The question of whether being a loaner counts as income is a complex one, often misunderstood by many. In essence, loaning money to others can indeed generate income through the interest charged on the loan. This interest is typically a percentage of the principal amount loaned out, and it represents the cost of borrowing the money. However, it's important to note that not all loaning situations result in taxable income. For instance, if you loan money to a friend or family member without charging interest, this would generally not be considered income for tax purposes. Additionally, the tax implications can vary depending on the jurisdiction and the specific circumstances of the loan. Therefore, it's crucial to understand the legal and tax implications of loaning money to ensure compliance with relevant laws and regulations.

Explore related products

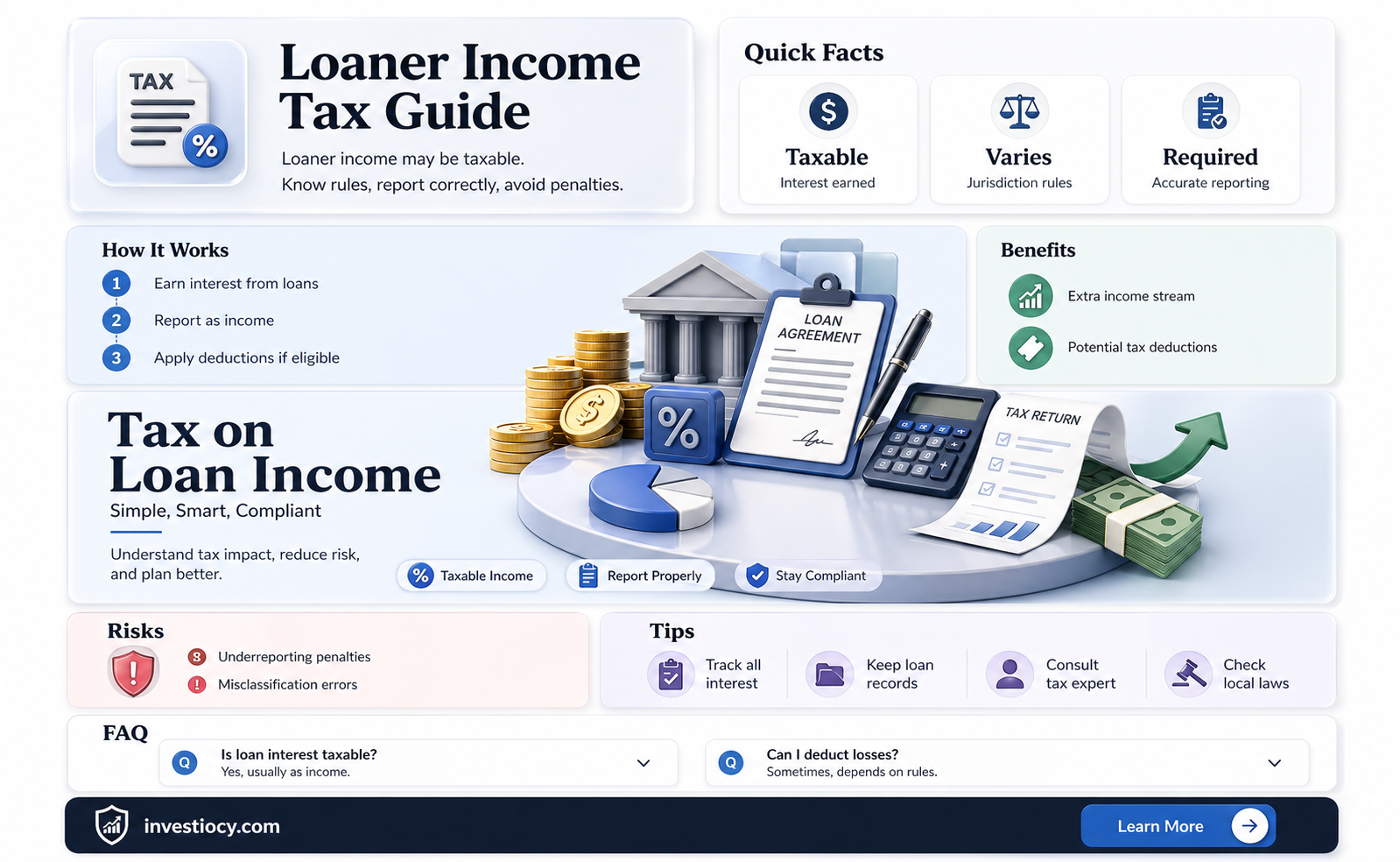

What You'll Learn

- Definition of Income: Clarifying what constitutes income, including various types and sources

- Loan Characteristics: Explaining the features of loans, such as interest rates, terms, and repayment schedules

- Tax Implications: Discussing how loans are treated for tax purposes, including interest deductions and capital gains

- Financial Reporting: Analyzing how loans are reported on financial statements, like balance sheets and income statements

- Economic Impact: Examining the broader economic effects of loans, including their role in monetary policy and economic growth

![]()

Definition of Income: Clarifying what constitutes income, including various types and sources

Income is a fundamental concept in personal finance and economics, representing the flow of money into an individual's or entity's accounts. It encompasses various forms, including wages, salaries, tips, commissions, interest, dividends, rental income, and capital gains. Essentially, income is any monetary benefit received from employment, investments, or other financial activities.

In the context of being a loaner, the question arises whether the interest earned from lending money constitutes income. The answer is affirmative; interest income is a recognized form of income. When an individual lends money to another party, whether through a formal loan agreement or informal arrangement, the interest charged on the loan is considered taxable income. This is because the interest represents compensation for the use of the lender's funds.

However, it's crucial to note that not all forms of lending generate taxable income. For instance, if an individual lends money to a friend or family member without charging interest, this would not be considered income. Additionally, certain types of loans, such as those made through peer-to-peer lending platforms, may have specific tax implications that differ from traditional lending arrangements.

To further complicate matters, the tax treatment of interest income can vary depending on the jurisdiction. In some countries, interest income is taxed at the same rate as other forms of income, while in others, it may be subject to a lower tax rate or even exempt from taxation altogether. It's essential for individuals who earn interest income to consult with a tax professional to understand their specific tax obligations.

In conclusion, being a loaner can indeed count as income, specifically in the form of interest income. However, the tax implications and treatment of this income can vary depending on the circumstances and jurisdiction. It's crucial for individuals who engage in lending activities to be aware of these nuances to ensure compliance with tax laws and regulations.

Boosting Your Loan Approval Odds: The CPA Advantage Unveiled

You may want to see also

Explore related products

![]()

Loan Characteristics: Explaining the features of loans, such as interest rates, terms, and repayment schedules

Loans are financial instruments that allow individuals or businesses to borrow money from lenders, such as banks or credit unions, with the agreement to repay the principal amount plus interest over a specified period. Understanding the characteristics of loans is crucial for borrowers to make informed decisions and manage their finances effectively.

One key feature of loans is the interest rate, which is the percentage of the principal amount that the lender charges as a fee for lending the money. Interest rates can be fixed, meaning they remain constant throughout the loan term, or variable, meaning they can fluctuate based on market conditions. The interest rate directly impacts the total cost of the loan and the amount of each repayment installment.

Another important characteristic is the loan term, which is the length of time the borrower has to repay the loan in full. Loan terms can vary significantly, from short-term loans of a few months to long-term loans of several years. The loan term affects the size of the monthly payments, with longer terms typically resulting in lower payments but higher overall interest costs.

Repayment schedules are also a critical aspect of loans, as they outline how and when the borrower must make payments. Common repayment schedules include monthly installments, quarterly payments, or lump-sum payments at the end of the loan term. Some loans may offer flexible repayment options, allowing borrowers to adjust their payment amounts or frequency based on their financial situation.

In the context of whether being a loaner counts as income, it's important to note that loaning money to others can indeed generate income through interest payments. However, this income is subject to taxation, and lenders must report it to the appropriate tax authorities. Additionally, lending money carries risks, such as the possibility of default or late payments, which can impact the lender's financial stability.

Overall, understanding the characteristics of loans, including interest rates, terms, and repayment schedules, is essential for both borrowers and lenders to navigate the complexities of lending and borrowing effectively.

Explore related products

![]()

Tax Implications: Discussing how loans are treated for tax purposes, including interest deductions and capital gains

Loans can have significant tax implications, both for the lender and the borrower. One of the key areas of interest is the deductibility of loan interest. In many jurisdictions, interest paid on a loan can be deducted from taxable income, reducing the overall tax burden for the borrower. However, this deduction is often subject to certain conditions and limitations. For example, the interest may only be deductible if the loan is used for a specific purpose, such as purchasing a home or funding education expenses. Additionally, there may be caps on the amount of interest that can be deducted, particularly for high-income earners.

From the lender's perspective, the interest received on a loan is generally considered taxable income. This means that lenders must report the interest income on their tax returns and pay tax on it at their marginal rate. However, there are some exceptions and nuances to this rule. For instance, if a lender makes a loan to a family member or friend at below-market interest rates, the difference between the market rate and the actual rate charged may be considered a gift rather than taxable income. This can have implications for both the lender and the borrower, as gifts above a certain threshold may be subject to gift tax.

Capital gains can also come into play when it comes to loans. If a lender sells a loan at a profit, the gain realized from the sale is generally considered taxable income. Similarly, if a borrower repays a loan early, the lender may realize a capital gain on the difference between the face value of the loan and the amount repaid. However, there are specific rules and exceptions that apply to these situations, and it's important for both lenders and borrowers to understand their tax obligations in these scenarios.

In conclusion, the tax implications of loans can be complex and multifaceted. Both lenders and borrowers need to be aware of the potential tax consequences of their actions, and it's often advisable to consult with a tax professional to ensure compliance with all applicable laws and regulations. By understanding the tax implications of loans, individuals can make more informed decisions about their financial arrangements and minimize their tax liabilities.

Explore related products

![]()

Financial Reporting: Analyzing how loans are reported on financial statements, like balance sheets and income statements

In financial reporting, the treatment of loans on financial statements is a critical aspect that can significantly impact the interpretation of a company's financial health. Loans are typically reported as liabilities on the balance sheet, representing the company's obligation to repay the borrowed funds. This classification is straightforward when the loan is taken out, but the reporting becomes more nuanced as the loan is repaid or if the terms of the loan change.

When a company repays a loan, the liability on the balance sheet is reduced, and the cash account is debited. This transaction does not affect the income statement directly, as the repayment of a loan is not considered an expense or revenue. However, the interest paid on the loan is typically reported as an expense on the income statement, reducing the company's net income.

A unique angle to consider in financial reporting is the impact of loan modifications. If a loan is modified, for example, by extending the repayment term or changing the interest rate, the company must reassess the loan's value and report any changes accordingly. This could involve recognizing a gain or loss on the modification, which would affect the income statement.

Another important consideration is the reporting of collateralized loans. If a loan is secured by collateral, such as property or inventory, the value of the collateral must be reported on the balance sheet. The collateral's value can fluctuate, affecting the company's reported assets and liabilities.

In summary, financial reporting of loans involves careful consideration of their classification, repayment, modifications, and collateralization. Each of these factors can have a significant impact on the company's financial statements, and it is essential for financial professionals to understand and accurately report these transactions to provide a clear picture of the company's financial position.

![]()

Economic Impact: Examining the broader economic effects of loans, including their role in monetary policy and economic growth

Loans play a pivotal role in the economy by facilitating the flow of funds between lenders and borrowers. This financial intermediation is crucial for economic growth, as it enables businesses to invest in new projects, individuals to purchase homes or education, and governments to fund infrastructure and public services. The availability of loans can stimulate economic activity by increasing consumer spending and business investment, which in turn can lead to job creation and higher GDP growth.

Monetary policy, conducted by central banks, heavily relies on loans to influence economic conditions. By adjusting interest rates, central banks can make borrowing more or less expensive, thereby affecting the demand for loans. Lower interest rates typically encourage borrowing, leading to increased economic activity, while higher interest rates can slow down borrowing and dampen economic growth. This tool is used to manage inflation, stabilize currency values, and promote overall economic stability.

The economic impact of loans is also evident in their role in financial inclusion. Access to credit can empower individuals and businesses in underserved communities, enabling them to participate more fully in the economy. Microfinance institutions, for example, provide small loans to entrepreneurs in developing countries, helping them to start or expand their businesses and improve their livelihoods. Similarly, student loans can increase access to higher education, which can lead to higher earning potential and better economic opportunities for individuals.

However, the economic effects of loans are not always positive. Excessive borrowing can lead to debt crises, both at the individual and national levels. High levels of debt can constrain economic growth by diverting resources away from productive investments and towards debt servicing. Additionally, the reliance on loans can create vulnerabilities in the financial system, as seen in the 2008 global financial crisis, which was triggered by a housing bubble fueled by subprime lending.

In conclusion, loans are a critical component of the economy, influencing economic growth, monetary policy, and financial inclusion. While they can provide significant benefits, it is essential to manage lending responsibly to avoid the negative consequences of excessive debt and financial instability.

Frequently asked questions

Being a loaner typically refers to lending money to others, which in itself is not considered income. However, if you charge interest on the loans you provide, that interest can be counted as income.

Interest income from loans is generally taxed as ordinary income. The tax rate will depend on your overall income level and tax bracket. It's important to report this income on your tax return to avoid any potential penalties or audits.

Yes, there are several legal and regulatory considerations. For instance, you must comply with usury laws, which limit the amount of interest you can charge. Additionally, you should ensure that your lending activities do not violate any local or federal regulations regarding money lending. It's advisable to consult with a legal professional to understand all the requirements and implications.