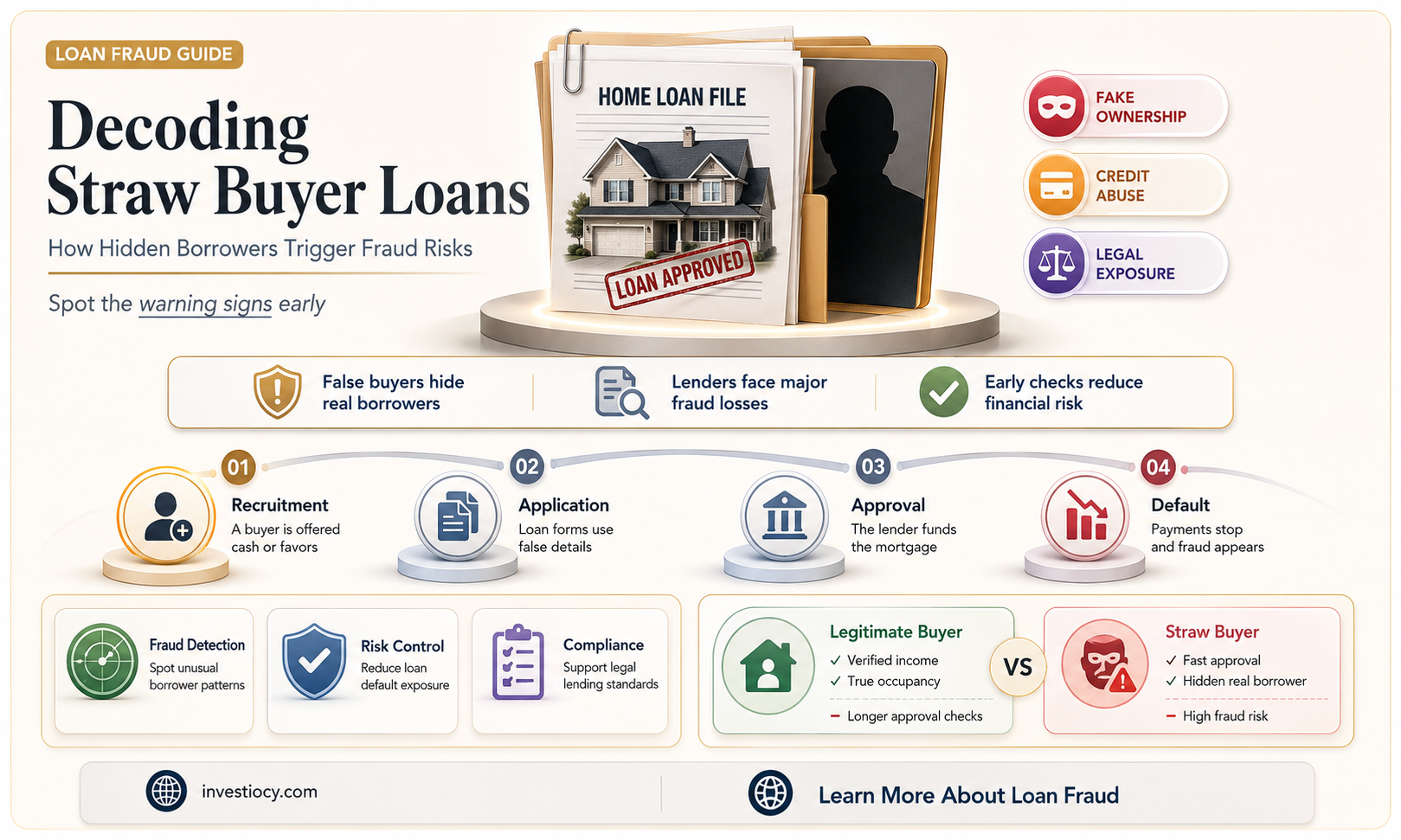

A straw buyer loan is a type of mortgage fraud where an individual, known as the straw buyer, purchases a property using a loan obtained under false pretenses. This can involve misrepresenting income, assets, or other financial information to qualify for a loan that they would not otherwise be eligible for. The straw buyer may not intend to live in the property and may not even know that they are part of a fraudulent scheme. In some cases, the property may be flipped to another buyer at a higher price, with the proceeds going to the fraudsters. Straw buyer loans are illegal and can result in serious consequences for all parties involved, including the straw buyer, the lender, and the seller.

| Characteristics | Values |

|---|---|

| Definition | A straw buyer loan is a type of mortgage fraud where a person (the straw buyer) obtains a mortgage for a property they do not intend to occupy or own. |

| Purpose | The primary purpose is often to inflate the property's value or to obtain a loan that the actual borrower could not qualify for on their own. |

| Participants | Typically involves a straw buyer, a lender, and sometimes a real estate agent or broker who facilitates the transaction. |

| Legal Implications | Straw buyer loans are illegal and considered a form of mortgage fraud. Participants can face severe legal consequences, including fines and imprisonment. |

| Detection | Red flags include a buyer with a poor credit history, a property that is overvalued, and a buyer who does not intend to live in the property. |

| Prevention | Lenders can prevent straw buyer loans by thoroughly vetting borrowers, verifying income and employment, and ensuring the property's value is accurate. |

| Impact on Lenders | Lenders may suffer financial losses if the straw buyer defaults on the loan, and it can damage their reputation. |

| Impact on Housing Market | Straw buyer loans can artificially inflate property values, leading to a housing bubble and making it difficult for genuine buyers to enter the market. |

| Historical Examples | Notable cases include the mortgage fraud schemes that contributed to the 2008 financial crisis. |

| Current Trends | With advancements in technology, straw buyer schemes have become more sophisticated, making detection and prevention more challenging. |

| Regulatory Measures | Governments and financial institutions have implemented stricter regulations and oversight to combat mortgage fraud. |

| Consumer Education | Educating consumers about the risks and consequences of participating in straw buyer schemes is crucial for prevention. |

Explore related products

What You'll Learn

- Definition: A straw buyer loan is a type of mortgage fraud where a person buys a property on behalf of another

- Purpose: The main purpose is to conceal the true identity of the buyer, often to secure a loan

- Process: The straw buyer applies for the loan, and the lender disburses funds, unaware of the deception

- Legal Implications: Straw buyer loans are illegal and can result in severe legal consequences for all parties involved

- Prevention: Lenders can prevent such fraud by conducting thorough background checks and verifying the buyer's identity

![]()

Definition: A straw buyer loan is a type of mortgage fraud where a person buys a property on behalf of another

A straw buyer loan is a sophisticated form of mortgage fraud that involves a third party purchasing a property on behalf of another individual or entity. This type of fraud is often used to circumvent lending regulations, hide the true identity of the borrower, or facilitate the laundering of illicit funds. The straw buyer, who may be a willing participant or an unwitting accomplice, typically has a better credit history or financial profile than the actual borrower, making it easier to secure a loan.

The process of obtaining a straw buyer loan usually involves the following steps: First, the fraudster identifies a suitable property and recruits a straw buyer. The straw buyer then applies for a mortgage, using their own financial information and credit history. Once the loan is approved, the straw buyer purchases the property and takes out a mortgage in their name. The fraudster then takes control of the property, making payments on the mortgage or renting it out to generate income.

Straw buyer loans can have serious consequences for all parties involved. The straw buyer may face legal repercussions, including criminal charges and financial penalties, if they are found to have knowingly participated in the fraud. The lender may suffer financial losses if the loan goes into default or if the property is sold for less than the outstanding mortgage balance. The true borrower may also face legal consequences, as well as damage to their credit history and financial reputation.

To avoid falling victim to straw buyer loan fraud, it is essential for lenders to conduct thorough due diligence on all mortgage applications. This includes verifying the identity and financial information of the borrower, as well as monitoring the property for signs of fraud, such as unusual payment patterns or unauthorized changes to the property. Borrowers should also be cautious when considering a straw buyer loan, as it may seem like an easy way to obtain financing but can ultimately lead to significant legal and financial consequences.

Exclusive Access: The Insider's Guide to Member-Only Communities

You may want to see also

Explore related products

![]()

Purpose: The main purpose is to conceal the true identity of the buyer, often to secure a loan

The primary objective of a straw buyer loan is to disguise the true identity of the purchaser, typically to facilitate the acquisition of a loan. This practice is often employed when the actual buyer may not qualify for a loan due to credit issues, income limitations, or other financial constraints. By using a straw buyer, who is essentially a stand-in for the real purchaser, the transaction can be structured in a way that meets the lender's criteria.

One common scenario involves a family member or friend acting as the straw buyer. For instance, if a parent wants to help their child buy a home but the child doesn't have the necessary credit history or income, the parent might act as the straw buyer. They would apply for the loan in their own name, using their financial information to secure the mortgage. Once the loan is approved and the property is purchased, the parent might then transfer the property to the child, either immediately or after a certain period.

Another example could be in the realm of business. A company might use a straw buyer to acquire a property or asset that they cannot purchase directly due to legal or financial restrictions. In this case, the straw buyer would be an individual or entity that is not directly affiliated with the company but is acting on their behalf. The straw buyer would secure the loan and purchase the property, which would then be transferred to the company through a lease or sale.

It's important to note that while the use of a straw buyer can be a creative solution to financing challenges, it also carries significant risks. If the straw buyer defaults on the loan, the lender can pursue legal action against them, which could lead to financial ruin. Additionally, if the true identity of the buyer is discovered, the lender might consider the loan to be in default, potentially leading to foreclosure or other legal consequences.

In conclusion, a straw buyer loan is a complex financial arrangement that involves using a third party to conceal the true identity of the buyer. While it can be a useful strategy in certain situations, it's crucial to understand the risks and legal implications involved. Anyone considering a straw buyer loan should consult with a financial advisor or attorney to ensure they are making an informed decision.

Understanding Financial Aid: Grants vs. Loans Explained

You may want to see also

Explore related products

![]()

Process: The straw buyer applies for the loan, and the lender disburses funds, unaware of the deception

The process of obtaining a straw buyer loan involves a series of deliberate steps designed to deceive the lender. It begins with the straw buyer, who may be an individual or a company, applying for a loan under false pretenses. This application is often supported by fraudulent documentation, such as inflated income statements, fake employment records, or misleading credit reports. The goal is to present a financial picture that is more favorable than the reality, thereby increasing the likelihood of loan approval.

Once the application is submitted, the lender conducts its due diligence, which may include verifying the information provided, checking credit scores, and assessing the collateral offered, if any. However, due to the sophistication of the deception, the lender may not detect the fraud and proceeds to disburse the funds. This disbursement is typically done without the lender's knowledge of the true purpose of the loan or the identity of the actual borrower.

The funds are then used by the actual borrower, who may be someone other than the straw buyer, for purposes that may not align with the loan's intended use. This could range from personal expenses to business ventures, all while the straw buyer is responsible for repaying the loan. The actual borrower may make payments to the straw buyer to cover the loan repayments, or they may default, leaving the straw buyer liable for the debt.

The consequences of participating in a straw buyer loan can be severe for all parties involved. If the deception is discovered, the lender may take legal action against the straw buyer and the actual borrower, leading to potential criminal charges, fines, and damage to credit scores. Additionally, the lender may attempt to recover the funds disbursed, which could result in financial hardship for the straw buyer and the actual borrower.

To avoid such schemes, lenders must remain vigilant and employ robust verification processes. This includes cross-checking information with multiple sources, conducting thorough background checks, and ensuring that the loan's purpose aligns with the borrower's financial profile. Borrowers, on the other hand, should be cautious about engaging in any transactions that involve misrepresenting their financial situation or using someone else's identity to obtain credit.

Unlocking Opportunities: Your Guide to Becoming an Arizona Loan Signing Agent

You may want to see also

![]()

Legal Implications: Straw buyer loans are illegal and can result in severe legal consequences for all parties involved

Straw buyer loans are a form of mortgage fraud that involves a person (the straw buyer) purchasing a property on behalf of another individual or entity (the true buyer) who is unable to secure a loan themselves. This illegal practice can have severe legal consequences for all parties involved.

One of the primary legal implications of straw buyer loans is the potential for criminal charges. Mortgage fraud is a serious crime, and those involved in straw buyer schemes can face charges such as conspiracy to commit fraud, wire fraud, and mail fraud. Convictions can result in significant fines and even imprisonment.

In addition to criminal charges, straw buyers and the true buyers they are representing can also face civil penalties. Lenders may sue for breach of contract, misrepresentation, or fraud, seeking to recover any losses incurred as a result of the illegal loan. This can include the full amount of the loan, as well as legal fees and other associated costs.

Furthermore, straw buyer loans can have a negative impact on the credit scores of both the straw buyer and the true buyer. If the loan goes into default, it will be reported on both individuals' credit reports, making it more difficult for them to secure future loans or credit.

It is also important to note that straw buyer loans can have broader implications for the housing market and the economy as a whole. By artificially inflating property values and enabling unqualified buyers to purchase homes, straw buyer schemes can contribute to housing bubbles and market instability.

In conclusion, straw buyer loans are illegal and can result in severe legal consequences for all parties involved. These consequences can include criminal charges, civil penalties, and damage to credit scores, as well as broader implications for the housing market and the economy.

Unlocking Opportunities: Your Guide to Becoming a Loan Signing Notary

You may want to see also

![]()

Prevention: Lenders can prevent such fraud by conducting thorough background checks and verifying the buyer's identity

Lenders play a crucial role in preventing straw buyer loan fraud. One of the primary methods to mitigate this risk is by conducting thorough background checks on all parties involved in the loan application process. This includes verifying the identity of the buyer, as well as scrutinizing their financial history, employment records, and creditworthiness. By doing so, lenders can identify potential red flags that may indicate fraudulent activity, such as inconsistencies in personal information or a history of financial mismanagement.

In addition to background checks, lenders should also implement robust identity verification processes. This can involve using advanced technologies such as biometric authentication, facial recognition, or document verification tools to ensure that the individual presenting themselves as the buyer is indeed who they claim to be. Furthermore, lenders should consider cross-referencing the buyer's information with external databases and watchlists to detect any potential links to criminal activity or fraud.

Another important preventive measure is to educate borrowers and other stakeholders about the risks and consequences of straw buyer loan fraud. By raising awareness about the warning signs and providing guidance on how to report suspicious activity, lenders can empower individuals to take an active role in protecting themselves and others from fraud. This can be achieved through targeted outreach programs, online resources, and training sessions for real estate professionals and financial advisors.

Moreover, lenders should establish clear policies and procedures for handling suspected cases of straw buyer loan fraud. This includes having a dedicated team or department responsible for investigating and addressing potential fraud incidents, as well as implementing a system for reporting and tracking such cases. By taking a proactive and systematic approach to fraud prevention, lenders can not only protect their own interests but also contribute to the overall integrity of the financial system.

In conclusion, preventing straw buyer loan fraud requires a multifaceted approach that involves thorough background checks, robust identity verification, education and awareness initiatives, and clear policies and procedures for handling suspected fraud cases. By implementing these measures, lenders can significantly reduce the risk of fraud and ensure that their lending practices are both secure and compliant with regulatory requirements.

Understanding Cash App Borrow Limit Increases: A Comprehensive Guide

You may want to see also

Frequently asked questions

A straw buyer loan is a type of mortgage fraud where a person, known as the straw buyer, purchases a property using a loan obtained under false pretenses. The straw buyer typically has no intention of living in the property and is often paid for their role in the scheme.

In a straw buyer loan, the fraudster finds a willing participant (the straw buyer) to purchase a property. The straw buyer applies for a mortgage using false information, such as inflated income or assets. Once the loan is approved, the fraudster uses the loan proceeds for their own benefit, while the straw buyer may receive a fee for their involvement.

Straw buyer loans can have severe consequences for all parties involved. The lender may suffer significant financial losses if the loan defaults. The straw buyer may face legal repercussions, including criminal charges for mortgage fraud. Additionally, the property may be foreclosed, leading to further financial losses for the lender and potential damage to the community.

Preventing straw buyer loans requires vigilance from lenders, real estate professionals, and other parties involved in the mortgage process. Lenders should thoroughly verify the borrower's income, assets, and credit history. Real estate agents and brokers should be aware of the warning signs of mortgage fraud, such as a buyer who is unwilling to provide documentation or who seems overly eager to close the deal.

Some red flags that may indicate a straw buyer loan include:

- The buyer is unwilling to provide documentation or verify their income and assets.

- The buyer seems overly eager to close the deal and may be pressuring the lender or real estate agent to rush the process.

- The buyer is purchasing a property that is significantly more expensive than their income would suggest they can afford.

- The buyer is using a third party to facilitate the purchase, such as a friend or family member.

- The property is being purchased in a high-risk area or is in poor condition.