The Free Application for Federal Student Aid (FAFSA) is a crucial form that students fill out to determine their eligibility for various types of financial aid, including grants, scholarships, and loans. One common question among students is whether the FAFSA form itself determines the loan provider. To clarify, the FAFSA does not directly choose your loan provider. Instead, it assesses your financial situation and calculates your Expected Family Contribution (EFC), which is then used by schools to determine your eligibility for different aid packages. The loan provider is typically chosen by the school's financial aid office from a list of preferred lenders, or you may have the option to select a lender of your choice. It's important to understand this distinction to navigate the financial aid process effectively.

| Characteristics | Values |

|---|---|

| Loan Provider Selection | The FAFSA (Free Application for Federal Student Aid) does not directly choose your loan provider. Instead, it determines your eligibility for federal student aid and sends this information to the schools you've applied to. |

| Role of FAFSA | FAFSA is an application form used to determine the financial aid eligibility of students seeking federal assistance for higher education. |

| Loan Provider Options | After submitting the FAFSA, students receive a financial aid package from their school, which may include federal loans. The school typically has partnerships with specific loan providers, and students can choose from these options. |

| Federal Loan Types | The types of federal loans a student may be eligible for include Direct Subsidized Loans, Direct Unsubsidized Loans, and PLUS Loans. |

| Loan Provider Criteria | Loan providers must meet certain criteria set by the U.S. Department of Education to participate in the federal student loan program. |

| Student Choice | Students have the right to choose any loan provider that participates in the federal student loan program, not just those suggested by their school. |

| Loan Terms and Conditions | Loan terms and conditions, including interest rates and repayment plans, are standardized for federal loans but may vary slightly between different loan providers. |

| Loan Servicing | After disbursement, federal loans are serviced by loan servicers, which are companies contracted by the U.S. Department of Education to manage the repayment process. |

| Loan Forgiveness Programs | Federal loans may be eligible for loan forgiveness programs, such as Public Service Loan Forgiveness (PSLF), depending on the borrower's employment and repayment history. |

| Private Loan Options | In addition to federal loans, students may also consider private student loans from banks, credit unions, and other financial institutions. |

| Loan Repayment | Repayment of federal loans typically begins six months after graduation or when the borrower's enrollment status changes to less than half-time. |

| Interest Rates | Interest rates on federal loans are fixed and determined by the U.S. Congress. As of the 2023-2024 academic year, the interest rates range from 5.5% to 8.5%. |

| Loan Limits | Federal loan limits vary based on the type of loan, the borrower's dependency status, and the academic year. For example, the maximum Direct Subsidized Loan amount for an undergraduate student is $5,500 for the 2023-2024 academic year. |

| Application Process | To apply for federal student aid, students must complete and submit the FAFSA online at fafsa.gov. The application requires personal and financial information, including income, assets, and family size. |

| Renewal Process | Students must renew their FAFSA application each year to maintain eligibility for federal student aid. The renewal process typically opens in October and uses the previous year's tax information. |

| Additional Resources | For more information about federal student loans and the FAFSA application, students can visit the U.S. Department of Education's website at ed.gov/finaid. |

Explore related products

$12.95 $21.99

What You'll Learn

- FAFSA's Role: FAFSA determines eligibility for federal aid, not the loan provider

- Loan Provider Selection: Borrowers choose their loan provider after receiving a financial aid offer

- Types of Loans: FAFSA covers various loan types, including subsidized, unsubsidized, and PLUS loans

- Interest Rates: Loan interest rates are set by the government, not the provider

- Repayment Options: FAFSA loans offer flexible repayment plans, regardless of the provider

![]()

FAFSA's Role: FAFSA determines eligibility for federal aid, not the loan provider

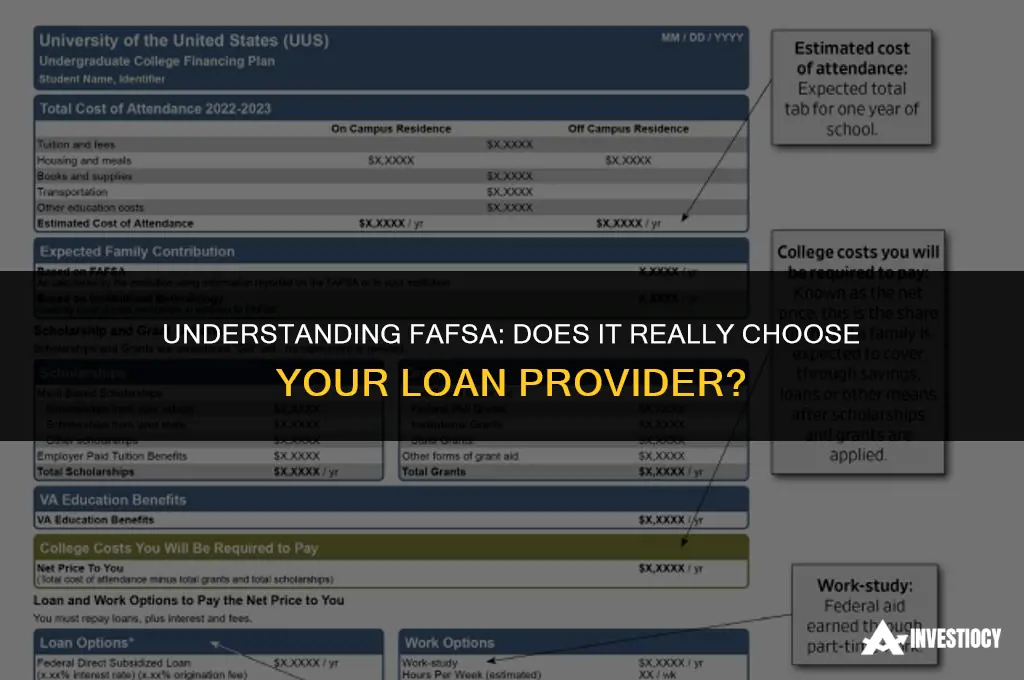

FAFSA, the Free Application for Federal Student Aid, plays a crucial role in the financial aid process for students in the United States. It is important to clarify that FAFSA does not choose your loan provider; rather, it determines your eligibility for federal aid. This distinction is significant because it empowers students to make informed decisions about their financial aid options.

When you submit your FAFSA, the information you provide is used to calculate your Expected Family Contribution (EFC). This figure is then used by schools to determine how much federal aid you are eligible to receive. The aid package may include grants, work-study opportunities, and loans. However, the specific loan provider is not determined by FAFSA. Instead, students have the flexibility to choose their loan provider from a list of approved lenders.

This flexibility allows students to shop around for the best interest rates, repayment terms, and customer service. It is advisable to research different loan providers and compare their offerings before making a decision. Some students may prefer a loan provider that offers additional benefits, such as interest rate reductions for good credit or flexible repayment options.

In summary, while FAFSA is a critical step in the financial aid process, it does not dictate your loan provider. Understanding this distinction can help students navigate the financial aid landscape more effectively and make informed decisions about their educational financing.

Exploring the Universal Path: Do We All Encounter Loans?

You may want to see also

Explore related products

$15.19 $18.99

![]()

Loan Provider Selection: Borrowers choose their loan provider after receiving a financial aid offer

After receiving a financial aid offer, borrowers are often faced with the task of selecting a loan provider. This decision can be crucial as it affects the terms of the loan, the interest rates, and the overall borrowing experience. While the Free Application for Federal Student Aid (FAFSA) determines the amount of aid a student is eligible for, it does not dictate which loan provider the borrower must use. This choice is left to the borrower, and it's important to make an informed decision.

When selecting a loan provider, borrowers should consider several factors. First, they should look at the interest rates offered by different providers. Even a small difference in interest rates can significantly impact the total amount paid over the life of the loan. Additionally, borrowers should consider the repayment terms, such as the length of the repayment period and any penalties for early repayment. Some providers may offer flexible repayment plans or income-driven repayment options, which can be beneficial for borrowers with varying financial situations.

Another important aspect to consider is the customer service and support provided by the loan provider. Borrowers should research the provider's reputation for customer service, as well as their accessibility and responsiveness. This can include looking at online reviews, contacting the provider directly with questions, and assessing their online resources and tools. A provider with good customer service can make the borrowing process smoother and provide assistance if any issues arise during repayment.

Furthermore, borrowers should be aware of any additional benefits or perks offered by loan providers. Some providers may offer rewards programs, discounts for good grades, or other incentives that can help reduce the overall cost of borrowing. It's also important to consider any fees associated with the loan, such as origination fees or late payment fees, as these can add up over time.

In conclusion, selecting a loan provider is a significant decision that should be made carefully. Borrowers should take the time to research and compare different providers based on interest rates, repayment terms, customer service, and additional benefits. By making an informed choice, borrowers can ensure they are getting the best possible terms for their loan and setting themselves up for a successful repayment experience.

Exploring Experian's Loan Services: What You Need to Know

You may want to see also

Explore related products

![]()

Types of Loans: FAFSA covers various loan types, including subsidized, unsubsidized, and PLUS loans

FAFSA, the Free Application for Federal Student Aid, is a crucial form for students seeking financial assistance for their higher education. While it's commonly known that FAFSA determines eligibility for grants and loans, a lesser-known fact is that it does not directly choose your loan provider. This distinction is important for students to understand as they navigate the complex landscape of student loans.

The types of loans available through FAFSA include subsidized, unsubsidized, and PLUS loans. Subsidized loans are need-based and have the government paying the interest while the student is in school. Unsubsidized loans, on the other hand, are not need-based and require the student to pay the interest throughout the loan period. PLUS loans are available to graduate students and parents of undergraduate students, offering a higher loan limit but at a higher interest rate.

One of the key benefits of FAFSA is that it provides students with a standardized way to apply for federal student aid, regardless of the school they attend. This means that students can compare loan offers from different providers and choose the one that best fits their needs. However, it's important to note that not all loan providers participate in the FAFSA process, so students may need to do additional research to find a lender that meets their requirements.

When selecting a loan provider, students should consider factors such as interest rates, repayment terms, and customer service. It's also important to be aware of any additional fees or charges that may be associated with the loan. By carefully comparing loan offers, students can make an informed decision about which provider to choose.

In conclusion, while FAFSA plays a critical role in determining eligibility for student loans, it does not directly choose the loan provider. Students have the freedom to select a lender that best meets their needs, and it's important to carefully consider the terms and conditions of each loan offer before making a decision. By understanding the different types of loans available and the factors to consider when choosing a provider, students can make the most of the financial assistance available to them.

Exploring the Role of Financial Intermediaries in Every Loan

You may want to see also

Explore related products

![]()

Interest Rates: Loan interest rates are set by the government, not the provider

The assertion that "Loan interest rates are set by the government, not the provider" is a critical distinction in understanding the dynamics of student loans. This statement implies that the interest rates on loans, which can significantly impact the total amount repaid, are determined by governmental policies rather than by the individual financial institutions that provide the loans. This can be particularly relevant in the context of FAFSA (Free Application for Federal Student Aid), as it suggests that the interest rates on federal student loans are standardized and regulated by the government, ensuring a level of consistency and fairness across different lenders.

In the realm of federal student loans, the interest rates are indeed set by the U.S. Congress and are based on the 10-year Treasury note rate. This means that all federal student loan borrowers, regardless of their credit history or the lender they choose, will pay the same interest rate for a given loan type. This standardization is designed to protect borrowers from predatory lending practices and to ensure that all students have access to affordable education financing.

However, it's important to note that while the interest rates are set by the government, the actual loan servicing—including the management of loan payments, the handling of deferments and forbearances, and the provision of customer service—is typically carried out by private companies known as loan servicers. These servicers are contracted by the Department of Education to manage the day-to-day aspects of federal student loans.

In contrast, private student loans are not subject to the same governmental interest rate caps. These loans are offered by banks, credit unions, and other financial institutions, and their interest rates can vary widely based on the borrower's creditworthiness, the loan terms, and the lender's policies. As a result, borrowers of private student loans may face higher interest rates and less predictable repayment terms compared to those with federal loans.

Understanding the role of the government in setting interest rates for federal student loans can help borrowers make informed decisions about their education financing. By recognizing that these rates are standardized and regulated, students can focus on other factors when choosing a loan provider, such as the quality of customer service, the availability of repayment plans, and the lender's reputation. This knowledge can empower borrowers to navigate the complex landscape of student loan financing with greater confidence and clarity.

Exploring Loan Recasting Options: A Comprehensive Lender Comparison

You may want to see also

![]()

Repayment Options: FAFSA loans offer flexible repayment plans, regardless of the provider

FAFSA loans, which are facilitated by the Free Application for Federal Student Aid, come with a variety of repayment options designed to accommodate different financial situations. One of the key benefits of these loans is the flexibility they offer in terms of repayment plans, which can be tailored to the borrower's needs regardless of the loan provider. This means that whether you choose a federal loan servicer like Navient or a private lender, you will have access to similar repayment plans.

One popular repayment option for FAFSA loans is the Standard Repayment Plan, which allows borrowers to pay off their loans in equal monthly installments over a period of up to 10 years. This plan is often chosen by those who can afford a higher monthly payment and want to pay off their loans as quickly as possible. Another option is the Graduated Repayment Plan, which starts with lower monthly payments that gradually increase over time. This plan is beneficial for borrowers who expect their income to increase in the future and can afford higher payments later on.

For those who are struggling to make their monthly payments, FAFSA loans also offer income-driven repayment plans. These plans, such as the Revised Pay As You Earn (REPAYE) Plan and the Pay As You Earn (PAYE) Plan, cap monthly payments at a percentage of the borrower's discretionary income. This can help make loan payments more manageable for those with lower incomes or high levels of debt. Additionally, FAFSA loans offer a Public Service Loan Forgiveness (PSLF) program, which can forgive the remaining balance of the loan after 120 qualifying payments for those who work in public service jobs.

It's important to note that while the repayment options for FAFSA loans are flexible, the specific plans available may vary depending on the loan provider. Borrowers should carefully review their repayment options and choose a plan that best fits their financial situation and goals. By understanding the different repayment plans available, borrowers can make informed decisions about how to manage their student loan debt effectively.

Understanding the Impact of Expected Family Contribution on Unsubsidized Stafford Loans

You may want to see also

Frequently asked questions

No, FAFSA does not choose your loan provider. FAFSA, which stands for Free Application for Federal Student Aid, is a form used to determine your eligibility for federal student aid, including loans. It is up to you to choose your loan provider after you have been approved for a loan.

After submitting your FAFSA and receiving your financial aid award letter from your school, you can choose a loan provider. Your school may have a preferred lender list, but you are not required to use any of those lenders. You can research and compare different lenders based on their interest rates, repayment terms, and customer service before making a decision.

Through FAFSA, you can get several types of federal student loans, including Direct Subsidized Loans, Direct Unsubsidized Loans, and Direct PLUS Loans. The type of loan you are eligible for depends on your financial need and other factors. Subsidized loans are for undergraduate students with financial need, and the government pays the interest while you are in school. Unsubsidized loans are available to both undergraduate and graduate students, and you are responsible for paying the interest. PLUS loans are for graduate students and parents of undergraduate students.

FAFSA plays a crucial role in the student loan process by determining your eligibility for federal student aid, including loans. When you submit your FAFSA, the information you provide is used to calculate your Expected Family Contribution (EFC), which is then used by your school to determine how much financial aid you need. Based on your EFC and other factors, your school will offer you a financial aid package that may include federal student loans. You can then choose a loan provider and apply for the loan.