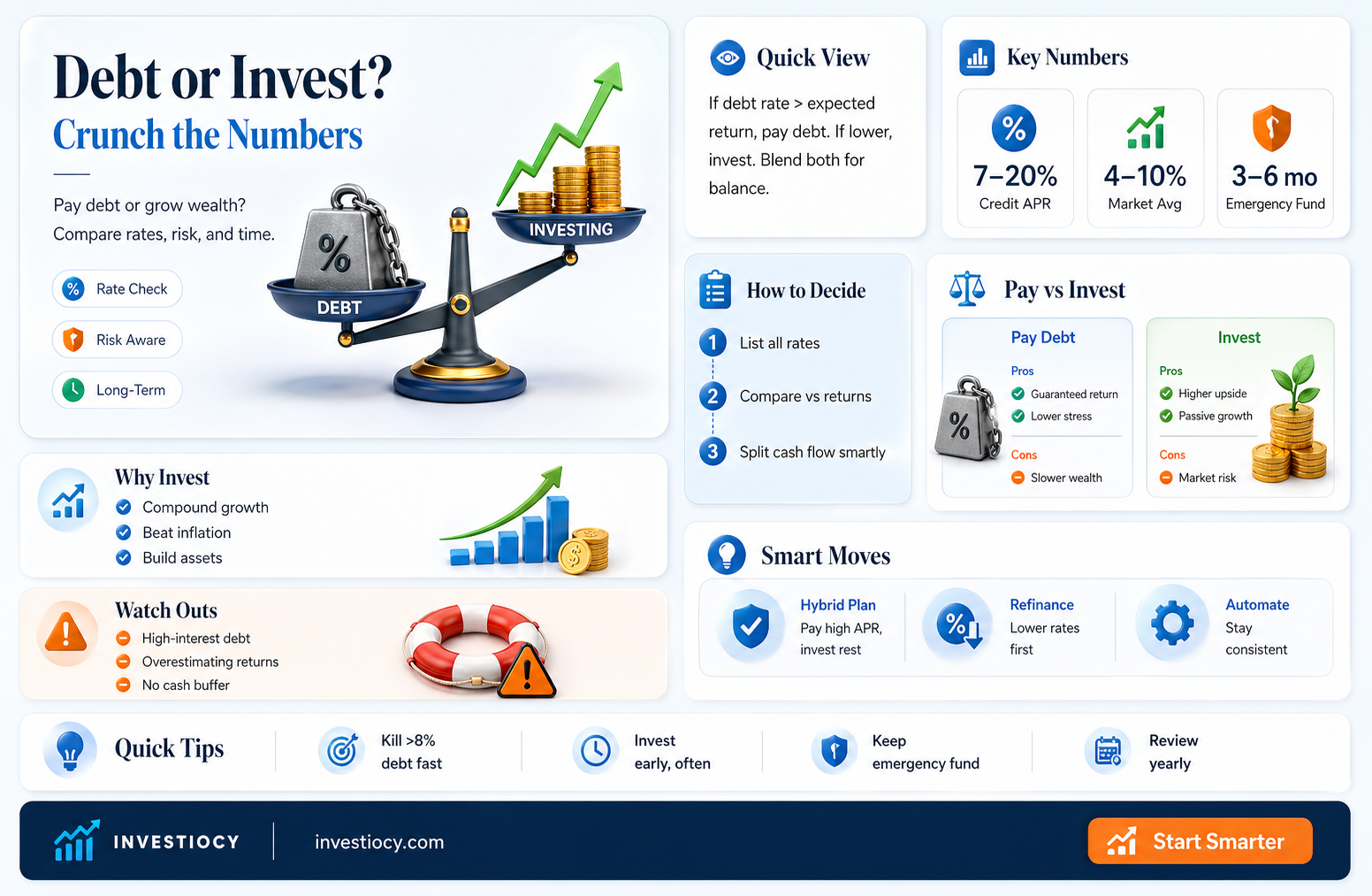

When considering whether to pay off debt or invest, it's essential to weigh the potential benefits and drawbacks of each option. Paying off debt can provide immediate financial relief and reduce the burden of interest payments, while investing can potentially generate long-term wealth growth. A 'should I pay off debt or invest calculator' can help you make an informed decision by comparing the costs and returns of each strategy based on your individual financial situation. This tool typically takes into account factors such as your debt balance, interest rates, investment returns, and time horizon to provide a personalized recommendation. By using such a calculator, you can better understand the trade-offs involved and make a choice that aligns with your financial goals and priorities.

| Characteristics | Values |

|---|---|

| Purpose | Helps individuals decide between paying off debt or investing by comparing potential outcomes |

| Input Parameters | Debt amount, interest rate, investment return rate, time horizon |

| Output Metrics | Break-even point, total wealth accumulation, debt payoff timeline |

| User Interface | Interactive sliders or input fields for parameters, visual charts or graphs for results |

| Algorithm | Utilizes compound interest formulas and Monte Carlo simulations to project future financial scenarios |

| Accuracy | Depends on the precision of input data and the sophistication of the underlying financial model |

| Target Audience | Individuals with disposable income facing decisions about debt repayment versus investment |

| Platform | Available as a web-based tool, mobile app, or software download |

| Cost | Free or freemium models with optional premium features or subscriptions |

| Security | Should employ encryption and secure data storage to protect user financial information |

| Updates | Regularly updated to reflect changes in economic conditions and financial regulations |

| Customer Support | Offers resources such as FAQs, tutorials, and contact options for user assistance |

| Integration | May integrate with other financial tools or services for a more comprehensive financial overview |

| Customization | Allows users to adjust parameters and scenarios to fit their unique financial situations |

| Education | Provides educational resources or explanations to help users understand the financial concepts involved |

Explore related products

What You'll Learn

- Debt vs. Investment Returns: Compare the interest rates on your debt with potential investment returns to determine the best strategy

- Emergency Fund Considerations: Ensure you have an emergency fund in place before deciding between paying off debt or investing

- Types of Debt: Prioritize high-interest debt, such as credit card balances, over lower-interest debt like mortgages or student loans

- Investment Options: Explore various investment options like stocks, bonds, or mutual funds and their associated risks and rewards

- Time Horizon: Consider your financial goals and time horizon when deciding whether to focus on debt repayment or investing for the future

![]()

Debt vs. Investment Returns: Compare the interest rates on your debt with potential investment returns to determine the best strategy

To determine whether to prioritize paying off debt or investing, a critical comparison is necessary: the interest rates on your debt versus the potential returns on your investments. This analysis will help you make an informed decision tailored to your financial situation.

First, gather all the necessary information. List out your debts, including credit card balances, student loans, and mortgages, along with their respective interest rates. Next, research potential investment options such as stocks, bonds, mutual funds, or real estate, and estimate their average returns based on historical data and market trends.

Once you have this information, compare the interest rates on your debt with the expected returns on your investments. If the interest rates on your debt are higher than the potential investment returns, it may be more beneficial to focus on paying off your debt first. This strategy can save you money in the long run by reducing the amount of interest you pay over time.

However, if the potential investment returns are significantly higher than the interest rates on your debt, investing might be the better option. This approach can potentially grow your wealth faster, allowing you to pay off your debt more quickly in the future.

It's also important to consider your risk tolerance and financial goals. If you have a low risk tolerance or are nearing retirement, paying off debt might be the safer choice. On the other hand, if you have a higher risk tolerance and are in your younger years, investing could be more suitable.

In conclusion, the decision between paying off debt and investing depends on a careful analysis of interest rates, potential returns, and your personal financial circumstances and goals. By weighing these factors, you can develop a strategy that best aligns with your financial objectives.

Explore related products

![]()

Emergency Fund Considerations: Ensure you have an emergency fund in place before deciding between paying off debt or investing

Having an emergency fund in place is a critical step before deciding whether to pay off debt or invest. This fund acts as a financial safety net, covering unexpected expenses such as medical bills, car repairs, or sudden job loss. Without an emergency fund, you may be forced to rely on high-interest credit cards or loans, which can exacerbate your debt situation.

The general rule of thumb is to have three to six months' worth of living expenses in your emergency fund. However, this amount may vary depending on your individual circumstances, such as your job stability, health, and existing debt obligations. It's essential to assess your personal situation and adjust your emergency fund goal accordingly.

When building your emergency fund, consider placing it in a high-yield savings account or a money market fund. These options offer liquidity and a higher interest rate than traditional savings accounts, allowing your fund to grow while remaining easily accessible. Avoid investing your emergency fund in volatile assets like stocks or mutual funds, as these carry a higher risk and may not be readily available when you need them.

Once you have established your emergency fund, you can then evaluate whether to prioritize paying off debt or investing. If you have high-interest debt, such as credit card balances, it may be more beneficial to focus on debt repayment first. Conversely, if you have lower-interest debt or are on a stable repayment plan, you may consider investing in assets that can generate long-term growth.

Remember, the decision between paying off debt and investing is not one-size-fits-all. It's crucial to weigh your options carefully, considering factors such as your debt-to-income ratio, interest rates, and long-term financial goals. Consulting with a financial advisor can provide personalized guidance tailored to your specific situation.

Explore related products

![]()

Types of Debt: Prioritize high-interest debt, such as credit card balances, over lower-interest debt like mortgages or student loans

When tackling debt, it's crucial to understand the different types and their implications on your financial health. High-interest debt, such as credit card balances, can quickly spiral out of control due to compounding interest. This makes it essential to prioritize paying off these debts first. On the other hand, lower-interest debt like mortgages or student loans may have more manageable interest rates, but they still require attention to avoid long-term financial strain.

To effectively manage debt, it's important to create a repayment plan that focuses on high-interest debts while still making minimum payments on lower-interest ones. This approach, known as the debt avalanche method, can help you save money on interest and pay off debts faster. For example, if you have a credit card balance with an 18% interest rate and a mortgage with a 4% interest rate, you should allocate more of your repayment budget to the credit card to minimize the impact of compounding interest.

However, it's also essential to consider the potential benefits of investing. While paying off high-interest debt should be a priority, you may want to simultaneously invest in assets that can generate returns higher than the interest rate on your debt. This can be particularly beneficial for long-term financial goals, such as retirement. A balanced approach that combines debt repayment with strategic investing can help you achieve financial stability and growth.

When deciding between paying off debt and investing, it's important to consider your individual financial situation and goals. Factors such as your income, expenses, debt balances, and interest rates should all be taken into account. Additionally, your risk tolerance and investment horizon play a crucial role in determining the right balance between debt repayment and investing.

In conclusion, prioritizing high-interest debt repayment while still considering investment opportunities can be a smart financial strategy. By understanding the different types of debt and their implications, creating a repayment plan, and balancing debt repayment with investing, you can work towards achieving financial stability and long-term growth.

Explore related products

![]()

Investment Options: Explore various investment options like stocks, bonds, or mutual funds and their associated risks and rewards

Investing in stocks offers the potential for high returns but comes with significant risks. Stock prices can fluctuate wildly due to market conditions, company performance, and global events. Investors must be prepared for the possibility of losing a substantial portion of their investment. However, historically, stocks have provided higher returns than other investment options over the long term. For those looking to invest in stocks, it's essential to diversify their portfolio to mitigate risk and consider their investment horizon and risk tolerance.

Bonds are often considered a safer investment option compared to stocks. They provide a fixed income through regular interest payments and the return of the principal amount at maturity. The risk associated with bonds is generally lower, but so are the returns. Bonds are suitable for investors seeking stable income and capital preservation. However, it's crucial to understand the credit quality of the bond issuer and the impact of interest rate changes on bond prices.

Mutual funds offer a way to invest in a diversified portfolio of stocks, bonds, or other securities managed by professional fund managers. They are suitable for investors who want to spread their risk across various assets without having to select individual investments. Mutual funds come with fees and expenses, which can impact overall returns. Investors should carefully consider the fund's investment strategy, performance history, and cost structure before investing.

When deciding between paying off debt and investing, it's important to consider the interest rates on your debt and the potential returns on your investments. If your debt has a high interest rate, it may be more beneficial to pay it off before investing. On the other hand, if you have low-interest debt and the potential for higher returns on your investments, investing might be the better option. It's also crucial to have an emergency fund in place before investing to avoid having to liquidate investments at an inopportune time.

In conclusion, exploring various investment options is essential for making informed decisions about whether to pay off debt or invest. Each investment type has its own risks and rewards, and understanding these can help investors create a balanced strategy that aligns with their financial goals and risk tolerance.

Explore related products

$10.96 $19

![]()

Time Horizon: Consider your financial goals and time horizon when deciding whether to focus on debt repayment or investing for the future

When evaluating whether to prioritize debt repayment or investing, it's crucial to consider your financial goals and time horizon. This decision can significantly impact your long-term financial health and achieving your objectives.

If your financial goals are short-term, such as paying off high-interest debt or saving for a down payment on a house within the next few years, focusing on debt repayment may be more beneficial. By eliminating debt, you can reduce your monthly expenses and free up more money for savings or investments. Additionally, paying off debt can improve your credit score, which can lead to better interest rates on future loans.

On the other hand, if your financial goals are long-term, such as retirement or funding your children's education, investing for the future may be a more effective strategy. By starting to invest early, you can take advantage of compound interest and potentially grow your wealth over time. However, it's essential to ensure that you're not neglecting high-interest debt, as the interest charges can outweigh any potential investment returns.

When deciding between debt repayment and investing, it's also important to consider your risk tolerance. If you're risk-averse, paying off debt may provide a sense of security and stability. Conversely, if you're comfortable with risk, investing may offer the potential for higher returns.

Ultimately, the decision to focus on debt repayment or investing depends on your individual financial situation, goals, and time horizon. It may be helpful to consult with a financial advisor or use a debt repayment vs. investment calculator to determine the best strategy for your specific circumstances.

Frequently asked questions

When deciding between paying off debt and investing, consider the interest rates on your debts and potential investment returns, your financial goals, risk tolerance, and current financial stability.

Use a calculator to compare the long-term costs of your debt with the potential returns on investments. Input variables like interest rates, principal amounts, and time horizons to see which option yields better financial outcomes.

Generally, it's advisable to pay off high-interest debt before investing, as the interest on debt can compound quickly and outweigh potential investment gains. However, consider your overall financial situation and goals before making a decision.