Freddie Mac, a government-sponsored enterprise, plays a significant role in the U.S. housing finance system. One of its primary functions is to purchase loans from lenders, which helps to increase the availability of mortgage credit for homebuyers. By buying these loans, Freddie Mac provides lenders with the necessary liquidity to continue offering mortgages. This process also helps to stabilize the housing market by ensuring a steady supply of mortgage funds. Freddie Mac's loan purchases are subject to certain criteria, including loan size limits and underwriting standards, to ensure that the loans are of high quality and pose minimal risk to the organization.

Explore related products

What You'll Learn

- Loan Eligibility Criteria: Guidelines Freddie Mac follows to determine which loans to purchase

- Types of Loans Purchased: Various loan types Freddie Mac buys, including conventional and multifamily loans

- Loan Servicing: How Freddie Mac handles the servicing of loans it purchases

- Benefits to Lenders: Advantages lenders gain by selling loans to Freddie Mac

- Impact on Housing Market: Freddie Mac's loan purchasing activities' influence on the housing market and economy

![]()

Loan Eligibility Criteria: Guidelines Freddie Mac follows to determine which loans to purchase

Freddie Mac, a government-sponsored enterprise, plays a crucial role in the U.S. housing finance system by purchasing mortgages from lenders. To ensure the quality and reliability of the loans they acquire, Freddie Mac adheres to strict eligibility criteria. These guidelines are designed to mitigate risk and promote responsible lending practices.

One of the primary criteria Freddie Mac considers is the borrower's creditworthiness. This includes evaluating credit scores, payment history, and debt-to-income ratios. Borrowers must demonstrate a solid history of making timely payments on their debts and maintaining a reasonable level of indebtedness relative to their income. Additionally, Freddie Mac may require lenders to verify the borrower's employment history and income to ensure stability and sufficient cash flow to cover mortgage payments.

Another key factor in Freddie Mac's loan eligibility criteria is the property itself. The property must meet certain standards regarding its condition, location, and value. For instance, Freddie Mac may require an appraisal to determine the property's market value and ensure it aligns with the loan amount. The property must also be free of any liens or encumbrances that could jeopardize Freddie Mac's interest in the property.

Furthermore, Freddie Mac has specific requirements for the loan terms and structure. This includes guidelines on the maximum loan-to-value ratio, which varies depending on the type of property and the borrower's credit profile. Freddie Mac also has limits on the loan amount, which are periodically adjusted based on changes in the housing market and regulatory requirements.

In addition to these criteria, Freddie Mac may consider other factors such as the borrower's assets, the purpose of the loan (e.g., purchase or refinance), and the lender's underwriting practices. By evaluating these various elements, Freddie Mac aims to ensure that the loans it purchases are of high quality and pose a minimal risk of default.

Overall, Freddie Mac's loan eligibility criteria are comprehensive and designed to promote responsible lending and borrowing practices. These guidelines help maintain the stability of the housing finance system and ensure that Freddie Mac can continue to support the dream of homeownership for millions of Americans.

Navigating Loan Modifications: Can Foreclosure Be Halted?

You may want to see also

Explore related products

![]()

Types of Loans Purchased: Various loan types Freddie Mac buys, including conventional and multifamily loans

Freddie Mac, a government-sponsored enterprise, plays a significant role in the U.S. housing finance system by purchasing various types of loans from lenders. This process helps to ensure liquidity in the mortgage market and makes homeownership more accessible to millions of Americans. Among the loan types Freddie Mac buys are conventional loans, which are not insured or guaranteed by the government but adhere to specific underwriting standards set by Freddie Mac and Fannie Mae. These loans typically require a minimum credit score of 620 and a debt-to-income ratio of no more than 50%.

In addition to conventional loans, Freddie Mac also purchases multifamily loans, which are mortgages secured by apartment buildings or other residential properties with more than four units. These loans are crucial for financing the construction, acquisition, and refinancing of multifamily housing, thereby supporting the availability of affordable rental units. Freddie Mac’s multifamily loan products include fixed-rate and adjustable-rate options, with various terms and amortization schedules to meet the needs of different borrowers.

Another type of loan Freddie Mac buys is the FHA loan, which is insured by the Federal Housing Administration. FHA loans are popular among first-time homebuyers due to their lower down payment requirements and more lenient credit score criteria. Freddie Mac purchases these loans to support the FHA’s mission of promoting homeownership and ensuring access to affordable housing.

Furthermore, Freddie Mac purchases VA loans, which are guaranteed by the Department of Veterans Affairs and designed to help veterans, active-duty military personnel, and their surviving spouses buy homes. VA loans offer favorable terms, such as no down payment requirements and lower interest rates, making them an attractive option for those who have served in the military.

Lastly, Freddie Mac buys USDA loans, which are guaranteed by the United States Department of Agriculture and aimed at promoting homeownership in rural areas. These loans offer 100% financing, meaning no down payment is required, and are available to borrowers with moderate incomes. By purchasing USDA loans, Freddie Mac supports the USDA’s efforts to improve the quality of life in rural communities.

In summary, Freddie Mac’s loan purchasing activities encompass a wide range of mortgage products, including conventional, multifamily, FHA, VA, and USDA loans. This diverse portfolio helps to maintain a healthy and liquid mortgage market, while also supporting various government initiatives aimed at promoting homeownership and affordable housing.

Exploring the Impact of Forbearance Loans on Cosigners: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Loan Servicing: How Freddie Mac handles the servicing of loans it purchases

Freddie Mac, a government-sponsored enterprise, plays a pivotal role in the U.S. mortgage market by purchasing loans from lenders and securitizing them. However, the process doesn't end there. Loan servicing is a critical aspect of Freddie Mac's operations, involving the management and administration of these loans post-purchase. This includes collecting payments, handling escrow accounts, and ensuring compliance with various regulations.

The servicing of loans purchased by Freddie Mac is typically outsourced to third-party servicers. These servicers are responsible for the day-to-day management of the loans, including sending out monthly statements, collecting payments, and handling any issues that may arise. Freddie Mac, however, retains oversight of these servicers to ensure that they adhere to specific standards and guidelines.

One of the key aspects of loan servicing is the handling of escrow accounts. These accounts are used to hold funds for property taxes and insurance, which are typically paid annually. Servicers are responsible for managing these accounts, ensuring that funds are collected and disbursed appropriately. Freddie Mac has strict guidelines in place to ensure that servicers handle escrow accounts in a fair and transparent manner.

In addition to collecting payments and managing escrow accounts, servicers are also responsible for handling delinquent loans. This involves working with borrowers who have fallen behind on their payments to bring them back to current status. Freddie Mac provides servicers with a range of tools and resources to help with this process, including loan modification programs and foreclosure alternatives.

Overall, the servicing of loans purchased by Freddie Mac is a complex process that involves multiple parties and a range of responsibilities. By outsourcing this process to third-party servicers, Freddie Mac is able to leverage specialized expertise and resources, while still maintaining oversight to ensure that loans are serviced in a fair and efficient manner.

Understanding Foreclosure: Does It Hurt Your Loan Prospects?

You may want to see also

![]()

Benefits to Lenders: Advantages lenders gain by selling loans to Freddie Mac

Lenders benefit significantly from selling loans to Freddie Mac, primarily through the enhancement of their liquidity and the reduction of credit risk. By offloading loans to Freddie Mac, lenders can free up capital that would otherwise be tied up in long-term investments, allowing them to originate more loans and expand their business operations. This increased liquidity can be particularly advantageous in tight financial markets where access to capital is limited.

Another key advantage is the mitigation of credit risk. Freddie Mac assumes the credit risk associated with the loans it purchases, which means lenders are no longer exposed to the possibility of borrower default. This risk transfer can help lenders maintain a healthier balance sheet and reduce the need for costly risk management practices. Furthermore, Freddie Mac's rigorous underwriting standards ensure that the loans it purchases are of high quality, which can enhance the overall creditworthiness of a lender's portfolio.

Selling loans to Freddie Mac can also provide lenders with a predictable and consistent source of revenue. Freddie Mac purchases loans at a price that is typically close to the loan's face value, which means lenders can expect a reliable return on their investment. This predictability can be especially valuable for lenders who need to manage cash flow and plan for future financial obligations.

In addition to these financial benefits, Freddie Mac's loan purchase program can help lenders improve their operational efficiency. By streamlining the loan sale process, Freddie Mac enables lenders to reduce the administrative burden associated with servicing loans, which can free up resources for other business activities. Freddie Mac also provides lenders with access to its sophisticated loan servicing systems and expertise, which can help lenders enhance their own servicing capabilities.

Overall, the benefits lenders gain by selling loans to Freddie Mac are multifaceted, encompassing improvements in liquidity, risk management, revenue predictability, and operational efficiency. These advantages can help lenders strengthen their financial position, expand their business operations, and better serve their customers.

Decoding College Loans: The Role of Freddie and Fannie

You may want to see also

![]()

Impact on Housing Market: Freddie Mac's loan purchasing activities' influence on the housing market and economy

Freddie Mac's loan purchasing activities have a profound impact on the housing market and the broader economy. By buying loans from lenders, Freddie Mac provides a crucial source of liquidity that enables banks and other financial institutions to continue making mortgages. This, in turn, supports the housing market by ensuring that there is a steady supply of credit available to homebuyers.

One of the key ways in which Freddie Mac influences the housing market is through its ability to set standards for the types of loans it will purchase. These standards, which include criteria such as credit scores, debt-to-income ratios, and loan-to-value ratios, effectively determine the terms and conditions that lenders offer to borrowers. By setting these standards, Freddie Mac plays a significant role in shaping the overall health and stability of the housing market.

Furthermore, Freddie Mac's activities have a ripple effect throughout the economy. When the housing market is strong, it tends to boost consumer confidence and spending, which can lead to increased economic growth. Conversely, when the housing market is weak, it can have a negative impact on the economy as a whole. By purchasing loans and supporting the housing market, Freddie Mac helps to mitigate the risk of a housing downturn and its potential consequences for the economy.

In addition to its direct impact on the housing market, Freddie Mac also plays a role in promoting affordable housing and homeownership opportunities. Through its various programs and initiatives, Freddie Mac works to make mortgages more accessible and affordable for a wider range of borrowers, including those with lower incomes or less-than-perfect credit. This not only helps to increase homeownership rates but also contributes to the overall stability and resilience of the housing market.

Overall, Freddie Mac's loan purchasing activities are a critical component of the housing market and the economy. By providing liquidity, setting standards, and promoting affordable housing, Freddie Mac helps to ensure that the housing market remains a vital and dynamic part of the broader economic landscape.

Impact of Loan Foreclosure on Your CIBIL Score: What You Need to Know

You may want to see also

Frequently asked questions

No, Freddie Mac does not buy loans directly from individual borrowers. Instead, it purchases loans from lenders who have already made the loans to borrowers.

Freddie Mac typically buys conventional mortgages, which are loans that are not insured or guaranteed by the government. These loans are often used to purchase or refinance single-family homes.

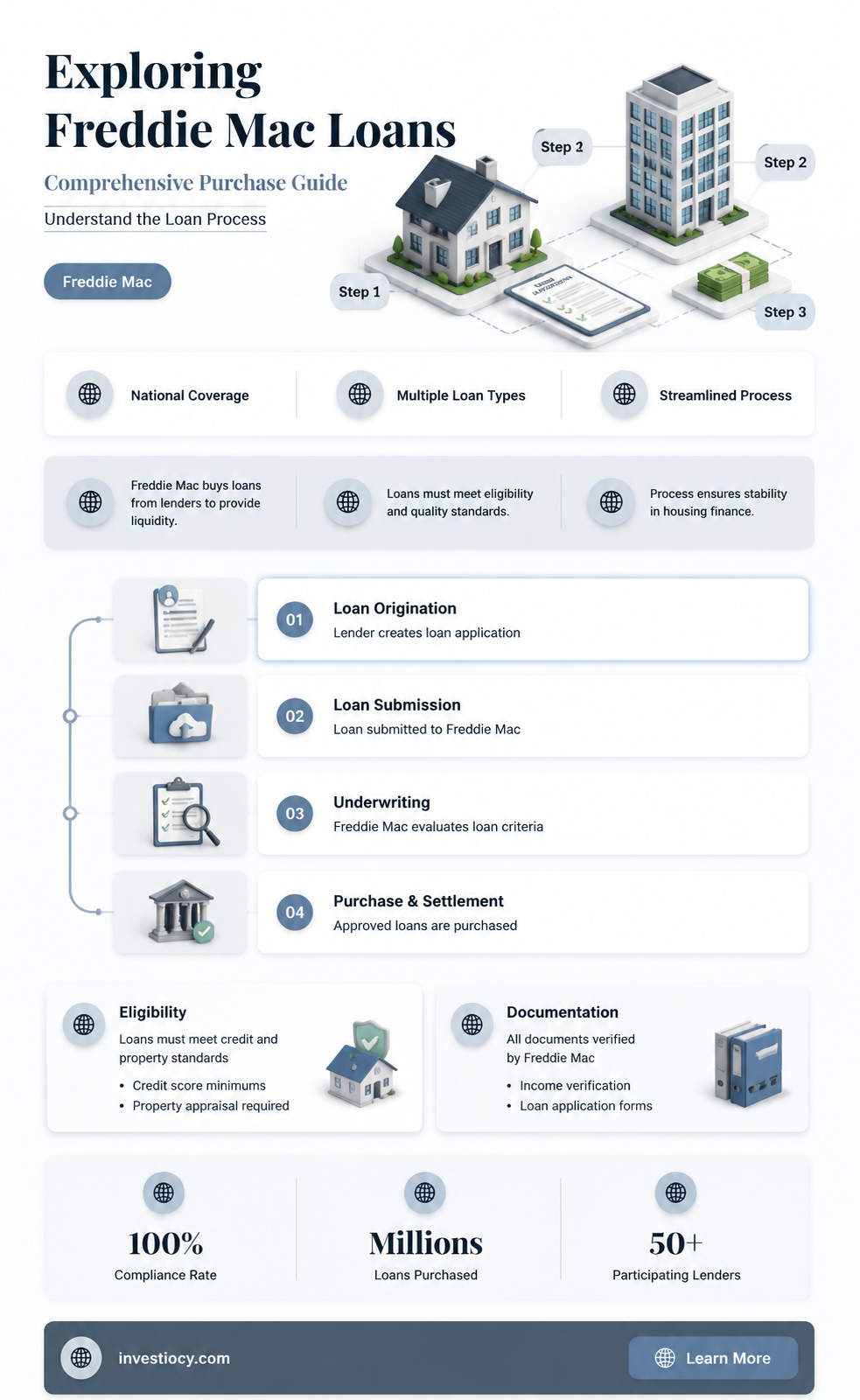

Freddie Mac's loan purchasing process involves several steps. First, a lender originates a loan to a borrower. Then, the lender sells the loan to Freddie Mac. Freddie Mac pools these loans together and sells them as mortgage-backed securities to investors. This process helps to provide liquidity to the mortgage market and allows lenders to make more loans to borrowers.