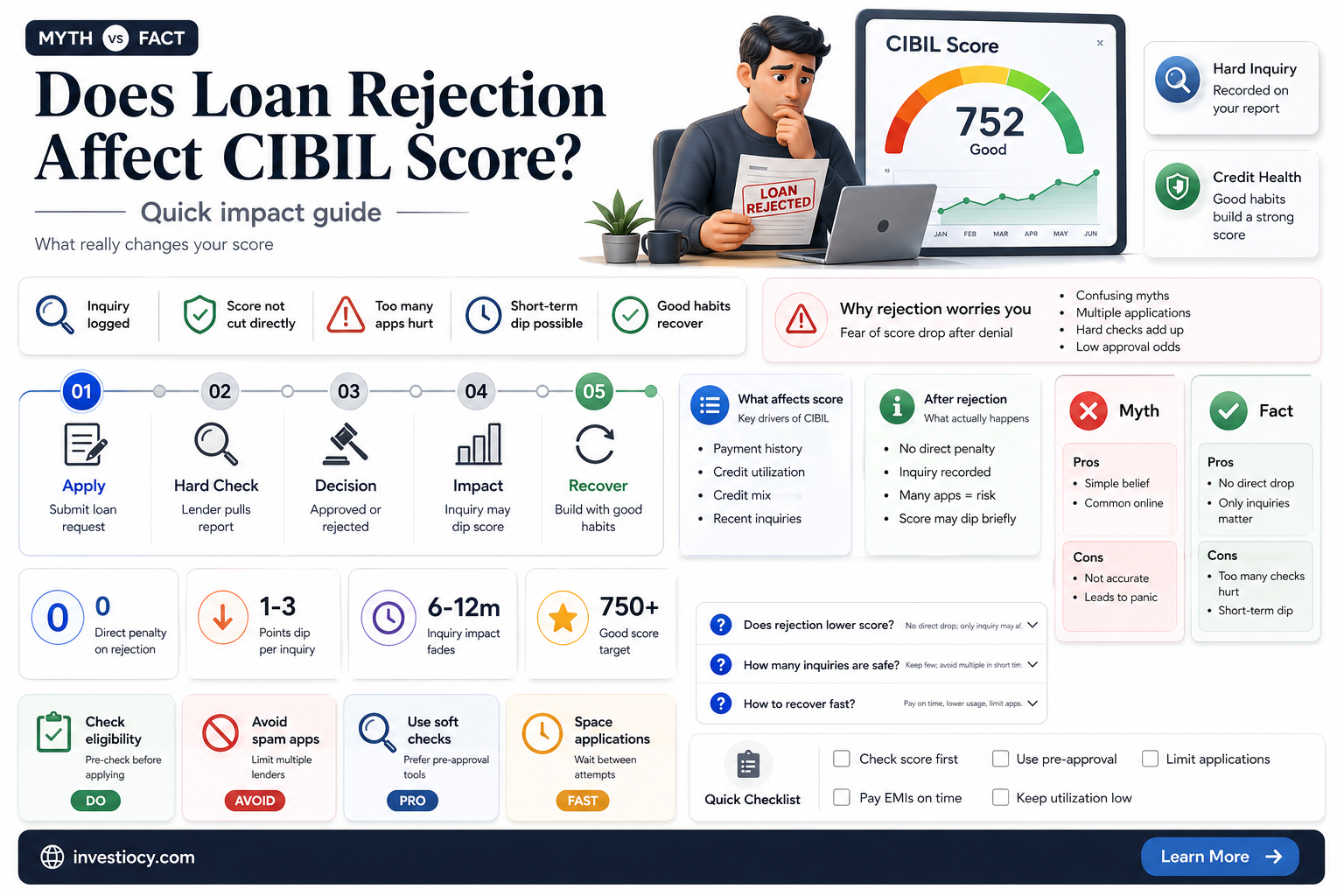

Loan rejection can indeed have an impact on an individual's CIBIL score, which is a critical factor in determining creditworthiness in India. When a loan application is rejected, it may indicate to lenders that the applicant may not be able to repay the loan, leading to a potential decrease in the CIBIL score. This can create a vicious cycle, making it more challenging for the individual to secure credit in the future. It's essential to understand the reasons behind a loan rejection and take steps to improve one's credit profile to mitigate any negative effects on the CIBIL score.

Explore related products

What You'll Learn

- Loan Rejection Definition: Understand what constitutes a loan rejection and its immediate implications

- CIBIL Score Overview: A brief explanation of what a CIBIL score is and its importance

- Impact Analysis: Detailed examination of how loan rejections can influence your CIBIL score

- Credit Report Errors: Common errors in credit reports that might lead to loan rejections

- Improvement Strategies: Tips and strategies to improve your CIBIL score after a loan rejection

![]()

Loan Rejection Definition: Understand what constitutes a loan rejection and its immediate implications

A loan rejection occurs when a financial institution, such as a bank or credit union, denies an applicant's request for a loan. This can happen for various reasons, including a poor credit score, insufficient income, high debt-to-income ratio, or lack of collateral. The immediate implications of a loan rejection can be significant, impacting not only the applicant's financial plans but also their creditworthiness.

One of the key consequences of a loan rejection is its potential impact on the applicant's CIBIL score. CIBIL, or Credit Information Bureau (India) Limited, is a credit bureau that collects and maintains credit information about individuals and businesses. A loan rejection can lead to a negative entry on the applicant's CIBIL report, which can, in turn, lower their credit score. This can make it more difficult for the applicant to secure credit in the future, as lenders often use CIBIL scores to assess creditworthiness.

It's important to note that not all loan rejections will result in a negative impact on the CIBIL score. For example, if the loan application was rejected due to insufficient documentation or a technical error, it may not be reported to CIBIL. However, if the rejection was due to credit-related issues, such as a poor credit history or high debt levels, it is likely to be reported and could negatively affect the applicant's credit score.

To mitigate the impact of a loan rejection on their CIBIL score, applicants can take several steps. First, they should review their credit report to ensure that there are no errors or inaccuracies. If they find any, they can dispute them with CIBIL. Second, they should focus on improving their creditworthiness by paying off existing debts, avoiding new credit, and maintaining a good credit utilization ratio. Finally, they should consider alternative lending options, such as peer-to-peer lending or microfinance institutions, which may have more flexible credit criteria.

In conclusion, a loan rejection can have significant implications for an applicant's financial plans and creditworthiness. Understanding the reasons behind a loan rejection and taking steps to improve creditworthiness can help mitigate its impact on the CIBIL score and increase the chances of securing credit in the future.

State-by-State Variations in Loan Regulations: What You Need to Know

You may want to see also

Explore related products

![]()

CIBIL Score Overview: A brief explanation of what a CIBIL score is and its importance

The CIBIL score is a numerical representation of an individual's creditworthiness, ranging from 300 to 850. It is calculated based on various factors, including payment history, credit utilization, length of credit history, and new credit inquiries. Lenders use this score to assess the risk of lending to a borrower and determine the interest rate and loan terms. A higher CIBIL score indicates a lower risk of default and better credit management, while a lower score suggests a higher risk and potential difficulties in obtaining credit.

The importance of a CIBIL score cannot be overstated, as it plays a crucial role in an individual's financial life. A good credit score can lead to lower interest rates, higher loan amounts, and better credit card offers. On the other hand, a poor credit score can result in loan rejections, higher interest rates, and limited access to credit. Therefore, it is essential to maintain a healthy CIBIL score by making timely payments, keeping credit utilization low, and avoiding excessive credit inquiries.

One common misconception is that loan rejection automatically leads to a decrease in CIBIL score. While it is true that loan rejection can negatively impact credit score, it is not the rejection itself that causes the drop. Instead, it is the factors that led to the rejection, such as missed payments or high credit utilization, that can lower the score. Additionally, applying for multiple loans in a short period can also negatively affect the credit score, as it indicates a higher risk of default.

To mitigate the impact of loan rejection on CIBIL score, it is crucial to address the underlying issues that led to the rejection. This may involve improving payment history, reducing credit utilization, or disputing errors on the credit report. By taking these steps, individuals can not only prevent further damage to their credit score but also improve their chances of obtaining credit in the future.

In conclusion, the CIBIL score is a critical factor in an individual's financial life, and maintaining a healthy score is essential for accessing credit at favorable terms. Loan rejection can negatively impact credit score, but it is the factors leading to rejection that cause the damage. By addressing these issues and practicing responsible credit management, individuals can protect their credit score and improve their financial prospects.

Loan Rehabilitation: Your Path to Ending Wage Garnishment

You may want to see also

![]()

Impact Analysis: Detailed examination of how loan rejections can influence your CIBIL score

Loan rejections can have a significant impact on your CIBIL score, which is a critical factor in determining your creditworthiness. When a loan application is rejected, it is often due to issues related to your credit history, such as late payments, high debt levels, or a lack of credit history. These factors can negatively affect your CIBIL score, making it more difficult for you to secure loans in the future.

One of the primary ways in which loan rejections can influence your CIBIL score is through the inquiry process. When you apply for a loan, the lender will typically conduct a hard inquiry on your credit report. This inquiry can result in a temporary drop in your CIBIL score, as it indicates to credit bureaus that you are actively seeking credit. If you are rejected for the loan, the impact of this inquiry may be more pronounced, as it suggests that you were unable to secure credit despite your efforts.

Furthermore, loan rejections can also lead to a decrease in your credit utilization ratio, which is another important factor in determining your CIBIL score. When you are rejected for a loan, you may be forced to rely on other forms of credit, such as credit cards, which can result in higher credit utilization. This, in turn, can negatively impact your CIBIL score, as credit bureaus view high credit utilization as a sign of financial distress.

In addition to these direct impacts, loan rejections can also have indirect effects on your CIBIL score. For example, if you are rejected for a loan and subsequently struggle to make ends meet, you may be more likely to miss payments or default on other loans. This can lead to further damage to your credit history and a decrease in your CIBIL score.

To mitigate the impact of loan rejections on your CIBIL score, it is important to take proactive steps to improve your creditworthiness. This may include paying off outstanding debts, making timely payments, and avoiding excessive credit inquiries. By taking these steps, you can help to rebuild your credit history and improve your chances of securing loans in the future.

![]()

Credit Report Errors: Common errors in credit reports that might lead to loan rejections

Credit report errors are a significant concern for individuals seeking loans, as they can lead to loan rejections and negatively impact one's credit score. One common error is the presence of inaccurate or outdated information, such as incorrect addresses, phone numbers, or employment details. This can occur when creditors fail to update their records or when individuals move frequently. Another frequent mistake is the misreporting of payment statuses, where a payment made on time is incorrectly marked as late or missed. This can significantly lower a credit score and raise red flags for lenders.

Identity theft is another issue that can result in credit report errors. Fraudulent accounts opened in a person's name can lead to a damaged credit history, even if the individual is unaware of the activity. It is crucial for people to regularly monitor their credit reports to detect any signs of identity theft or other errors. Disputing these errors with the credit bureaus is a necessary step to correct the inaccuracies and potentially improve one's credit score.

Furthermore, credit report errors can sometimes be the result of clerical mistakes made by lenders or credit reporting agencies. For instance, a lender might accidentally report a loan as defaulted when it is actually in good standing. Such errors can be particularly frustrating for borrowers who have consistently made their payments on time. To mitigate these issues, it is essential for individuals to maintain detailed records of their financial transactions and to follow up with lenders to ensure that their payment histories are accurately reported.

In conclusion, credit report errors are a common issue that can lead to loan rejections and negatively impact an individual's credit score. By regularly monitoring their credit reports, disputing inaccuracies, and maintaining detailed financial records, individuals can take proactive steps to protect their credit health and improve their chances of securing loans in the future.

![]()

Improvement Strategies: Tips and strategies to improve your CIBIL score after a loan rejection

After a loan rejection, it's crucial to focus on improving your CIBIL score to enhance your creditworthiness. One effective strategy is to pay off any existing debts promptly and consistently. Timely payments demonstrate responsible credit behavior and can significantly boost your score over time. Additionally, consider reducing your credit utilization ratio by paying down high balances on credit cards and loans. A lower utilization ratio indicates that you're using less of your available credit, which can positively impact your score.

Another key strategy is to avoid applying for multiple loans or credit cards in quick succession. Each application results in a hard inquiry on your credit report, which can temporarily lower your score. Instead, space out your applications and only apply for credit when necessary. Furthermore, it's essential to monitor your credit report regularly for any errors or inaccuracies. Disputing and correcting these errors can help improve your score.

In addition to these strategies, consider diversifying your credit mix. Having a combination of different types of credit, such as credit cards, personal loans, and mortgages, can demonstrate your ability to manage various forms of credit responsibly. However, it's important to avoid taking on more debt than you can handle. Focus on maintaining a healthy credit mix and making timely payments to see improvements in your CIBIL score.

Lastly, be patient and persistent in your efforts to improve your score. Credit score improvement is a gradual process that requires consistent and responsible financial behavior. By following these strategies and maintaining good credit habits, you can increase your chances of loan approval in the future.

Frequently asked questions

Loan rejection itself does not directly lower your CIBIL score. However, the factors that led to the rejection, such as a high debt-to-income ratio or a history of late payments, might be reflected in your credit report and could negatively impact your score.

A loan rejection typically stays on your credit report for a period of 6 to 12 months, depending on the lender's policies and the credit bureau's guidelines. After this period, it should be automatically removed from your report.

Yes, you can improve your CIBIL score after a loan rejection by addressing the underlying issues that led to the rejection. This may include paying off existing debts, making timely payments on your credit cards and loans, and avoiding applying for multiple loans in a short period. Over time, these positive financial behaviors can help boost your credit score.