Calculating interest on an investment is a fundamental aspect of personal finance and investment management. It involves determining the amount of money earned or charged over a specific period based on the principal amount invested, the interest rate, and the duration of the investment. Understanding how to calculate interest is crucial for making informed decisions about savings, loans, and various investment options. This knowledge helps individuals and businesses alike to optimize their financial strategies, ensuring they maximize returns while minimizing costs associated with borrowing.

Explore related products

What You'll Learn

- Simple Interest Formula: Principal amount, interest rate, time period

- Compound Interest Formula: Principal, rate, time, compounding frequency

- Annual Percentage Yield (APY): Compounded interest rate, investment return

- Interest Accrual Methods: Daily, monthly, quarterly, semi-annually, annually

- Investment Types: Stocks, bonds, mutual funds, real estate, interest rates

![]()

Simple Interest Formula: Principal amount, interest rate, time period

The Simple Interest Formula is a fundamental tool in finance, used to calculate the interest earned on an investment over a specific period. This formula is particularly useful for understanding the basics of interest accrual and can be applied to various financial scenarios, from savings accounts to loans.

The formula itself is straightforward and consists of three key components: the principal amount, the interest rate, and the time period. The principal amount is the initial sum of money invested or borrowed. The interest rate is the percentage at which the principal earns interest, typically expressed as an annual rate. The time period is the duration over which the interest is calculated, usually in years.

To calculate simple interest, you multiply the principal amount by the interest rate and then by the time period. The formula can be expressed as:

\[ \text{Simple Interest} = \text{Principal} \times \text{Interest Rate} \times \text{Time Period} \]

For example, if you invest $1,000 at an annual interest rate of 5% for 3 years, the simple interest earned would be:

\[ \text{Simple Interest} = 1000 \times 0.05 \times 3 = 150 \]

This means you would earn $150 in interest over the 3-year period.

One important note is that simple interest does not compound, meaning it does not earn interest on the interest already accrued. This is in contrast to compound interest, where interest is calculated on the principal plus any accumulated interest.

Understanding the Simple Interest Formula is crucial for making informed financial decisions. It allows you to estimate the return on your investments and compare different investment options. Additionally, it can help you understand the cost of borrowing and make better decisions when taking out loans.

In summary, the Simple Interest Formula is a basic yet powerful tool in finance. By understanding how to use this formula, you can gain valuable insights into your financial situation and make more informed decisions about your investments and borrowings.

Smart Investing: A Step-by-Step Guide to Calculating Investment Spending

You may want to see also

Explore related products

![]()

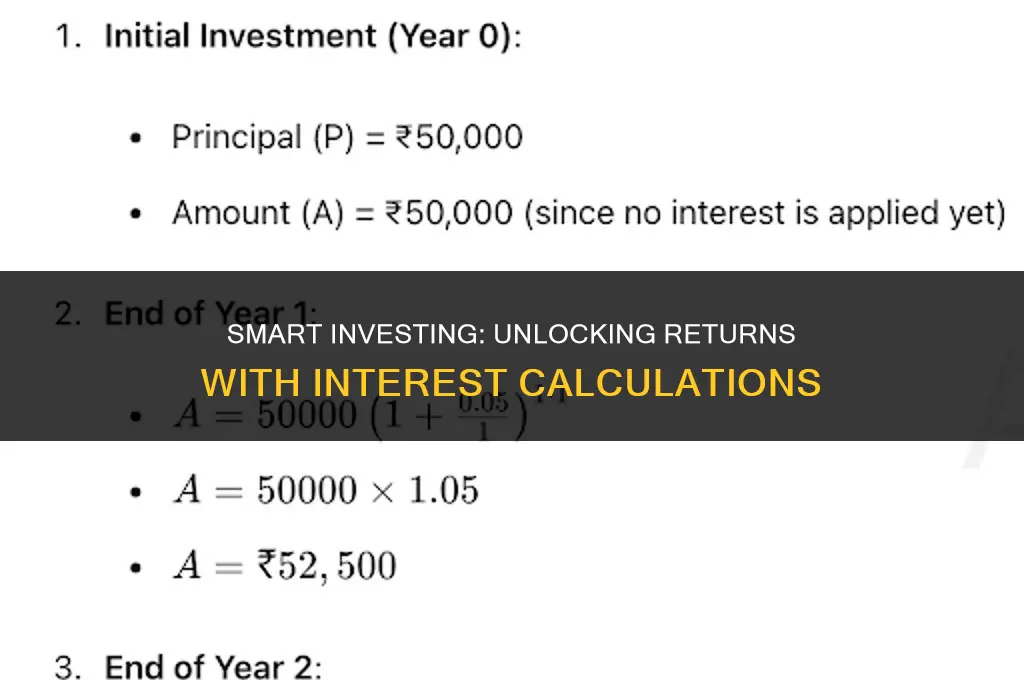

Compound Interest Formula: Principal, rate, time, compounding frequency

The compound interest formula is a powerful tool for calculating the growth of an investment over time. It takes into account four key variables: the principal amount, the interest rate, the time period, and the compounding frequency. Understanding how these components interact is crucial for investors looking to maximize their returns.

The principal amount is the initial sum of money invested. This is the foundation upon which all future growth is built. The interest rate is the percentage of the principal that is earned as interest each year. It's important to note that this rate can vary depending on the type of investment and the market conditions.

Time is another critical factor in the compound interest formula. The longer the investment is held, the more time there is for the interest to compound and grow. This is why it's often recommended to start investing as early as possible, even with small amounts.

The compounding frequency refers to how often the interest is added to the principal. This can be annually, semi-annually, quarterly, or even monthly. The more frequent the compounding, the faster the investment will grow.

To calculate compound interest, you can use the formula: A = P(1 + r/n)^(nt), where A is the amount of money accumulated after n compounding periods, P is the principal amount, r is the annual interest rate (decimal), n is the number of times that interest is compounded per year, and t is the time the money is invested for in years.

For example, let's say you invest $1,000 at an annual interest rate of 5%, compounded quarterly. After 10 years, your investment would grow to approximately $1,628.89. This is significantly more than the $1,500 you would have if the interest were compounded annually.

In conclusion, the compound interest formula is a valuable tool for investors. By understanding how the principal, rate, time, and compounding frequency interact, you can make informed decisions about your investments and watch your money grow over time.

Calculating Gross Investment: A Step-by-Step Guide for Financial Success

You may want to see also

Explore related products

![]()

Annual Percentage Yield (APY): Compounded interest rate, investment return

The Annual Percentage Yield (APY) is a critical metric for investors seeking to understand the true return on their investments. Unlike the Annual Percentage Rate (APR), which only accounts for simple interest, APY takes into account the compounding effect of interest over time. This means that APY provides a more accurate representation of the investment's growth potential.

To calculate APY, you need to know the interest rate, the compounding frequency, and the initial investment amount. The formula for APY is:

APY = (1 + r/n)^(nt) - 1

Where:

- R is the annual interest rate (expressed as a decimal)

- N is the number of compounding periods per year

- T is the time the money is invested (in years)

For example, if you invest $1,000 in a savings account with an annual interest rate of 5% that compounds quarterly, the APY would be:

APY = (1 + 0.05/4)^(4*1) - 1 = 0.050625 or 5.0625%

This means that your investment would grow by 5.0625% over the course of one year, taking into account the compounding effect of interest.

When comparing investment options, it's essential to consider the APY rather than just the APR, as it provides a more comprehensive picture of the investment's potential growth. Additionally, be aware that APY can fluctuate based on changes in interest rates and compounding frequencies, so it's important to review and adjust your investment strategy accordingly.

Smart Investing: How to Calculate Additional Investment for Maximum Returns

You may want to see also

Explore related products

![]()

Interest Accrual Methods: Daily, monthly, quarterly, semi-annually, annually

Interest accrual methods vary depending on the frequency at which interest is calculated and added to the principal amount. The most common methods are daily, monthly, quarterly, semi-annually, and annually. Each method has its own implications for the growth of an investment over time.

Daily accrual is the most frequent method, where interest is calculated every day based on the outstanding principal balance. This method results in the most accurate reflection of the time value of money, as it accounts for the compounding effect on a daily basis. For example, if you have a savings account with a daily accrual interest rate of 1%, the interest earned each day would be added to the principal, and the next day's interest would be calculated on the new, higher balance.

Monthly accrual is another common method, where interest is calculated once a month. This method is often used for loans and credit cards, as it simplifies the calculation process. However, it can result in a slightly lower return on investment compared to daily accrual, as the compounding effect is less frequent.

Quarterly accrual calculates interest every three months, which is a less common method but still used in some investment products. This method strikes a balance between the accuracy of daily accrual and the simplicity of monthly accrual.

Semi-annual accrual calculates interest twice a year, which is often used for bonds and other fixed-income securities. This method results in a lower return on investment compared to more frequent accrual methods, as the compounding effect is less pronounced.

Annual accrual is the least frequent method, where interest is calculated once a year. This method is often used for long-term investments, such as certificates of deposit (CDs), where the interest rate is fixed for the entire term. While annual accrual is the simplest method, it can result in the lowest return on investment due to the infrequent compounding.

In conclusion, the choice of interest accrual method can have a significant impact on the growth of an investment over time. Daily accrual is the most accurate method, but it can also be the most complex. Monthly accrual is a good balance between accuracy and simplicity, while quarterly, semi-annual, and annual accrual methods are less common but still used in various investment products. When choosing an investment, it's important to consider the interest accrual method and how it will affect the overall return on investment.

Unlocking Economic Growth: A Guide to Calculating Investment

You may want to see also

Explore related products

![Yield [Explicit]](https://m.media-amazon.com/images/I/71Hf22OiIWL._AC_UY218_.jpg)

![]()

Investment Types: Stocks, bonds, mutual funds, real estate, interest rates

Understanding the different types of investments is crucial when learning how to calculate interest on investments. Each investment type has its unique characteristics and methods for generating returns.

Stocks: Stocks represent ownership in a company and can generate returns through dividends and capital appreciation. Dividends are portions of a company's profits distributed to shareholders, usually quarterly. Capital appreciation occurs when the stock price increases over time. To calculate the interest or return on a stock investment, you would use the formula:

\[

\text{Return on Stock} = \left( \frac{\text{Current Stock Price} - \text{Initial Stock Price}}{\text{Initial Stock Price}} \right) \times 100

\]

Additionally, if the stock pays dividends, you would calculate the dividend yield:

\[

\text{Dividend Yield} = \left( \frac{\text{Annual Dividend}}{\text{Current Stock Price}} \right) \times 100

\]

Bonds: Bonds are debt securities issued by governments or corporations. They generate returns through interest payments and capital appreciation. The interest rate on a bond is typically fixed and paid periodically, such as semi-annually or annually. To calculate the interest on a bond investment, you would use the formula:

\[

\text{Interest on Bond} = \text{Principal} \times \text{Interest Rate} \times \text{Time Period}

\]

For example, if you invest $1,000 in a bond with a 5% annual interest rate, the interest earned in one year would be:

\[

\text{Interest on Bond} = 1000 \times 0.05 \times 1 = 50

\]

Mutual Funds: Mutual funds are investment vehicles that pool money from multiple investors to invest in a diversified portfolio of stocks, bonds, or other securities. They generate returns through capital appreciation and dividends or interest payments from the underlying investments. To calculate the return on a mutual fund investment, you would use the formula:

\[

\text{Return on Mutual Fund} = \left( \frac{\text{Current Fund Value} - \text{Initial Fund Value}}{\text{Initial Fund Value}} \right) \times 100

\]

Real Estate: Real estate investments can generate returns through rental income, property appreciation, and tax benefits. Rental income is the periodic payment received from tenants. Property appreciation occurs when the property's value increases over time. To calculate the return on a real estate investment, you would use the formula:

\[

\text{Return on Real Estate} = \left( \frac{\text{Current Property Value} - \text{Initial Property Value}}{\text{Initial Property Value}} \right) \times 100

\]

Additionally, if the property generates rental income, you would calculate the rental yield:

\[

\text{Rental Yield} = \left( \frac{\text{Annual Rental Income}}{\text{Current Property Value}} \right) \times 100

\]

Interest Rates: Interest rates play a critical role in determining the returns on various investments. They influence the cost of borrowing and the returns on savings and investments. Central banks set benchmark interest rates, which affect the rates offered by financial institutions on savings accounts, loans, and bonds. To calculate the interest earned on a savings account, you would use the formula:

\[

\text{Interest on Savings} = \text{Principal} \times \text{Interest Rate} \times \text{Time Period}

\]

For example, if you deposit $5,000 in a savings account with a 2% annual interest rate, the interest earned in one year would be:

\[

\text{Interest on Savings} = 5000 \times 0.02 \times 1 = 100

\]

In conclusion, each investment type has its unique method for calculating returns and interest. Understanding these methods is essential for making informed investment decisions and accurately assessing the performance of your investments.

Mastering Cash Flow: A Guide to Calculating Investing Activities

You may want to see also

Frequently asked questions

The formula to calculate simple interest is: Simple Interest = Principal × Rate × Time. Where 'Principal' is the initial amount invested, 'Rate' is the annual interest rate (expressed as a decimal), and 'Time' is the duration of the investment in years.

Compound interest is calculated using the formula: Compound Interest = Principal × [(1 + Rate/n)^(nt) - 1]. Here, 'Principal' is the initial investment, 'Rate' is the annual interest rate (as a decimal), 'n' is the number of times interest is compounded per year, and 't' is the time the money is invested in years.

Simple interest is calculated only on the initial principal amount, whereas compound interest is calculated on the principal plus any accumulated interest. This means compound interest can grow faster over time as it includes interest on interest.

Interest is typically compounded quarterly (four times a year) in many investment accounts, but it can also be compounded monthly, semi-annually, or annually, depending on the specific terms of the investment.