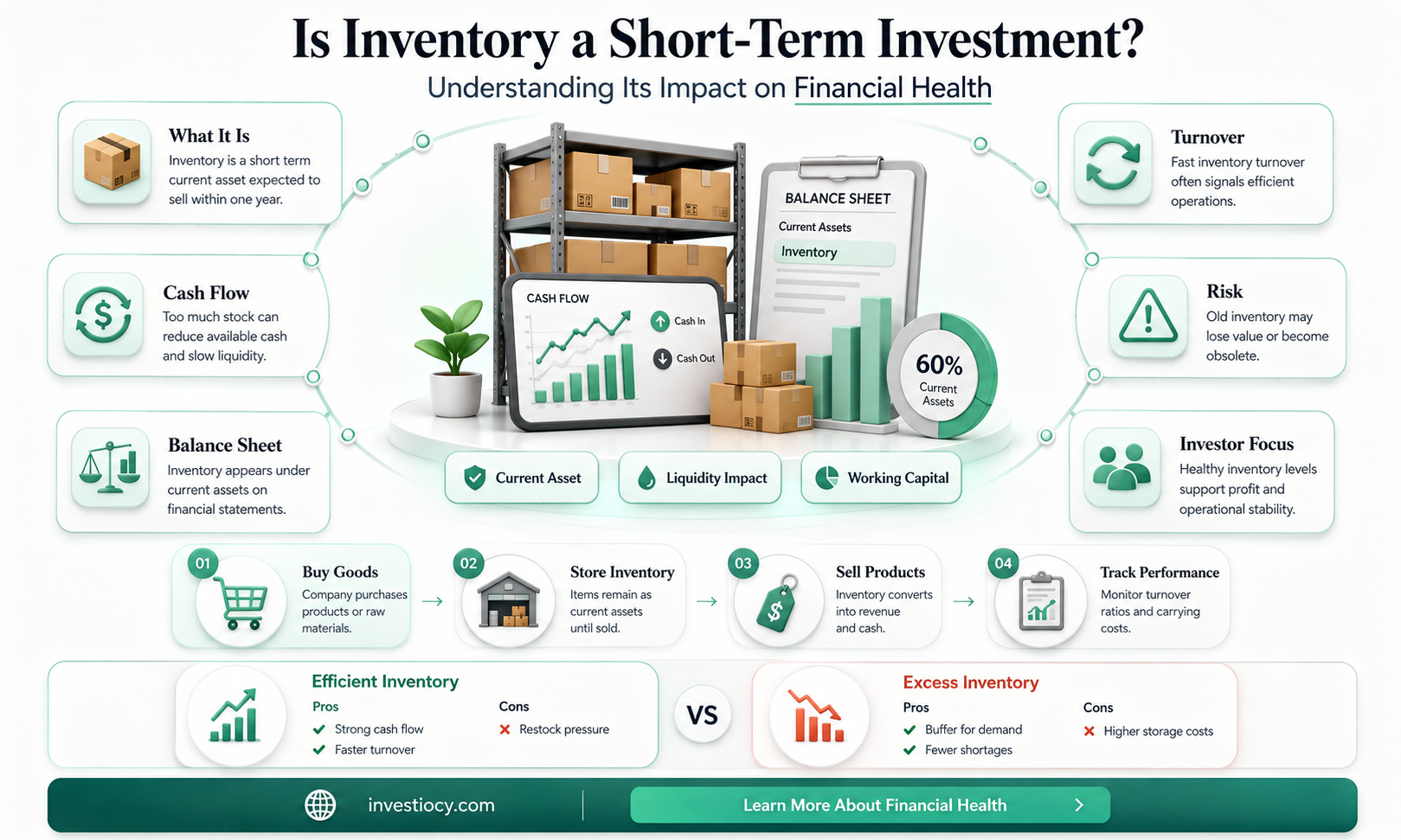

Inventory is a crucial component of a company's assets, representing goods and materials held for sale in the ordinary course of business. When discussing whether inventory is a short-term investment, it's essential to consider the nature of the inventory and the company's operational cycle. Short-term investments are typically liquid assets that can be converted into cash within a year or less. Inventory, by its nature, is intended to be sold and converted into cash as part of a company's regular operations. However, the classification of inventory as a short-term investment depends on factors such as the company's inventory turnover rate, the type of industry, and the market conditions for the goods held. In general, inventory is considered a short-term investment because it is expected to be sold and replaced frequently, aligning with the company's short-term financial goals and operational needs.

Explore related products

What You'll Learn

- Definition of Inventory: Inventory refers to goods and materials held by a business for resale or production

- Short-Term Investment: Investments expected to be converted to cash or used within one year are considered short-term

- Inventory Turnover: Measures how often inventory is sold and replaced within a given period, indicating liquidity

- Holding Costs: Costs associated with storing and maintaining inventory, such as warehousing and insurance

- Opportunity Costs: Potential returns missed by holding inventory instead of investing in other assets or opportunities

![]()

Definition of Inventory: Inventory refers to goods and materials held by a business for resale or production

Inventory, in the context of business and accounting, refers to the goods and materials that a company holds for the purpose of resale or production. This can include raw materials, work-in-progress, and finished goods. The classification of inventory as a short-term investment is based on its liquidity and the expectation that it will be converted into cash within one year or within the company's normal operating cycle, whichever is longer.

The primary reason inventory is considered a short-term investment is due to its role in the production and sales cycle of a business. Companies typically aim to turn over their inventory quickly to generate revenue and cover the costs associated with holding inventory, such as storage, insurance, and potential obsolescence. Efficient inventory management is crucial for maintaining a healthy cash flow and ensuring that the business can meet customer demand without incurring excessive holding costs.

In accounting terms, inventory is recorded as an asset on the balance sheet and is valued at the lower of cost or market price. This valuation method ensures that the inventory is not overstated on the financial statements, reflecting the conservative principle of accounting. When inventory is sold, the cost of goods sold (COGS) is recognized on the income statement, reducing the inventory balance and matching the revenue generated from the sale.

From a financial analysis perspective, inventory turnover is a key metric used to assess the efficiency of a company's inventory management. A high inventory turnover ratio indicates that the company is effectively converting its inventory into sales, while a low ratio may suggest issues with inventory management, such as overstocking or slow-moving products. Investors and analysts often examine inventory turnover as part of their evaluation of a company's operational efficiency and financial health.

In conclusion, inventory is a critical component of a business's operations and financial strategy. Its classification as a short-term investment reflects its role in the production and sales cycle, as well as its liquidity and potential for quick conversion into cash. Effective inventory management is essential for maintaining a healthy cash flow, minimizing holding costs, and ensuring that the business can meet customer demand efficiently.

Unlocking Profits: A Guide to Short-Term Rental Investments

You may want to see also

Explore related products

![]()

Short-Term Investment: Investments expected to be converted to cash or used within one year are considered short-term

Inventory is indeed classified as a short-term investment, primarily because it is expected to be converted into cash or used within a year. This classification is crucial for businesses as it affects how inventory is managed and reported on financial statements. Short-term investments are typically more liquid than long-term investments, meaning they can be easily converted to cash without significant loss of value. Inventory fits this description as it is a current asset that companies aim to sell or use in the near future.

The management of inventory as a short-term investment involves strategies to optimize its turnover and minimize holding costs. Companies must balance having enough inventory to meet customer demand with the costs associated with storing and maintaining that inventory. Effective inventory management can lead to improved cash flow and profitability, as it ensures that capital is not tied up in unsold goods for extended periods.

From an accounting perspective, inventory is reported on the balance sheet under current assets. Its value is determined by the lower of cost or net realizable value, which is the estimated selling price minus any costs to complete the sale. This conservative approach ensures that the financial statements reflect a realistic view of the inventory's value.

In conclusion, inventory is a short-term investment because it is intended to be converted to cash or used within a year. This classification has significant implications for how businesses manage and report their inventory, emphasizing the importance of efficient inventory turnover and accurate financial reporting.

Exploring Short-Term Investments: A Guide to Financial Flexibility

You may want to see also

Explore related products

![]()

Inventory Turnover: Measures how often inventory is sold and replaced within a given period, indicating liquidity

Inventory turnover is a critical metric in assessing the liquidity of a company's inventory. It measures the number of times inventory is sold and replaced within a given period, typically a year. A higher inventory turnover indicates that a company is efficiently managing its inventory, selling products quickly, and maintaining a steady flow of goods. This is particularly important for businesses that deal with perishable items or products with a short shelf life.

To calculate inventory turnover, you divide the cost of goods sold (COGS) by the average inventory value. The formula is: Inventory Turnover = COGS / Average Inventory. For example, if a company's COGS is $500,000 and its average inventory value is $100,000, the inventory turnover would be 5. This means the company sells and replaces its inventory five times a year.

A high inventory turnover can be beneficial for several reasons. Firstly, it reduces the risk of inventory obsolescence, which is when products become outdated or unsellable. Secondly, it minimizes the costs associated with holding inventory, such as storage, insurance, and taxes. Thirdly, it improves cash flow by converting inventory into sales more quickly.

However, there are also potential downsides to a high inventory turnover. If a company is selling and replacing inventory too quickly, it may be indicative of overstocking or poor demand forecasting. This can lead to excess inventory costs and potential write-offs. Additionally, a very high turnover rate may strain a company's supply chain and logistics capabilities, potentially leading to stockouts or delays in fulfilling orders.

In conclusion, inventory turnover is a valuable metric for evaluating the efficiency and liquidity of a company's inventory management. While a higher turnover rate is generally desirable, it's important to balance this with effective demand forecasting and supply chain management to avoid potential pitfalls.

Smart Investing: Balancing Short-Term Gains and Long-Term Growth

You may want to see also

Explore related products

![]()

Holding Costs: Costs associated with storing and maintaining inventory, such as warehousing and insurance

Holding costs are a critical component of inventory management that can significantly impact a company's financial health. These costs include warehousing, insurance, and maintenance expenses, among others. Warehousing costs can be particularly high, especially for businesses that operate in urban areas where real estate is expensive. Insurance costs can also add up, particularly for companies that deal with high-value or perishable goods.

One way to reduce holding costs is to implement a just-in-time (JIT) inventory system. This approach involves ordering and receiving inventory only as needed, which can help to minimize storage and maintenance expenses. However, JIT systems can be complex to implement and may not be suitable for all businesses. Another strategy is to negotiate better rates with suppliers or to consolidate inventory in a single location to reduce storage costs.

It's also important to consider the opportunity costs of holding inventory. For example, if a company has a large amount of inventory tied up in storage, it may not have the funds available to invest in other areas of the business. Additionally, holding onto inventory for too long can lead to obsolescence, which can result in significant losses.

In conclusion, holding costs are a key consideration for businesses that manage inventory. By understanding these costs and implementing strategies to reduce them, companies can improve their financial performance and gain a competitive edge in the market.

Debunking Myths: Not All Long-Term Investments Guarantee Returns

You may want to see also

Explore related products

![]()

Opportunity Costs: Potential returns missed by holding inventory instead of investing in other assets or opportunities

Holding inventory ties up capital that could otherwise be invested in a variety of other assets or opportunities, each with its own potential return. This is the essence of opportunity cost—the value of the next best alternative forgone. For instance, a business might choose to hold $10,000 worth of inventory instead of investing that money in the stock market, which historically has provided an average annual return of around 10%. Over a year, this decision could result in a missed opportunity cost of $1,000, assuming the inventory does not appreciate in value or generate revenue equivalent to the investment returns.

The opportunity cost of holding inventory can be particularly significant for businesses with high inventory turnover rates, as the capital is continuously cycled through inventory rather than being available for other investments. Moreover, the cost is not just financial; it also includes the time and resources spent managing inventory, which could be allocated to other strategic activities.

To mitigate these opportunity costs, businesses can adopt strategies such as just-in-time inventory management, which minimizes the amount of inventory held at any given time, or dropshipping, where inventory is held by a third party and shipped directly to customers. These methods free up capital and reduce the administrative burden of inventory management, allowing businesses to explore other investment opportunities.

However, it's important to note that inventory can also serve as a buffer against market volatility and supply chain disruptions. In some cases, the strategic benefits of holding inventory may outweigh the opportunity costs, especially for businesses in industries with high demand variability or long lead times for restocking.

Ultimately, the decision to hold inventory versus investing in other assets depends on a thorough analysis of the business's financial situation, market conditions, and strategic objectives. By carefully considering the opportunity costs and benefits, businesses can make informed decisions that optimize their overall performance and profitability.

Unlocking Liquidity: A Guide to Short-Term Investments on the Balance Sheet

You may want to see also

Frequently asked questions

Inventory is typically not considered a short-term investment. It is an asset that a company holds with the intention of selling it in the future, but it is not usually classified as short-term because it may take longer than a year to sell.

Inventory is classified as a current asset on a balance sheet, which means it is expected to be converted into cash or used within one year. However, this classification can vary depending on the nature of the inventory and the company's accounting practices.

Examples of inventory that might be considered short-term investments include perishable goods, such as food or flowers, that have a limited shelf life and are expected to be sold quickly. Additionally, companies that sell seasonal products, such as winter clothing or holiday decorations, may consider these items short-term investments because they are only held for a short period of time before being sold.

Inventory management can have a significant impact on a company's financial performance. If a company holds too much inventory, it can tie up valuable resources and lead to increased storage and maintenance costs. On the other hand, if a company does not hold enough inventory, it may miss out on sales opportunities and lose customers. Effective inventory management involves balancing these factors to ensure that the company has the right amount of inventory to meet customer demand while minimizing costs.

Some strategies for managing inventory effectively include implementing a just-in-time (JIT) inventory system, which involves ordering inventory only when it is needed, and using inventory management software to track inventory levels and optimize ordering. Additionally, companies can use techniques such as ABC analysis to categorize inventory items based on their value and importance, and focus on managing the most critical items more closely.