A deed is a legal document that transfers ownership of property from one party to another, while a mortgage is a loan secured by the property. Although both documents are related to property ownership, they serve different purposes. A deed does not inherently show a mortgage, as it only indicates the transfer of ownership. However, if there is a mortgage on the property, it may be mentioned in the deed or recorded separately in public records. To determine if a deed shows a mortgage, one must carefully examine the document for any references to a mortgage or loan agreement.

Explore related products

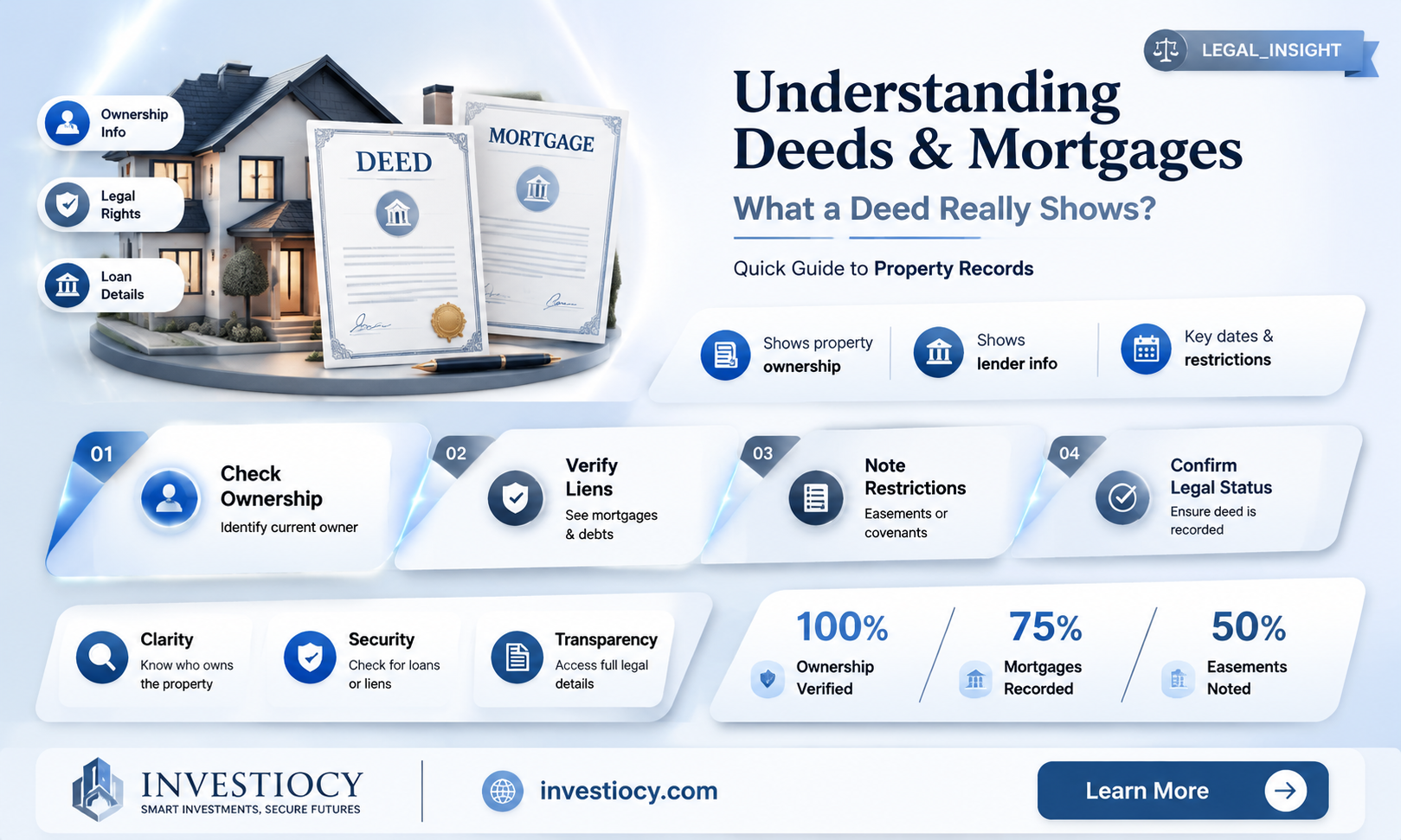

What You'll Learn

- Understanding Deeds: A deed is a legal document that transfers property ownership from one party to another

- Mortgage Information: A mortgage is a loan secured by real property, typically used to finance property purchases

- Deed vs. Mortgage: A deed shows ownership, while a mortgage shows a financial interest in the property

- Recording Mortgages: Mortgages are often recorded in public records to establish the lender's claim on the property

- Impact on Property Rights: A mortgage can affect the property rights conveyed by a deed, as the lender has a claim on the property

![]()

Understanding Deeds: A deed is a legal document that transfers property ownership from one party to another

A deed is a fundamental legal document in real estate transactions, serving as the instrument that officially transfers ownership of property from one party to another. This document is critical in ensuring that the transfer of property rights is legally recognized and recorded. Deeds typically contain essential information such as the names of the parties involved, a detailed description of the property, and the terms of the transfer. They must be signed by the party transferring the property and, in many jurisdictions, must also be notarized to verify the authenticity of the signatures.

Understanding the different types of deeds is crucial for anyone involved in real estate. The most common types include quitclaim deeds, warranty deeds, and grant deeds. Each type serves a specific purpose and offers different levels of protection and warranties to the parties involved. For instance, a quitclaim deed is often used when the property is being transferred without any warranties or guarantees regarding its title, while a warranty deed provides the recipient with assurances that the property is free from encumbrances and that the seller has the legal right to transfer ownership.

One important aspect to note is that while a deed transfers ownership, it does not necessarily show the existence of a mortgage on the property. A mortgage is a separate legal document that creates a lien on the property as security for a loan. Although a deed may mention the existence of a mortgage, it is not required to do so. To determine if there is a mortgage on a property, one would need to conduct a title search or review the property records maintained by the local government.

In some cases, a deed may include a clause that specifically states whether the property is subject to a mortgage. This can be useful for buyers who want to ensure that they are purchasing the property free and clear of any liens. However, even if the deed does not mention a mortgage, it is still possible that one exists. Therefore, it is always advisable for buyers to conduct thorough due diligence and review all relevant documents before completing a property purchase.

In conclusion, while a deed is an essential document for transferring property ownership, it does not inherently show the existence of a mortgage. To obtain a complete picture of the property's legal status, it is necessary to review additional documents and conduct a thorough title search. By understanding the role and limitations of a deed, buyers and sellers can navigate real estate transactions more effectively and ensure that their interests are protected.

Understanding Cosigner Rights in a Mortgage Agreement

You may want to see also

Explore related products

![]()

Mortgage Information: A mortgage is a loan secured by real property, typically used to finance property purchases

A mortgage is a legal agreement between a lender and a borrower, where the borrower pledges their property as collateral to secure the loan. This means that if the borrower fails to repay the loan, the lender has the right to take possession of the property. Mortgages are commonly used to finance the purchase of homes, but they can also be used for other types of real estate, such as commercial properties or land.

There are several types of mortgages, including fixed-rate mortgages, adjustable-rate mortgages, and government-backed mortgages. Fixed-rate mortgages have a set interest rate that does not change over the life of the loan, while adjustable-rate mortgages have an interest rate that can fluctuate based on market conditions. Government-backed mortgages, such as FHA loans and VA loans, are insured by the federal government and offer more favorable terms to borrowers who meet certain eligibility requirements.

When a property is purchased with a mortgage, the lender will typically require the borrower to sign a deed of trust or a mortgage document. This document serves as a lien on the property, giving the lender the right to take possession of the property if the borrower defaults on the loan. The deed of trust or mortgage document will also outline the terms of the loan, including the interest rate, payment schedule, and any penalties for late payments.

In some cases, a deed may show a mortgage, but this is not always the case. A deed is a legal document that transfers ownership of a property from one party to another, and it may not necessarily include information about any outstanding mortgages on the property. To determine if a property has a mortgage, it is important to review the property records or contact the lender directly.

If you are considering purchasing a property with a mortgage, it is important to carefully review the terms of the loan and ensure that you understand your obligations as a borrower. You should also consider factors such as your credit score, income, and debt-to-income ratio to determine if you can afford the monthly mortgage payments. By doing your research and seeking guidance from a qualified lender, you can make an informed decision about whether a mortgage is right for you.

Boosting Your Mortgage Amount: The Power of a Cosigner Revealed

You may want to see also

Explore related products

![]()

Deed vs. Mortgage: A deed shows ownership, while a mortgage shows a financial interest in the property

A deed and a mortgage are two distinct legal documents that serve different purposes in the realm of property ownership. While a deed is a written instrument that conveys ownership of real property from one party to another, a mortgage is a document that creates a lien on the property, giving a lender a financial interest in the property as security for a loan. Understanding the differences between these two documents is crucial for anyone involved in real estate transactions.

One key distinction between a deed and a mortgage is that a deed transfers the title of the property, while a mortgage does not. When a property owner executes a deed, they are essentially transferring their ownership rights to another party. This transfer is typically voluntary and is often part of a larger real estate transaction. On the other hand, a mortgage does not transfer ownership; instead, it creates a lien on the property, which means that the lender has a legal claim to the property if the borrower fails to repay the loan.

Another important difference is that a deed is a one-time transaction, while a mortgage is an ongoing financial arrangement. Once a deed is executed and recorded, the transfer of ownership is complete. In contrast, a mortgage is a long-term commitment that requires the borrower to make regular payments to the lender over a specified period. Failure to make these payments can result in foreclosure, which is a legal process that allows the lender to take possession of the property and sell it to recover the outstanding debt.

In summary, while both deeds and mortgages are essential components of real estate transactions, they serve different purposes and have distinct characteristics. Deeds transfer ownership of property, while mortgages create a financial interest in the property as security for a loan. Understanding these differences is crucial for anyone involved in buying, selling, or financing real estate.

Boosting Your Mortgage Approval Odds: The Power of a Cosigner

You may want to see also

Explore related products

$8.99

![]()

Recording Mortgages: Mortgages are often recorded in public records to establish the lender's claim on the property

Recording mortgages in public records is a critical step in the homeownership process. It serves as a legal mechanism to establish the lender's claim on the property, ensuring that their interest is formally recognized and protected. This process typically involves the filing of a mortgage deed or similar document with the appropriate government office, such as a county recorder or land registry.

The primary purpose of recording a mortgage is to provide constructive notice to third parties of the lender's lien on the property. This means that anyone who subsequently acquires an interest in the property, whether through purchase, inheritance, or other means, is deemed to have knowledge of the existing mortgage and takes their interest subject to it. This helps to prevent disputes over property ownership and ensures that the lender's rights are maintained even if the borrower defaults on their loan obligations.

In addition to providing notice, recording a mortgage also helps to establish the priority of the lender's claim in the event of a foreclosure or other legal proceeding. By being the first to record their interest, the lender can ensure that they are paid before other creditors or claimants. This is particularly important in situations where multiple parties have competing interests in the property, such as when there are multiple mortgages or liens.

The process of recording a mortgage can vary depending on the jurisdiction, but it generally involves the preparation and filing of a mortgage deed or similar document. This document typically includes details such as the names of the borrower and lender, the property address, the loan amount, and the terms of the mortgage. Once filed, the document becomes a matter of public record and can be accessed by anyone who wishes to review it.

In conclusion, recording mortgages in public records is a crucial step in the homeownership process that helps to establish the lender's claim on the property and protect their interests. It provides constructive notice to third parties, helps to establish the priority of the lender's claim, and ensures that the lender's rights are maintained even if the borrower defaults on their loan obligations.

Explore related products

![Judge John Deed (Season 6) - 2-DVD Box Set ( War Crimes / Evidence of Harm ) ( Judge John Deed - Season Six ) [ NON-USA FORMAT, PAL, Reg.2 Import - Netherlands ]](https://m.media-amazon.com/images/I/61lAFSeddoL._AC_UY218_.jpg)

![]()

Impact on Property Rights: A mortgage can affect the property rights conveyed by a deed, as the lender has a claim on the property

A mortgage can significantly impact the property rights conveyed by a deed. When a property owner takes out a mortgage, they are essentially granting the lender a lien on the property. This lien gives the lender a legal claim to the property, which can affect the owner's ability to sell or transfer the property. The lender's claim is typically recorded on the property's title, which means that it is a matter of public record and can be seen by anyone who searches the property's title.

One of the key ways that a mortgage affects property rights is by limiting the owner's ability to sell the property. If the owner wants to sell the property, they must first pay off the mortgage or obtain the lender's permission to sell the property subject to the existing mortgage. This can make it difficult for the owner to sell the property quickly or at a good price, as they may need to wait for the lender to approve the sale or find a buyer who is willing to take on the existing mortgage.

Another way that a mortgage affects property rights is by giving the lender the right to foreclose on the property if the owner fails to make their mortgage payments. Foreclosure is a legal process that allows the lender to take possession of the property and sell it to recover the amount of the unpaid mortgage. This can result in the owner losing their property and any equity they have built up in it.

In addition to these specific impacts, a mortgage can also affect property rights more generally. For example, a mortgage may limit the owner's ability to make changes to the property or to use it for certain purposes. The lender may also have the right to inspect the property or to require the owner to maintain it in a certain way. These restrictions can limit the owner's ability to fully enjoy their property rights.

Overall, it is important for property owners to understand how a mortgage can affect their property rights. By being aware of these impacts, owners can make informed decisions about whether or not to take out a mortgage and can take steps to protect their property rights if they do decide to take out a mortgage.

Frequently asked questions

A deed typically does not show a mortgage. A deed is a legal document that transfers ownership of property from one party to another, while a mortgage is a loan document that gives a lender a lien on the property.

A deed usually contains the names of the buyer and seller, a description of the property, the date of the transfer, and any restrictions or covenants on the property. It may also include information about the purchase price and any warranties or representations made by the seller.

To find out if there is a mortgage on a property, you can check the county recorder's office or the local courthouse. They will have records of all mortgages and liens on properties in their jurisdiction. You can also hire a title company to do a title search for you.

A deed is a document that transfers ownership of property, while a mortgage is a loan document that gives a lender a lien on the property. A deed is typically signed by the buyer and seller, while a mortgage is signed by the borrower and lender.

Yes, a mortgage can be removed from a property. This is typically done when the borrower pays off the loan in full. The lender will then release the lien on the property, and the borrower will have clear title to the property.

![No Good Deed [Blu-ray] by Sony](https://m.media-amazon.com/images/I/510t2yYnI6L._AC_UY218_.jpg)

![Silat Warriors: Deed of Death [Blu-ray]](https://m.media-amazon.com/images/I/61C4Ii5mA7L._AC_UY218_.jpg)

![Judge John Deed - Season One - 2-DVD Set ( Rough Justice / Duty of Care / Appropriate Response / Hidden Agenda ) ( Judge John Deed - Season 1 ) [ NON-USA FORMAT, PAL, Reg.2 Import - Netherlands ]](https://m.media-amazon.com/images/I/61qM0cj3ZsL._AC_UY218_.jpg)

![No Good Deed (2013) [Blu-ray]](https://m.media-amazon.com/images/I/51DZZKVyiUL._AC_UY218_.jpg)

![No good deed [IT Import]](https://m.media-amazon.com/images/I/717FWgwCcYL._AC_UY218_.jpg)