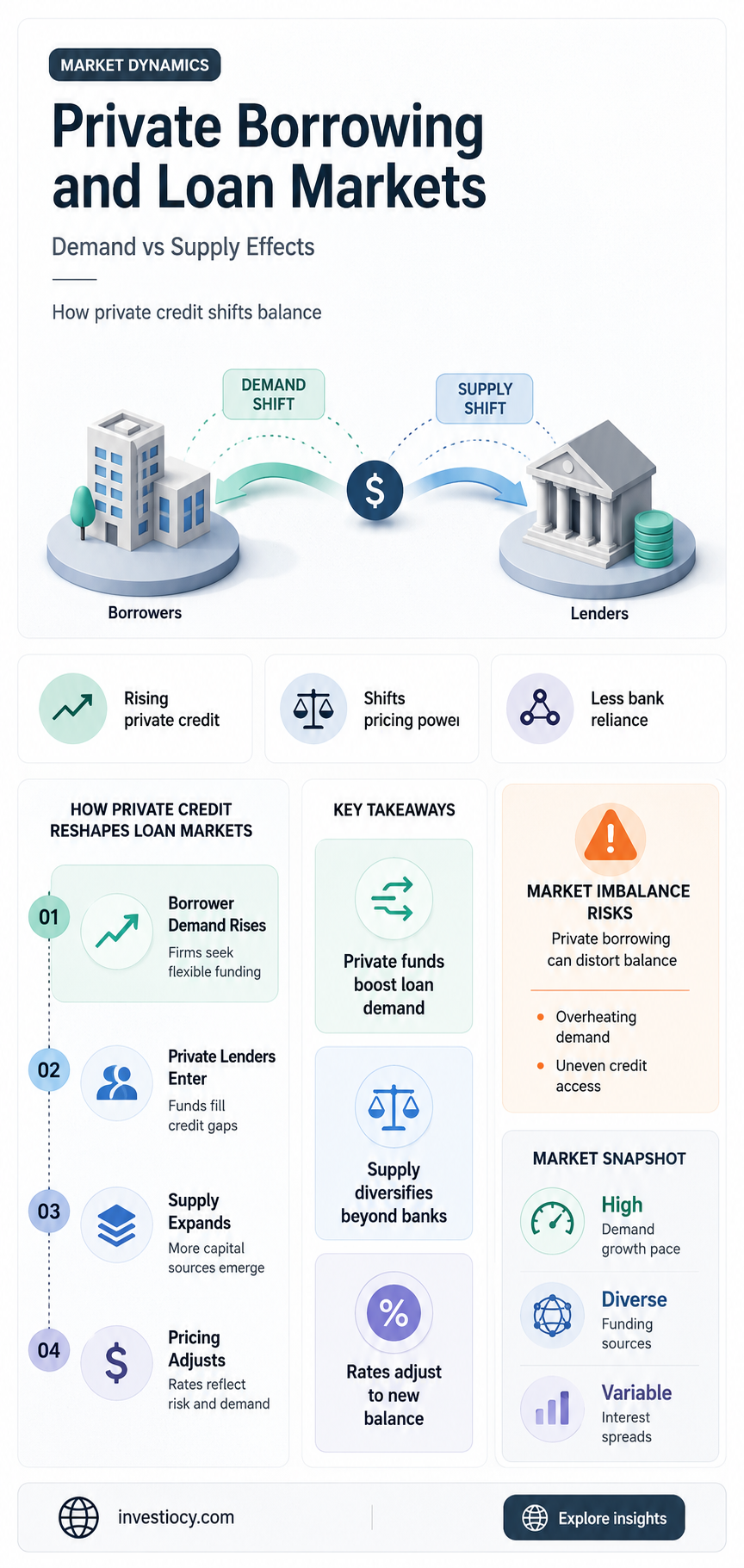

Private borrowing can have a significant impact on the demand and supply of loans in an economy. When individuals or businesses take out loans from private lenders, it increases the demand for credit. This can lead to higher interest rates if the supply of loans remains constant. On the other hand, private borrowing can also stimulate the supply of loans as lenders seek to profit from the increased demand. This can result in a more competitive lending market, potentially driving down interest rates. The overall effect of private borrowing on the demand and supply of loans depends on various factors, including the state of the economy, the availability of credit, and the borrowing habits of consumers and businesses.

Explore related products

What You'll Learn

- Impact on Interest Rates: Analyze how private borrowing influences interest rates and loan affordability

- Credit Availability: Discuss how private borrowing affects the availability of credit for other borrowers

- Economic Growth: Explore the relationship between private borrowing, economic growth, and loan demand

- Risk Assessment: Evaluate how lenders assess risk when private borrowing increases or decreases

- Government Intervention: Examine the role of government policies in regulating private borrowing and its effects on loan supply

![]()

Impact on Interest Rates: Analyze how private borrowing influences interest rates and loan affordability

Private borrowing has a significant impact on interest rates and loan affordability. When individuals or businesses take out loans from private lenders, it increases the demand for credit in the market. This heightened demand can lead to an increase in interest rates as lenders compete for a limited pool of funds. Higher interest rates can make borrowing more expensive, affecting the affordability of loans for consumers and businesses alike.

The relationship between private borrowing and interest rates is complex. On one hand, increased borrowing can drive up interest rates due to higher demand. On the other hand, if private borrowing leads to economic growth, it can also increase the supply of funds available for lending, potentially keeping interest rates in check. However, in times of economic uncertainty or when credit markets are tight, the impact of private borrowing on interest rates can be more pronounced.

Loan affordability is directly influenced by interest rates. When interest rates rise, the cost of borrowing increases, making it more difficult for individuals and businesses to afford loans. This can lead to a decrease in borrowing activity, which in turn can affect economic growth. Conversely, lower interest rates can make loans more affordable, encouraging borrowing and investment.

Private borrowing can also affect the availability of credit. If lenders perceive an increase in credit risk due to higher borrowing levels, they may become more cautious in their lending practices, potentially reducing the availability of loans. This can further impact interest rates and loan affordability, creating a cycle that can be challenging to break.

In conclusion, private borrowing plays a crucial role in shaping interest rates and loan affordability. Understanding this relationship is essential for policymakers, lenders, and borrowers alike. By analyzing the impact of private borrowing on the credit market, stakeholders can make informed decisions that can help maintain a healthy and sustainable economic environment.

Understanding 401(k) Loans: What Does Your Principal Allow?

You may want to see also

Explore related products

![]()

Credit Availability: Discuss how private borrowing affects the availability of credit for other borrowers

Private borrowing can have a significant impact on the availability of credit for other borrowers. When individuals or businesses take out loans from private lenders, it reduces the overall pool of available credit in the market. This is because private lenders have a limited amount of capital to lend, and once it is extended to borrowers, it is no longer available for others. As a result, increased private borrowing can lead to a decrease in credit availability for other potential borrowers.

Furthermore, private borrowing can also affect the interest rates charged on loans. As the demand for credit increases due to private borrowing, lenders may raise their interest rates to compensate for the higher risk and to maximize their profits. This can make it more expensive for other borrowers to access credit, potentially pricing them out of the market.

In addition, private borrowing can influence the types of loans that are available. Private lenders may prioritize certain types of loans, such as those for specific industries or purposes, which can limit the options available to other borrowers. This can be particularly challenging for individuals or businesses that do not fit into the preferred categories of private lenders.

To mitigate the impact of private borrowing on credit availability, it is important for policymakers and financial institutions to implement measures that promote a diverse and competitive lending market. This can include encouraging the development of alternative lending platforms, such as peer-to-peer lending and crowdfunding, which can provide additional sources of credit for borrowers. Additionally, financial institutions can work to improve their risk assessment and loan underwriting processes to ensure that credit is extended to a wider range of borrowers.

In conclusion, private borrowing can have a significant impact on the availability of credit for other borrowers. It can reduce the overall pool of available credit, increase interest rates, and limit the types of loans that are available. To address these challenges, it is important to promote a diverse and competitive lending market that provides a range of credit options for borrowers.

Prequalification vs. Loan Approval: Understanding the Key Differences

You may want to see also

Explore related products

![]()

Economic Growth: Explore the relationship between private borrowing, economic growth, and loan demand

Private borrowing plays a crucial role in stimulating economic growth by increasing the demand for loans. When individuals and businesses borrow more, it indicates a higher level of confidence in the economy, leading to increased investment and consumption. This, in turn, drives up the demand for loans as more people seek financing for various purposes, such as purchasing homes, starting businesses, or expanding existing operations.

The relationship between private borrowing and economic growth is cyclical. As economic growth accelerates, more people have the means and the confidence to borrow, which further fuels growth. Conversely, during economic downturns, borrowing tends to decrease as people become more cautious and risk-averse. This reduction in borrowing can exacerbate the economic slowdown, as it leads to a decrease in investment and consumption.

Loan demand is directly influenced by private borrowing, as the two are closely intertwined. When private borrowing increases, loan demand rises, and vice versa. This relationship is important for banks and financial institutions, as they need to manage their lending activities in line with the prevailing economic conditions. During periods of high loan demand, banks may need to increase their lending capacity, while during periods of low demand, they may need to focus on risk management and loan recovery.

In conclusion, private borrowing has a significant impact on economic growth and loan demand. By understanding this relationship, policymakers and financial institutions can better navigate the complexities of the economy and make informed decisions that promote sustainable growth and stability.

Unveiling the Truth: Does Prime Lending Sell Loans?

You may want to see also

Explore related products

![]()

Risk Assessment: Evaluate how lenders assess risk when private borrowing increases or decreases

Lenders employ various methods to assess risk when private borrowing fluctuates. One primary approach is to analyze the borrower's credit history and score. A higher credit score generally indicates a lower risk of default, while a lower score suggests a higher risk. Lenders may also consider the borrower's debt-to-income ratio, which compares the total monthly debt payments to the monthly gross income. A lower ratio is preferable, as it indicates the borrower has more income available to repay debts.

In addition to individual borrower assessment, lenders evaluate the overall economic environment. During periods of economic growth, lenders may be more willing to take on risk, as borrowers are more likely to have stable incomes and repay their loans. Conversely, during economic downturns, lenders may become more conservative, tightening lending standards to minimize potential losses.

Another factor lenders consider is the collateral provided for the loan. Secured loans, which are backed by collateral such as a home or vehicle, are generally considered less risky than unsecured loans. This is because the lender has the option to seize the collateral if the borrower defaults, thereby mitigating potential losses.

Lenders also assess the interest rate environment. When interest rates are low, borrowing becomes more attractive, potentially leading to an increase in private borrowing. However, low interest rates can also reduce the lender's profit margin, making it more challenging to manage risk effectively.

To further mitigate risk, lenders may diversify their loan portfolios, spreading their investments across various types of borrowers and loan products. This strategy helps to minimize the impact of any single borrower's default on the lender's overall financial health.

In conclusion, lenders use a multifaceted approach to assess risk when private borrowing increases or decreases. By considering factors such as credit history, debt-to-income ratio, economic environment, collateral, interest rates, and portfolio diversification, lenders can make informed decisions to manage risk effectively and ensure the stability of their financial institutions.

Exploring Prime Choice Funding's No-Income Verification Loan Options

You may want to see also

![]()

Government Intervention: Examine the role of government policies in regulating private borrowing and its effects on loan supply

Government policies play a crucial role in regulating private borrowing and its effects on loan supply. One key way in which governments intervene is through the implementation of interest rate policies. Central banks, such as the Federal Reserve in the United States, can adjust interest rates to influence borrowing costs. When interest rates are lowered, borrowing becomes cheaper, which can increase the demand for loans. Conversely, higher interest rates can discourage borrowing, thus reducing demand.

Another form of government intervention is through the regulation of financial institutions. Governments can impose lending restrictions, capital requirements, and other regulatory measures to ensure that banks and other lenders operate safely and responsibly. These regulations can affect the supply of loans by limiting the amount of credit that financial institutions can extend. For example, if a government imposes stricter capital requirements, banks may need to hold more reserves, which could reduce the amount of money available for lending.

Government-sponsored programs can also impact the supply of loans. Programs such as the Small Business Administration (SBA) in the United States provide guarantees for loans made to small businesses, which can encourage lenders to extend credit to these borrowers. Similarly, government-backed mortgage programs can increase the availability of home loans.

In addition to these direct interventions, governments can also influence borrowing behavior through fiscal policy. For instance, tax incentives for borrowing, such as mortgage interest deductions, can encourage individuals and businesses to take on more debt. On the other hand, austerity measures, such as budget cuts and tax increases, can reduce borrowing by making it more expensive or by decreasing the disposable income available for debt repayment.

Overall, government policies can have a significant impact on private borrowing and loan supply. By carefully crafting and implementing these policies, governments can help to ensure a stable and efficient credit market that supports economic growth and development.

How Your Principal Influences Loan Approval: A Comprehensive Guide

You may want to see also

Frequently asked questions

Private borrowing primarily affects the demand side of the loan market. When individuals or businesses take out private loans, they increase the demand for credit. This can lead to higher interest rates if the supply of loans remains constant, as lenders may charge more to meet the increased demand.

An increase in private borrowing can stimulate economic growth by providing individuals and businesses with the funds needed to invest, expand, or consume. However, if borrowing increases too rapidly, it can lead to inflationary pressures and potentially create asset bubbles. Central banks often monitor private borrowing trends to ensure that the economy remains stable.

Financial institutions, such as banks and credit unions, play a crucial role in private borrowing by providing the funds needed for loans. They assess the creditworthiness of borrowers and set interest rates based on the perceived risk. When financial institutions lend more, they increase the supply of loans, which can lower interest rates and encourage more borrowing. Conversely, if they become more conservative in their lending practices, the supply of loans decreases, potentially leading to higher interest rates and reduced borrowing.