed mortgage at a 4% interest rate would result in a monthly payment of approximately $19,000. However, it's important to note that these figures can vary widely based on the specific circumstances of the purchase.

Explore related products

What You'll Learn

![]()

Location: Urban vs. Rural

The disparity between urban and rural locations significantly impacts the average mortgage on a mansion. In urban areas, mansions are often situated in prime locations with high demand, leading to substantially higher property values. This is driven by factors such as proximity to business districts, luxury amenities, and prestigious schools. As a result, the average mortgage for an urban mansion can easily exceed several million dollars, with some of the most expensive properties reaching tens of millions.

In contrast, rural mansions, while still luxurious, tend to have lower property values due to their remote locations. These properties may offer expansive grounds and privacy but lack the convenience and status associated with urban addresses. The average mortgage for a rural mansion can vary widely, from just under a million to several million dollars, depending on the specific location and amenities.

When comparing urban and rural mortgages, it's essential to consider the cost of living and local property taxes, which can significantly affect the overall financial burden. Urban areas often have higher property taxes and living costs, which can make the mortgage payments on a mansion more substantial despite the higher property values. Conversely, rural areas may have lower taxes and living costs, potentially offsetting the lower property values.

Another critical factor to consider is the availability of financing options. Urban mansions may have more financing opportunities due to their higher demand and value, whereas rural properties might face more limited options, potentially leading to higher interest rates or stricter loan terms.

Ultimately, the choice between an urban and rural mansion depends on individual preferences and financial capabilities. While urban mansions offer prestige and convenience, rural properties provide privacy and a connection to nature. Understanding the mortgage implications of each location is crucial for making an informed decision.

Explore related products

![]()

Size and Features: Impact on Mortgage

The size of a mansion significantly impacts the mortgage amount due to the direct correlation between property value and the loan required to purchase it. Larger mansions typically have higher property values, which in turn lead to larger mortgage loans. For instance, a 10,000 square foot mansion in a prime location could easily cost several million dollars, necessitating a substantial mortgage.

Features of a mansion also play a crucial role in determining the mortgage. High-end features such as swimming pools, home theaters, and state-of-the-art kitchens increase the property's value and, consequently, the mortgage. Additionally, the number of bedrooms and bathrooms, the quality of materials used in construction, and the presence of luxury amenities all contribute to a higher mortgage amount.

When calculating the mortgage for a mansion, lenders consider the property's size and features alongside other factors such as the buyer's credit score, income, and debt-to-income ratio. This comprehensive evaluation ensures that the mortgage is manageable for the buyer while also protecting the lender's investment.

In summary, the size and features of a mansion have a direct and significant impact on the mortgage amount. Larger properties with high-end features typically require larger loans, making it essential for potential buyers to carefully consider their financial situation before purchasing a mansion.

Explore related products

![]()

Current Market Trends

The current market trends for mansions reveal a fascinating landscape shaped by economic fluctuations, changing consumer preferences, and evolving financial regulations. One notable trend is the increasing demand for luxury properties in suburban and rural areas, driven by a desire for more space and privacy among affluent buyers. This shift has led to a rise in the average mortgage amounts for mansions in these locations, as buyers are willing to invest more in their dream homes.

Another significant trend is the impact of interest rates on the mortgage market. With interest rates remaining relatively low, many buyers are opting for larger mortgages to take advantage of the favorable borrowing conditions. This has resulted in an increase in the average mortgage amount for mansions across the board, as buyers are able to afford more expensive properties without significantly increasing their monthly payments.

Furthermore, the growing popularity of jumbo loans has also contributed to the rise in average mortgage amounts for mansions. These loans, which exceed the conforming loan limits set by Fannie Mae and Freddie Mac, allow buyers to finance more expensive properties with a single mortgage. As a result, lenders have become more competitive in offering jumbo loan options, leading to more favorable terms and lower interest rates for borrowers.

In addition to these trends, the increasing prevalence of cash buyers in the luxury property market has also had an impact on average mortgage amounts. Cash buyers, who are not constrained by mortgage limits or interest rates, are able to offer higher prices for mansions, driving up the overall market value and, in turn, the average mortgage amount for those who do choose to finance their purchases.

Overall, the current market trends for mansions suggest a dynamic and evolving landscape, with a range of factors influencing the average mortgage amount for these luxury properties. As the market continues to shift, it will be interesting to see how these trends develop and what new factors emerge to shape the future of the luxury property market.

Explore related products

![NMLS Study Guide 2026-2027 - 5 Full-Length Practice Tests, SAFE MLO Exam Prep Secrets Book for the Mortgage Loan Originator Exam: [4th Edition]](https://m.media-amazon.com/images/I/717iHac5CwL._AC_UL320_.jpg)

![]()

Interest Rates: Fixed vs. Variable

The choice between fixed and variable interest rates is a pivotal decision when securing a mortgage, especially for high-value properties like mansions. Fixed interest rates offer stability and predictability, ensuring that the borrower's monthly payments remain constant throughout the loan term. This can be particularly advantageous in a rising interest rate environment, as it protects the borrower from future increases. However, fixed rates are typically higher than variable rates at the outset, which can result in higher initial monthly payments.

Variable interest rates, on the other hand, fluctuate based on market conditions, which can lead to lower initial payments compared to fixed rates. This can be an attractive option for borrowers who expect interest rates to remain low or decrease over time. However, the unpredictability of variable rates can also pose a risk, as rising interest rates can significantly increase monthly payments, potentially leading to financial strain.

When considering a mortgage on a mansion, the implications of choosing between fixed and variable rates are magnified due to the higher loan amounts involved. A slight increase in interest rates can result in substantial changes to monthly payments, making it crucial for borrowers to carefully evaluate their financial situation and future expectations.

To illustrate, let's consider a scenario where a borrower is securing a $1 million mortgage on a mansion. With a fixed interest rate of 4%, the monthly payment would be approximately $4,774. In contrast, a variable interest rate starting at 3% would result in an initial monthly payment of around $4,167. However, if the variable rate were to increase to 5% over the course of the loan, the monthly payment would surge to approximately $5,368.

Ultimately, the decision between fixed and variable interest rates depends on the borrower's risk tolerance, financial stability, and expectations for future interest rate movements. It is essential for borrowers to consult with a financial advisor to determine the most suitable option for their specific circumstances.

Explore related products

![]()

Income Requirements for Approval

Lenders typically require borrowers to meet specific income criteria to qualify for a mortgage on a mansion. This ensures that the borrower has the financial capacity to repay the loan. The exact income requirement varies depending on the lender, the size of the loan, and other factors such as credit score and debt-to-income ratio. However, as a general rule, borrowers should expect to need a substantial income to qualify for a mortgage on a high-value property like a mansion.

For example, if a borrower is applying for a $1 million mortgage, they may need to have an annual income of at least $200,000 to $300,000 or more, depending on the lender's requirements. This is because the monthly mortgage payment on a $1 million loan could be around $5,000 to $6,000 or more, and lenders want to ensure that the borrower has enough income to cover this payment comfortably.

In addition to meeting the income requirements, borrowers will also need to provide proof of their income, such as pay stubs, tax returns, and bank statements. Lenders will review this documentation to verify the borrower's income and ensure that it is stable and reliable. Borrowers who are self-employed or have irregular income may need to provide additional documentation or may face more stringent income requirements.

It's important to note that income is just one factor that lenders consider when approving a mortgage application. Other factors, such as credit score, debt-to-income ratio, and the value of the property, also play a significant role. Borrowers should work with a financial advisor or mortgage broker to understand the specific requirements for their situation and to develop a strategy for qualifying for a mortgage on a mansion.

Frequently asked questions

The average mortgage payment on a mansion can vary significantly depending on factors such as the location, size, and value of the property, as well as the interest rate and loan terms. As of my last update in June 2024, the average mortgage payment on a $1 million home with a 20% down payment and a 30-year fixed-rate mortgage at 4% interest would be approximately $4,774 per month. However, this is just an estimate, and actual payments could be higher or lower based on individual circumstances.

Qualifying for a mortgage on a mansion requires a substantial income. Lenders typically look at your debt-to-income ratio (DTI) to determine how much mortgage you can afford. As a general rule, your total monthly debt payments, including your mortgage, should not exceed 36% to 43% of your gross monthly income. For example, if you're applying for a $1 million mortgage with an estimated monthly payment of $4,774, you would need a gross monthly income of at least $11,000 to $13,500 to meet the DTI requirements. However, this is a rough estimate, and other factors such as credit score, assets, and loan terms can also impact your eligibility.

Mansions often come with unique features that can influence their mortgage rates. Some of these features include:

- Size: Larger properties may require higher mortgage amounts, which can lead to higher monthly payments.

- Location: Mansions in prime locations, such as beachfront or city center, may have higher property values and thus higher mortgage rates.

- Amenities: Luxurious amenities like swimming pools, home theaters, and extensive landscaping can increase the property value and mortgage amount.

- Historical significance: Mansions with historical or architectural significance may be considered higher-risk loans, potentially resulting in higher interest rates.

- Acreage: Properties with large amounts of land may require specialized loans with different terms and rates.

These factors can all impact the mortgage rate and overall cost of owning a mansion, so it's essential to consider them when applying for a mortgage.

![NMLS Study Guide 2026–2027: 10 Full-Length Practice Tests for the SAFE Mortgage Loan Originator (MLO) Exam Prep: [3rd Edition]](https://m.media-amazon.com/images/I/61s4wNIlEcL._AC_UL320_.jpg)