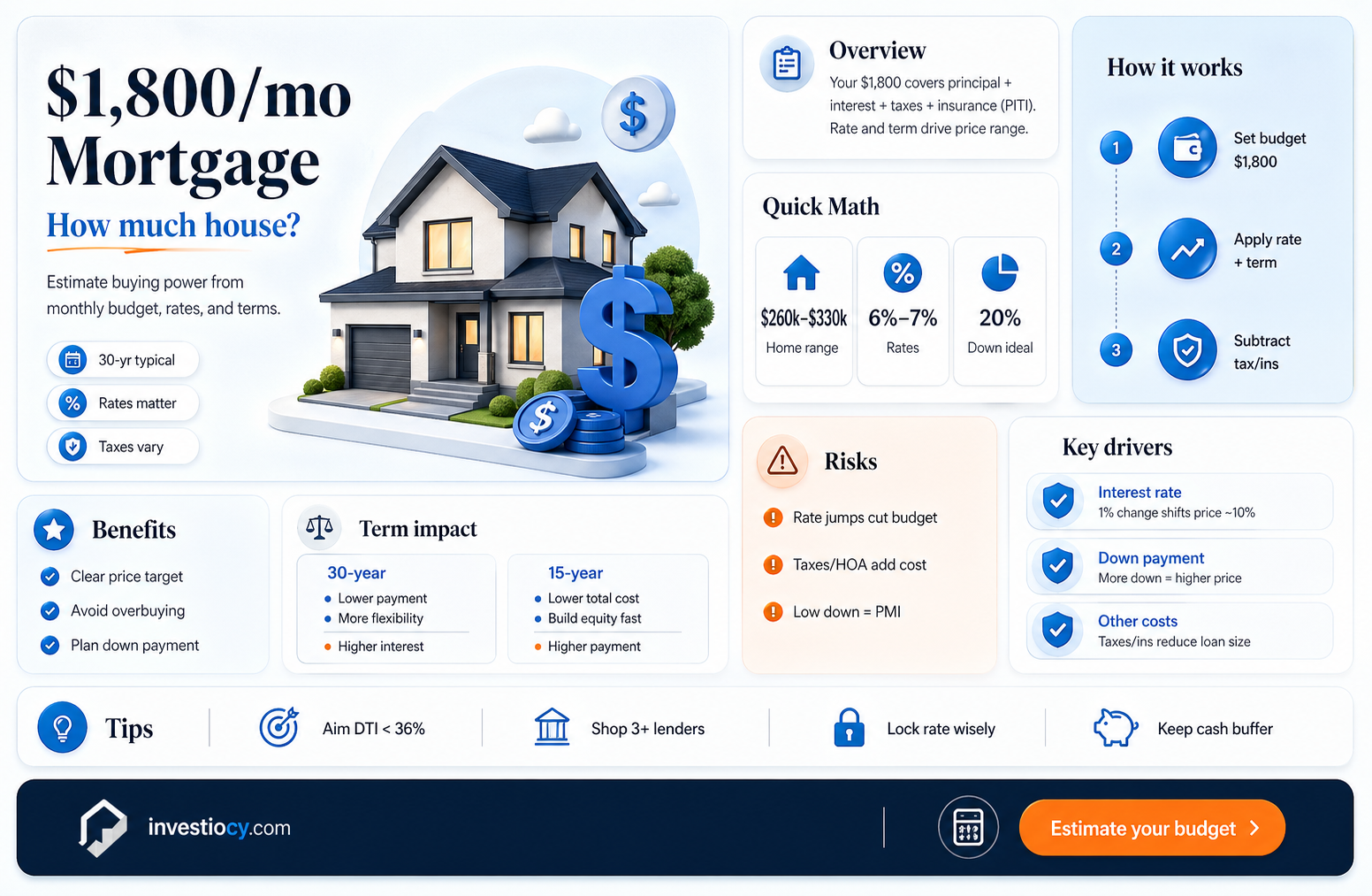

To determine how high a mortgage is at $1,800 a month, we need to consider several factors such as the loan amount, interest rate, and loan term. Assuming a standard 30-year fixed-rate mortgage, we can use a mortgage calculator to estimate the loan amount. For instance, at a 4% interest rate, a $1,800 monthly payment would correspond to a mortgage of approximately $425,000. However, this figure can vary significantly based on the interest rate and loan term. It's essential to note that this calculation does not include additional costs such as property taxes, insurance, and homeowners association fees, which can increase the total monthly payment. Therefore, understanding the full scope of mortgage payments and associated costs is crucial for potential homebuyers.

| Characteristics | Values |

|---|---|

| Monthly Payment | $1,800 |

| Interest Rate | 6.5% |

| Loan Term | 30 years |

| Principal Amount | $300,000 |

| Property Type | Single-family home |

| Location | Urban area |

| Credit Score | 720 |

| Debt-to-Income Ratio | 35% |

| Annual Income | $60,000 |

| Down Payment | 20% |

| Closing Costs | 2% of loan amount |

| Property Taxes | 1.2% of property value |

| Home Insurance | $1,200 per year |

| PMI (if applicable) | 0.5% of loan amount |

| Total Monthly Expenses | $2,200 |

Explore related products

What You'll Learn

- Mortgage Affordability: Calculate income needed to qualify for a mortgage with monthly payments of $1,800

- Interest Rates: Explore how different interest rates impact the principal amount for a $1,800 monthly mortgage

- Loan Terms: Understand the effect of loan terms (15 vs. 30 years) on total interest paid for a mortgage of $1,800 per month

- Down Payment: Determine the required down payment to secure a mortgage with monthly installments of $1,800

- Property Types: Identify types of properties (e.g., single-family homes, condos) that typically have $1,800 monthly mortgages

![]()

Mortgage Affordability: Calculate income needed to qualify for a mortgage with monthly payments of $1,800

To determine the income needed to qualify for a mortgage with monthly payments of $1,800, we need to consider several factors, including the loan amount, interest rate, and loan term. Let's assume a 30-year fixed-rate mortgage with an interest rate of 4%. Using a mortgage calculator, we can determine that the loan amount would be approximately $400,000.

Next, we need to calculate the debt-to-income ratio (DTI), which is the percentage of your gross monthly income that goes towards paying debts. Most lenders prefer a DTI of 36% or less. To calculate the DTI, we'll need to know the borrower's total monthly debt payments, including the mortgage payment, credit card payments, car loans, and any other debts.

Let's assume the borrower has no other debts besides the mortgage. In this case, the DTI would be $1,800 divided by the gross monthly income. To find the gross monthly income needed to qualify for the mortgage, we can rearrange the DTI formula: Gross Monthly Income = Monthly Debt Payments / DTI. Plugging in the numbers, we get Gross Monthly Income = $1,800 / 0.36 = $5,000.

Therefore, the borrower would need a gross monthly income of at least $5,000 to qualify for a mortgage with monthly payments of $1,800. It's important to note that this is just a rough estimate, and the actual income needed may vary depending on other factors, such as credit score, employment history, and assets.

Additionally, it's crucial to consider the borrower's overall financial situation and not just focus on the mortgage payment. The borrower should also have enough savings for a down payment, closing costs, and emergency funds. It's recommended to consult with a financial advisor or mortgage lender to get a more accurate assessment of the borrower's financial situation and determine the best mortgage options available.

Exploring the Heights: Average Mortgage Costs for Mansions Unveiled

You may want to see also

Explore related products

![]()

Interest Rates: Explore how different interest rates impact the principal amount for a $1,800 monthly mortgage

Let's delve into the impact of interest rates on a $1,800 monthly mortgage. We'll explore how varying interest rates can affect the principal amount you owe over time.

First, it's essential to understand that interest rates play a significant role in determining the total cost of your mortgage. A higher interest rate means you'll pay more in interest over the life of the loan, which can significantly increase the overall amount you owe. Conversely, a lower interest rate can help you save money on interest payments and reduce the total cost of your mortgage.

To illustrate this, let's consider an example. Suppose you have a 30-year fixed-rate mortgage with a principal amount of $200,000. If your interest rate is 4%, your monthly payment would be approximately $955. However, if your interest rate increases to 5%, your monthly payment would jump to around $1,074. This increase in monthly payments can add up over time, resulting in a higher total cost for your mortgage.

Now, let's apply this concept to a $1,800 monthly mortgage. If you're paying $1,800 per month, you might assume that you're paying off the principal amount quickly. However, if your interest rate is high, a significant portion of your monthly payment may be going towards interest rather than principal. This can slow down the rate at which you're paying off your mortgage and increase the total amount you owe over time.

To avoid this, it's crucial to shop around for the best interest rate possible. Even a small difference in interest rates can have a significant impact on your monthly payments and the total cost of your mortgage. Additionally, consider making extra payments towards your principal amount whenever possible. This can help you pay off your mortgage faster and reduce the total amount of interest you pay over time.

In conclusion, interest rates have a profound impact on the principal amount you owe for a $1,800 monthly mortgage. By understanding how interest rates work and taking steps to secure the best rate possible, you can save money on your mortgage and pay it off more quickly.

Explore related products

![]()

Loan Terms: Understand the effect of loan terms (15 vs. 30 years) on total interest paid for a mortgage of $1,800 per month

Let's delve into the specifics of how loan terms impact the total interest paid on a mortgage with a monthly payment of $1,800. We'll compare 15-year and 30-year loan terms to illustrate the differences.

First, it's essential to understand that the total interest paid on a mortgage is directly influenced by the loan term. A longer loan term, such as 30 years, will result in more interest paid over the life of the loan compared to a shorter term, like 15 years. This is because the interest rate is applied to the outstanding principal balance for a more extended period.

To quantify this difference, let's consider an example. Assume we have a mortgage of $216,000 (which would result in a monthly payment of approximately $1,800) with an interest rate of 4%. Over 30 years, the total interest paid would be around $144,000. In contrast, if we had the same mortgage but with a 15-year term, the total interest paid would be approximately $62,000. This significant difference highlights the impact of loan terms on the overall cost of a mortgage.

It's also important to note that while a shorter loan term results in less interest paid, it also means higher monthly payments. In our example, the monthly payment for the 15-year loan would be around $2,400, which is substantially higher than the $1,800 payment for the 30-year loan. This trade-off between interest paid and monthly payments is a crucial consideration for borrowers when choosing a loan term.

In conclusion, understanding the effect of loan terms on total interest paid is vital for making informed decisions about a mortgage. By comparing different loan terms and their associated costs, borrowers can choose the option that best fits their financial situation and goals.

Explore related products

![]()

Down Payment: Determine the required down payment to secure a mortgage with monthly installments of $1,800

To determine the required down payment for a mortgage with monthly installments of $1,800, we need to consider several factors, including the loan amount, interest rate, and loan term. Let's break down the process step by step.

First, we need to calculate the total loan amount. Assuming a 30-year fixed-rate mortgage with an interest rate of 4%, we can use a mortgage calculator to find the loan amount that corresponds to a monthly payment of $1,800. This calculation reveals that the loan amount would be approximately $430,000.

Next, we need to determine the down payment percentage required by the lender. This can vary depending on the type of mortgage and the borrower's creditworthiness. For a conventional mortgage, a minimum down payment of 3% is typically required, while FHA loans may require as little as 3.5%. For our example, let's assume a 3% down payment requirement.

Now, we can calculate the down payment amount by multiplying the loan amount by the down payment percentage. In this case, the down payment would be $430,000 x 0.03 = $12,900.

However, it's important to note that this is just the minimum down payment required. Borrowers may choose to make a larger down payment to reduce their monthly payments or to avoid paying private mortgage insurance (PMI). Additionally, some lenders may require a higher down payment for certain types of properties or for borrowers with lower credit scores.

In conclusion, the required down payment to secure a mortgage with monthly installments of $1,800 would be approximately $12,900, assuming a 3% down payment requirement. However, borrowers should be aware that this is just the minimum amount, and they may need to make a larger down payment depending on their individual circumstances and the requirements of their lender.

Explore related products

![]()

Property Types: Identify types of properties (e.g., single-family homes, condos) that typically have $1,800 monthly mortgages

To determine the types of properties that typically have an $1,800 monthly mortgage, we need to consider several factors, including the property type, location, and current market conditions. Single-family homes are a common property type that can have an $1,800 monthly mortgage, especially in suburban areas or smaller cities where the cost of living is lower. For example, in some parts of the Midwest or South, a single-family home with three bedrooms and two bathrooms can be purchased for around $250,000, which would result in an $1,800 monthly mortgage payment with a 20% down payment and a 30-year fixed-rate loan at 4% interest.

Condominiums are another property type that can have an $1,800 monthly mortgage, particularly in urban areas or coastal regions where the cost of living is higher. For instance, in some parts of California or Florida, a two-bedroom, two-bathroom condo can be purchased for around $350,000, which would result in an $1,800 monthly mortgage payment with a 20% down payment and a 30-year fixed-rate loan at 4% interest. However, it's important to note that condo mortgage payments can vary significantly depending on the size, location, and amenities of the building.

Townhouses are a third property type that can have an $1,800 monthly mortgage, offering a middle ground between single-family homes and condos. Townhouses often provide more space and privacy than condos, but less maintenance and yard work than single-family homes. For example, in some parts of the Northeast or Mid-Atlantic, a three-bedroom, two-bathroom townhouse can be purchased for around $300,000, which would result in an $1,800 monthly mortgage payment with a 20% down payment and a 30-year fixed-rate loan at 4% interest.

It's also worth considering other property types, such as duplexes or triplexes, which can have an $1,800 monthly mortgage and provide additional rental income. However, these types of properties often require more maintenance and management than single-family homes or condos. Additionally, it's important to factor in other costs associated with homeownership, such as property taxes, insurance, and homeowners association fees, which can vary significantly depending on the property type and location.

In conclusion, the types of properties that typically have an $1,800 monthly mortgage can vary widely depending on the location, market conditions, and property type. By considering these factors and doing thorough research, potential homebuyers can find a property that fits their budget and lifestyle.

Frequently asked questions

To determine how much mortgage you can afford with a monthly payment of $1,800, you'll need to consider factors like interest rates, loan terms, and your debt-to-income ratio. Generally, a $1,800 monthly payment could correspond to a mortgage amount ranging from $300,000 to $400,000, depending on these factors.

The interest rate for a mortgage with a $1,800 monthly payment can vary based on the loan amount, term, and your creditworthiness. As of my last update in June 2024, interest rates were hovering around 6% to 7%. Using a mortgage calculator, you can estimate that for a $350,000 loan with a 6.5% interest rate and a 30-year term, your monthly payment would be approximately $1,800.

Your credit score plays a significant role in determining the mortgage amount you can secure with a $1,800 monthly payment. A higher credit score typically allows you to borrow more money at a lower interest rate. For instance, with a credit score of 750 or higher, you might be able to get a larger mortgage amount compared to a score of 650, even with the same monthly payment.

In addition to the principal and interest included in your $1,800 monthly mortgage payment, you'll also need to consider other costs such as property taxes, homeowners insurance, and potentially private mortgage insurance (PMI) if your down payment is less than 20%. These additional costs can vary depending on the location and value of the property, as well as your insurance coverage choices.