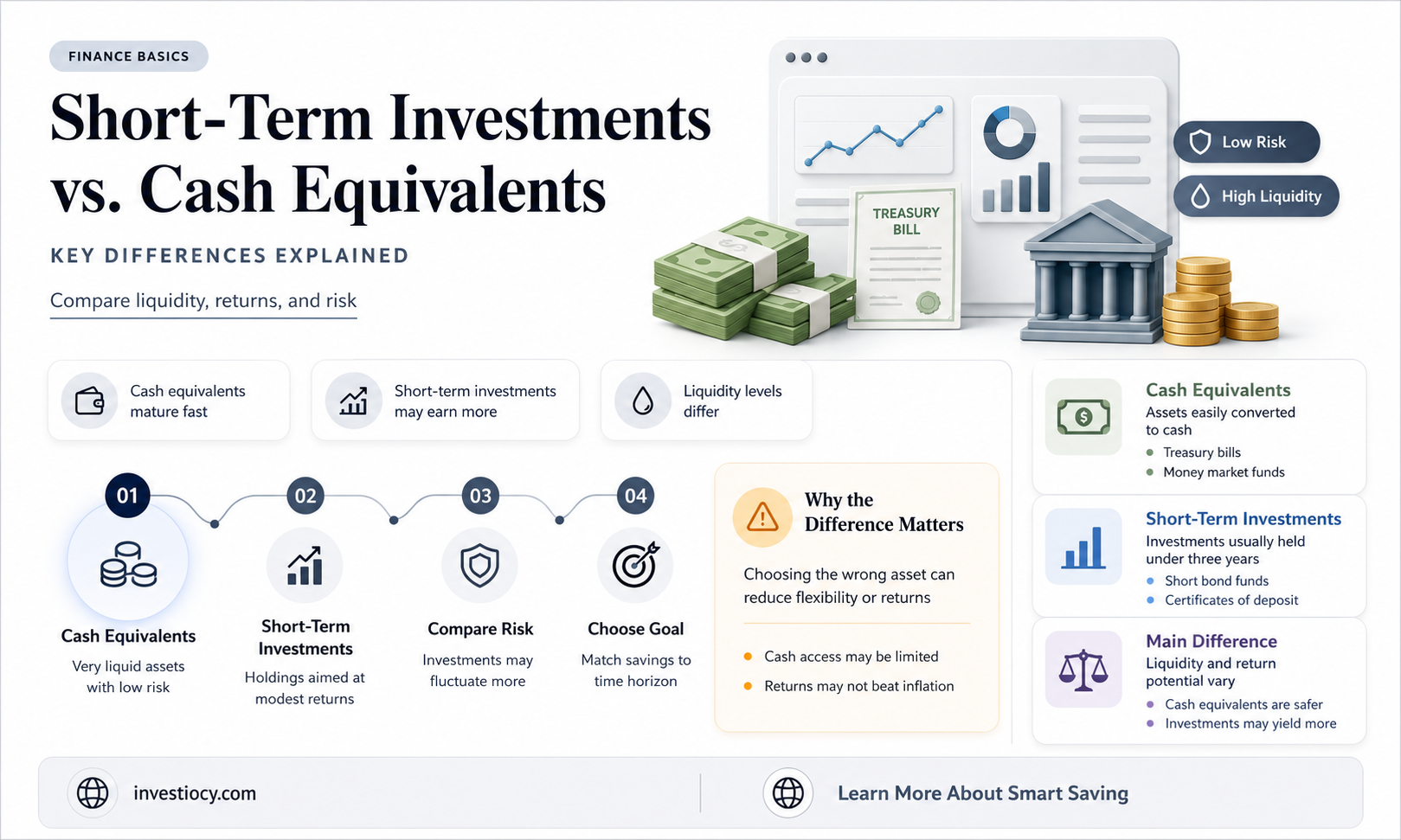

Short-term investments and cash equivalents are often confused due to their similar nature, but they have distinct differences. Cash equivalents are highly liquid assets that can be easily converted to cash within a short period, typically three months or less. Examples include savings accounts, money market funds, and treasury bills. On the other hand, short-term investments are assets that can be converted to cash within one year or less, but they may not be as liquid as cash equivalents. These can include short-term bonds, certificates of deposit, and some types of mutual funds. While both cash equivalents and short-term investments offer relatively low risk and high liquidity compared to long-term investments, understanding their differences is crucial for effective financial management and planning.

Explore related products

$8.73 $19.99

What You'll Learn

![]()

Definition of Cash Equivalents

Cash equivalents are assets that are readily convertible into cash within a short period, typically three months or less. These assets are considered to be as liquid as cash itself and are often used by companies to meet their short-term financial obligations. Common examples of cash equivalents include treasury bills, certificates of deposit, commercial paper, and money market funds.

The key characteristic of cash equivalents is their high liquidity and low risk. They are designed to provide a safe and stable place for investors to park their money for short periods while still earning some interest. Cash equivalents are often used by companies to manage their cash flow and ensure they have enough funds on hand to meet their day-to-day expenses.

One important aspect of cash equivalents is that they should not be confused with other types of short-term investments. While all cash equivalents are short-term investments, not all short-term investments are cash equivalents. For example, stocks and bonds can be considered short-term investments, but they are not cash equivalents because they are not as easily convertible into cash.

Another key point to note is that cash equivalents are not the same as cash reserves. Cash reserves refer to the actual cash that a company holds in its bank accounts, while cash equivalents are assets that can be quickly converted into cash. Companies often hold a combination of cash reserves and cash equivalents to ensure they have enough liquidity to meet their financial needs.

In summary, cash equivalents are highly liquid, low-risk assets that can be quickly converted into cash. They play an important role in helping companies manage their cash flow and meet their short-term financial obligations. While they are a type of short-term investment, they should not be confused with other types of investments that are not as easily convertible into cash.

Smart Investing: Balancing Short-Term Gains and Long-Term Growth

You may want to see also

Explore related products

$6.99 $9.33

![]()

Types of Short-Term Investments

Short-term investments are financial instruments that can be converted into cash within a year or less. They are often used by individuals and businesses to park their money temporarily while earning some interest or returns. One type of short-term investment is a savings account, which is a deposit account held at a bank or other financial institution that pays interest on the deposited funds. Another type is a money market fund, which is a mutual fund that invests in high-quality, short-term debt securities and pays dividends to its shareholders.

Certificates of deposit (CDs) are another popular short-term investment option. They are time deposits offered by banks and credit unions that pay a fixed rate of interest for a specified period, typically ranging from a few months to a year. Treasury bills, or T-bills, are short-term government securities that are issued by the U.S. Treasury Department and have maturities of less than a year. They are considered to be one of the safest investments available, as they are backed by the full faith and credit of the U.S. government.

Commercial paper is a type of short-term debt instrument issued by large corporations to finance their operations. It typically has a maturity of less than nine months and is sold at a discount to its face value. Finally, repurchase agreements, or repos, are short-term collateralized loans that are used by banks and other financial institutions to manage their liquidity. They involve the sale of securities with an agreement to repurchase them at a later date, usually within a few days or weeks.

When choosing a short-term investment, it's important to consider factors such as the investment's liquidity, risk, and potential returns. Savings accounts and money market funds are generally considered to be low-risk options, but they may not offer the highest returns. CDs and T-bills offer slightly higher returns, but they may have penalties for early withdrawal. Commercial paper and repos are higher-risk options that offer higher returns, but they are typically only available to institutional investors.

In conclusion, short-term investments can be a useful tool for managing cash flow and earning some interest on idle funds. By understanding the different types of short-term investments available and their respective risks and returns, investors can make informed decisions about where to park their money for the short term.

Is Inventory a Short-Term Investment? Understanding Its Impact on Financial Health

You may want to see also

Explore related products

![]()

Liquidity and Maturity

Short-term investments are typically those with a maturity of less than one year. To qualify as cash equivalents, these investments must not only be highly liquid but also have a maturity that aligns with the company's short-term financial needs. This ensures that the funds can be readily accessed to meet immediate obligations, such as paying bills or covering unexpected expenses.

When assessing liquidity, it's essential to consider the market depth and the bid-ask spread of the investment. A deep market with a narrow bid-ask spread indicates high liquidity, as it suggests that there are many buyers and sellers, and the price is stable. Examples of highly liquid short-term investments include treasury bills, commercial paper, and money market funds.

Maturity is equally important, as investments with longer maturities may not be suitable for companies with immediate cash flow needs. For instance, a six-month treasury bill may be considered a cash equivalent for a company with a three-month cash reserve requirement, but a two-year bond would not be appropriate.

In conclusion, liquidity and maturity are key determinants of whether short-term investments can be classified as cash equivalents. Companies must carefully evaluate these factors to ensure that their investments are both easily convertible to cash and aligned with their short-term financial obligations. By doing so, they can maintain a strong liquidity position and effectively manage their working capital.

Debunking Myths: Not All Long-Term Investments Guarantee Returns

You may want to see also

![]()

Risk and Return

Short-term investments are often evaluated based on their risk and return profiles. Risk refers to the potential loss of principal or the variability of returns, while return is the gain or loss generated by an investment over a specific period. In the context of short-term investments, understanding the trade-off between risk and return is crucial for making informed decisions.

One common short-term investment is the money market fund, which typically offers a low risk of principal loss and a modest return. These funds invest in high-quality, liquid securities such as U.S. Treasury bills, commercial paper, and certificates of deposit. While they are not insured by the FDIC, they are considered to be among the safest types of investments due to their diversification and the creditworthiness of the issuers.

Another option is the high-yield savings account, which offers a higher return than a traditional savings account but may come with a slightly higher risk. These accounts are insured by the FDIC up to $250,000, providing a level of security for investors. However, they may require a minimum balance or impose withdrawal restrictions, which can impact liquidity.

Short-term bonds, such as municipal bonds or corporate bonds with maturities of less than five years, can also be considered as short-term investments. These bonds offer a higher return than money market funds but come with a higher risk of default. Investors should carefully evaluate the creditworthiness of the issuer and the specific terms of the bond before investing.

Finally, investors may consider short-term stock market investments, such as exchange-traded funds (ETFs) or individual stocks. These investments offer the potential for higher returns but come with a significantly higher risk of principal loss. Short-term stock market investments are more volatile and can be affected by market fluctuations, economic conditions, and company-specific events.

In conclusion, short-term investments offer a range of risk and return profiles, and investors should carefully consider their financial goals, risk tolerance, and liquidity needs before selecting an investment. By understanding the trade-off between risk and return, investors can make informed decisions that align with their overall financial strategy.

Exploring Short-Term Investments: A Guide to Financial Flexibility

You may want to see also

![]()

Accounting Treatment

In accounting, the treatment of short-term investments as cash equivalents is a critical decision that impacts financial reporting and analysis. Cash equivalents are typically defined as investments that are readily convertible to cash within three months or less, and they are recorded at their market value on the balance sheet. Short-term investments, on the other hand, are those that are expected to be held for a longer period, usually between three and twelve months. The key distinction lies in the liquidity and maturity of these investments.

When short-term investments are classified as cash equivalents, they are grouped together with cash and other highly liquid assets in the current assets section of the balance sheet. This classification can affect the company's liquidity ratios, such as the current ratio and quick ratio, making them appear more favorable. However, it is essential to note that not all short-term investments qualify as cash equivalents. Investments that are not readily convertible to cash or that have a maturity of more than three months should be classified separately.

The accounting treatment for cash equivalents is straightforward; they are recorded at their market value, and any changes in value are reflected in the income statement as gains or losses. In contrast, short-term investments that are not cash equivalents are typically recorded at their amortized cost, with any changes in market value reported as unrealized gains or losses in other comprehensive income.

One unique aspect of accounting for short-term investments as cash equivalents is the need for continuous monitoring and evaluation. Companies must regularly assess whether their investments still meet the criteria for cash equivalents, considering factors such as market conditions, credit risk, and maturity dates. If an investment no longer qualifies as a cash equivalent, it must be reclassified, and the financial statements must be adjusted accordingly.

In practice, the decision to classify short-term investments as cash equivalents can have significant implications for financial reporting and decision-making. For example, a company that holds a large portfolio of short-term investments may choose to classify them as cash equivalents to improve its liquidity ratios and enhance its financial position. However, this decision must be carefully considered, as it may not accurately reflect the true nature of the investments.

In conclusion, the accounting treatment of short-term investments as cash equivalents is a complex and nuanced topic that requires careful consideration and ongoing evaluation. By understanding the criteria for cash equivalents and the implications of their classification, companies can ensure that their financial statements accurately reflect their liquidity and financial position.

Smart Strategies: Examples of Short-Term Investments for Quick Returns

You may want to see also

Frequently asked questions

Short-term investments are not typically considered cash equivalents. Cash equivalents are assets that are readily convertible to cash within three months or less, such as savings accounts, money market funds, and treasury bills. Short-term investments, while liquid, usually have a slightly longer maturity period and may not be as easily convertible to cash.

Examples of short-term investments include certificates of deposit (CDs), short-term bonds, commercial paper, and short-term mutual funds. These investments typically have maturities ranging from a few months to a few years.

A company might choose to invest in short-term investments to earn a higher return on its idle funds compared to the lower interest rates offered by cash equivalents. Short-term investments can provide a balance between liquidity and higher yields, allowing companies to make the most of their available cash.

Short-term investments carry some risks, including interest rate risk, credit risk, and market risk. Interest rate risk refers to the possibility that interest rates will rise, reducing the value of the investment. Credit risk involves the potential default of the issuer, while market risk is related to fluctuations in the overall market that can affect the investment's value.

Short-term investments are typically classified as current assets on a company's balance sheet. They are valued at their fair market value, and any changes in value are recorded in the income statement as gains or losses. The cash flows from short-term investments are also reflected in the cash flow statement, under the investing activities section.