Being a Certified Public Accountant (CPA) can significantly enhance one's credibility and financial acumen, which are crucial factors when dealing with loans. CPAs are trained professionals who have demonstrated expertise in accounting principles, financial analysis, and tax laws. This expertise can be particularly beneficial when applying for loans, as lenders often scrutinize an individual's financial history and literacy. A CPA's designation may signal to lenders that the borrower has a strong understanding of financial management and is likely to handle loan repayments responsibly. Furthermore, CPAs may have access to specialized financial products and services tailored to their profession, potentially offering more favorable loan terms. In summary, the skills and reputation associated with being a CPA can indeed be advantageous when navigating the loan application process.

Explore related products

What You'll Learn

- Creditworthiness: CPAs may be viewed as more creditworthy due to their financial expertise and stability

- Income Verification: Lenders may require CPAs to provide proof of income, which can be easily documented

- Financial Planning: CPAs are skilled in financial planning, which can help in managing loan repayments effectively

- Interest Rates: Some lenders offer lower interest rates to CPAs due to their perceived lower risk

- Loan Approval: The CPA designation might influence loan approval decisions, as it indicates a high level of financial knowledge

![]()

Creditworthiness: CPAs may be viewed as more creditworthy due to their financial expertise and stability

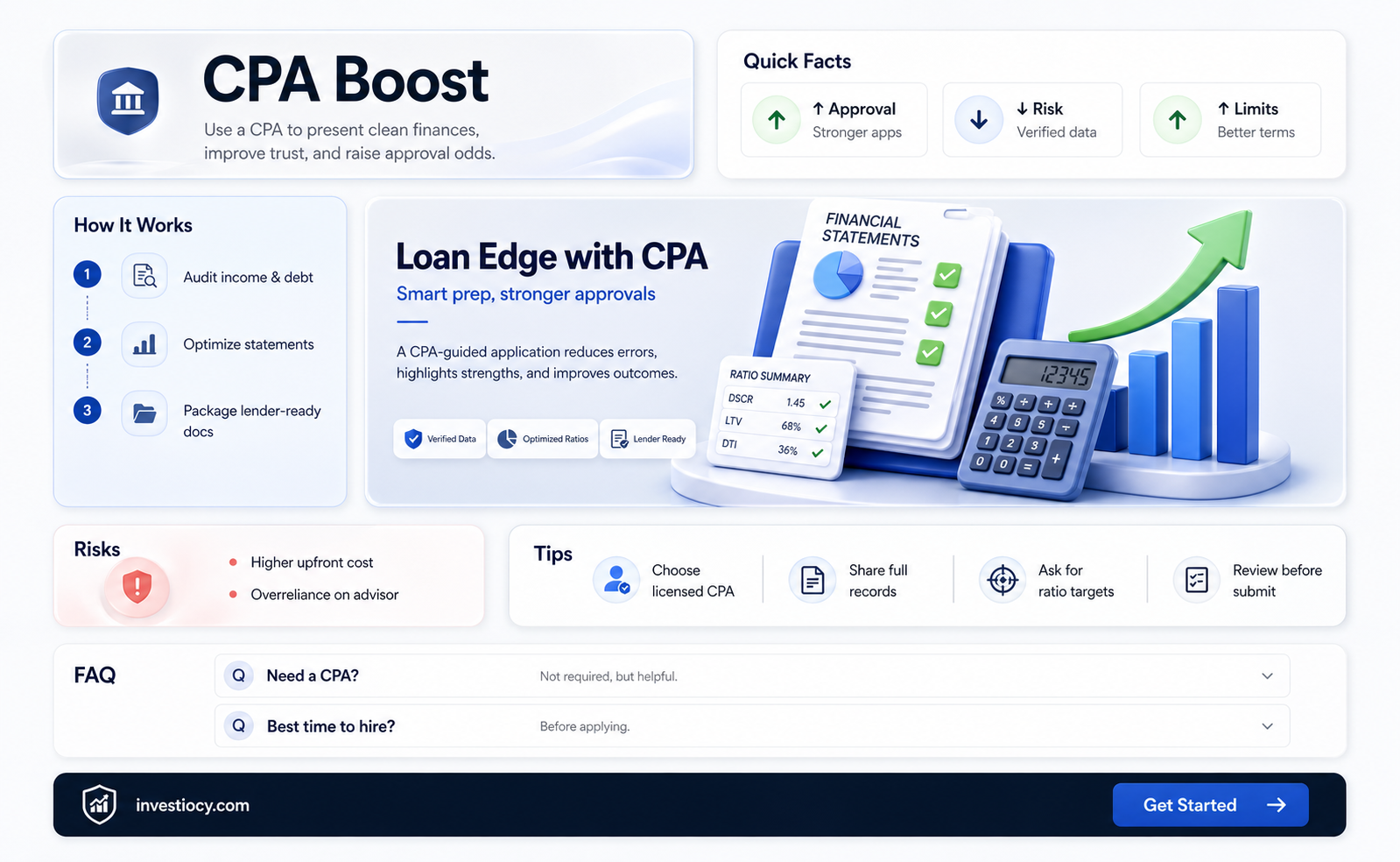

Lenders often assess creditworthiness based on a borrower's financial stability and expertise. Certified Public Accountants (CPAs) may be viewed as more creditworthy due to their demonstrated financial acumen and professional stability. This perception can be advantageous when applying for loans, as it may lead to more favorable terms and conditions.

One reason CPAs may be seen as more creditworthy is their rigorous training and certification process. Becoming a CPA requires passing a comprehensive exam that covers various aspects of accounting, auditing, and financial analysis. This demonstrates a high level of financial knowledge and expertise, which can be reassuring to lenders.

Additionally, CPAs are often employed in stable, well-paying jobs. Many work in corporate accounting, auditing firms, or as financial consultants, which are typically associated with steady income and low unemployment rates. This employment stability can contribute to a lender's confidence in a CPA's ability to repay a loan.

CPAs may also have access to financial resources and networks that can enhance their creditworthiness. They often work with financial institutions, investors, and other professionals in the finance industry, which can provide them with valuable insights and opportunities. This network can be beneficial when seeking loans, as it may open doors to alternative lending options or more competitive interest rates.

However, it's important to note that being a CPA does not automatically guarantee loan approval or favorable terms. Lenders still consider other factors, such as credit history, debt-to-income ratio, and collateral. Nonetheless, the financial expertise and stability associated with the CPA profession can certainly contribute positively to an individual's creditworthiness and overall loan application.

Explore related products

![]()

Income Verification: Lenders may require CPAs to provide proof of income, which can be easily documented

Lenders often require borrowers to provide proof of income as part of the loan application process. This is to ensure that the borrower has the financial means to repay the loan. For Certified Public Accountants (CPAs), this requirement can be easily met due to their profession. CPAs have access to detailed financial records and are trained to analyze and verify income statements. This makes them well-equipped to provide the necessary documentation to lenders.

One of the main advantages of being a CPA when applying for a loan is the ability to provide accurate and reliable financial information. CPAs are held to high ethical standards and are required to maintain confidentiality and integrity in their work. This means that lenders can trust the financial documents provided by a CPA, knowing that they have been prepared by a qualified professional.

In addition, CPAs are familiar with the specific financial documentation that lenders require. They can quickly and efficiently gather the necessary information, such as tax returns, pay stubs, and bank statements, and present it in a format that is acceptable to lenders. This can help to speed up the loan application process and increase the likelihood of approval.

Furthermore, CPAs are skilled at analyzing financial data and identifying potential issues that may affect a borrower's ability to repay a loan. By reviewing their own financial statements, CPAs can identify areas where they may need to improve their financial situation before applying for a loan. This can help to prevent potential loan denials and improve the overall financial health of the borrower.

In conclusion, being a CPA can be a significant advantage when applying for a loan. CPAs have the knowledge, skills, and resources to provide accurate and reliable financial information to lenders, which can help to speed up the loan application process and increase the likelihood of approval. Additionally, CPAs are well-equipped to identify and address potential financial issues that may affect their ability to repay a loan, ensuring a more secure financial future.

Explore related products

![]()

Financial Planning: CPAs are skilled in financial planning, which can help in managing loan repayments effectively

CPAs possess a deep understanding of financial planning, which is a critical skill in managing loan repayments effectively. This expertise allows them to analyze an individual's financial situation comprehensively, taking into account various factors such as income, expenses, assets, and liabilities. By doing so, they can create a tailored financial plan that optimizes loan repayment strategies while also considering other financial goals and obligations.

One of the key benefits of working with a CPA for loan management is their ability to identify potential tax implications and deductions related to loan repayments. For instance, they can advise on the tax deductibility of student loan interest or the potential benefits of consolidating loans to lower interest rates. This tax-savvy approach can lead to significant savings over the life of the loan.

Furthermore, CPAs can assist in budgeting and cash flow management, which are essential for ensuring timely loan repayments. They can help individuals track their expenses, identify areas for cost-cutting, and develop a realistic budget that allocates sufficient funds for loan payments while also covering other essential expenses. This proactive approach can prevent missed payments and the associated penalties and interest charges.

In addition to these technical skills, CPAs also bring a valuable behavioral perspective to financial planning. They can help individuals overcome common psychological barriers to effective money management, such as procrastination or emotional spending. By providing objective guidance and support, CPAs can empower their clients to make informed financial decisions and stay on track with their loan repayment goals.

Overall, the financial planning expertise of CPAs can be a game-changer for individuals struggling to manage their loan repayments. By leveraging their knowledge of tax laws, budgeting strategies, and behavioral finance, CPAs can help their clients develop a comprehensive and effective plan for paying off loans while also achieving their broader financial objectives.

Explore related products

![]()

Interest Rates: Some lenders offer lower interest rates to CPAs due to their perceived lower risk

Lenders often provide lower interest rates to Certified Public Accountants (CPAs) due to their perceived lower risk profile. This is primarily because CPAs are seen as having a higher level of financial literacy and responsibility, which translates into a reduced likelihood of defaulting on loans. As a result, financial institutions may offer more favorable terms to CPAs, including reduced interest rates, higher credit limits, and more flexible repayment options.

One of the key reasons why CPAs are considered lower risk borrowers is their rigorous training and certification process. Becoming a CPA requires passing a series of challenging exams and meeting strict educational and experience requirements. This demonstrates a high level of competence in financial matters, which lenders view as a positive indicator of creditworthiness. Additionally, CPAs are often subject to regular audits and professional oversight, which further reinforces their credibility and trustworthiness in the eyes of lenders.

Another factor contributing to the lower interest rates offered to CPAs is their typically higher earning potential. CPAs often hold senior positions in finance and accounting departments, or they may own their own practices, which can result in higher incomes compared to the general population. Lenders recognize that borrowers with higher incomes are generally better able to repay their loans, and therefore they may offer more competitive interest rates to attract CPA clients.

It's also worth noting that some lenders may offer special loan programs or discounts specifically tailored to CPAs. These programs may include features such as no application fees, reduced closing costs, or more lenient credit score requirements. By taking advantage of these specialized offerings, CPAs can potentially save money on their loan repayments and enjoy more favorable borrowing terms.

In conclusion, being a CPA can indeed help with loans, particularly in terms of securing lower interest rates. This is due to the combination of factors such as the CPA's perceived lower risk profile, higher earning potential, and the specialized loan programs offered by some lenders. As a result, CPAs who are in the market for a loan may be able to benefit from more favorable terms and conditions compared to non-CPA borrowers.

Explore related products

![]()

Loan Approval: The CPA designation might influence loan approval decisions, as it indicates a high level of financial knowledge

Lenders often view the CPA designation as a strong indicator of financial reliability and expertise. This perception can significantly influence loan approval decisions, as CPAs are seen to possess a deep understanding of financial statements, tax laws, and accounting principles. Their ability to manage complex financial information and provide accurate financial advice can reassure lenders about the borrower's capability to handle loan repayments responsibly.

The CPA designation can also impact the loan terms offered to an individual. For instance, a borrower with a CPA credential may be eligible for more favorable interest rates or higher loan amounts due to their demonstrated financial acumen. Lenders may be more confident in extending credit to CPAs, knowing that they have the professional knowledge to assess and manage their financial obligations effectively.

Moreover, CPAs often have access to detailed financial data and insights that can help them present a strong loan application. They can provide lenders with comprehensive financial statements, tax returns, and other relevant documents that clearly demonstrate their financial stability and creditworthiness. This level of transparency and thoroughness in financial documentation can further enhance their chances of loan approval.

In addition, the CPA designation can serve as a valuable asset when negotiating loan terms. CPAs are trained to analyze financial information critically and can use this skill to evaluate loan offers and negotiate more favorable terms. Their understanding of financial risks and opportunities can help them secure loans that align with their long-term financial goals and strategies.

Overall, being a CPA can indeed help with loan approval by providing lenders with assurance about the borrower's financial knowledge, reliability, and ability to manage credit responsibly. This designation can open up opportunities for more favorable loan terms and higher credit limits, making it a significant advantage in the loan application process.

Frequently asked questions

Being a CPA can be beneficial when applying for loans as it demonstrates a high level of financial expertise and credibility. Lenders may view CPAs as lower-risk borrowers due to their professional knowledge and commitment to ethical financial practices.

A CPA's expertise can potentially lead to more favorable loan terms, such as lower interest rates or higher borrowing limits. Lenders may be more confident in offering better terms to CPAs because of their proven financial management skills and understanding of complex financial concepts.

While there may not be loan programs exclusively for CPAs, some financial institutions offer specialized services or benefits tailored to professionals in the accounting field. These could include streamlined application processes, waived fees, or other perks designed to attract and support CPAs in their financial endeavors.