To find out how much mortgage interest you've paid, you'll need to review your mortgage statements or contact your lender. Your mortgage statement will typically show the breakdown of your monthly payments, including the portion that goes towards interest. If you don't have access to your statements, you can reach out to your lender's customer service department to request this information. They may be able to provide you with a detailed payment history or guide you through the process of calculating your interest payments. It's important to keep track of your mortgage interest as it may be tax-deductible in some cases, depending on your country's tax laws.

| Characteristics | Values |

|---|---|

| Query Type | Mortgage Interest Paid |

| Purpose | To determine the amount of interest paid on a mortgage |

| Relevant Information | Loan amount, interest rate, loan term, payment frequency |

| Calculation Method | Using a mortgage calculator or manual formula |

| Formula | Total Interest Paid = (Loan Amount x Interest Rate) / (1 - (1 + Interest Rate)^(-Loan Term x Payment Frequency)) |

| Tools Required | Calculator, spreadsheet software (optional) |

| Estimated Time | 10-15 minutes |

| Complexity | Moderate |

| Frequency of Use | Annually, quarterly, or monthly |

| Importance | Helps in understanding mortgage costs, useful for tax deductions |

| Related Queries | How to calculate mortgage payments, how to find mortgage principal paid |

| Additional Tips | Consider using online resources or consulting a financial advisor for more detailed information |

Explore related products

What You'll Learn

- Understanding Mortgage Interest: Learn how mortgage interest works and how it's calculated

- Reviewing Loan Documents: Check your loan agreement for details on interest rates and payment schedules

- Using Online Calculators: Utilize online tools to estimate your mortgage interest payments

- Contacting Your Lender: Reach out to your lender for a detailed breakdown of your mortgage interest

- Tax Implications: Understand how mortgage interest can impact your tax situation and potential deductions

![]()

Understanding Mortgage Interest: Learn how mortgage interest works and how it's calculated

Mortgage interest is a critical component of your monthly mortgage payment, but understanding how it's calculated can be complex. The interest you pay is determined by several factors, including the principal amount of your loan, your interest rate, and the loan term.

To calculate your mortgage interest, lenders typically use an amortization schedule. This schedule breaks down your monthly payments into principal and interest portions. In the early years of your mortgage, a larger portion of your payment goes towards interest, while in the later years, more goes towards the principal.

For example, if you have a $200,000 mortgage with a 4% interest rate and a 30-year term, your monthly payment would be approximately $955. In the first month, about $667 of that payment would go towards interest, and the remaining $288 would go towards the principal.

It's important to note that the interest rate can vary depending on the type of mortgage you have. Fixed-rate mortgages have a constant interest rate throughout the loan term, while adjustable-rate mortgages (ARMs) have rates that can change periodically based on market conditions.

Understanding how your mortgage interest is calculated can help you make informed decisions about your loan and potentially save you money. For instance, making extra payments towards the principal can reduce the amount of interest you pay over the life of the loan.

To find out how much interest you've paid on your mortgage, you can review your loan statements or contact your lender. They should be able to provide you with a detailed breakdown of your payments, including the interest paid to date.

Locate Your HSBC Mortgage Account Number: A Simple Guide

You may want to see also

Explore related products

![]()

Reviewing Loan Documents: Check your loan agreement for details on interest rates and payment schedules

To determine the amount of mortgage interest paid, it's essential to review your loan documents thoroughly. Start by locating your loan agreement, which should contain detailed information about your mortgage, including the interest rate and payment schedule. This document is typically provided at the time of closing and should be kept in a safe and accessible location.

Once you have your loan agreement, look for the section that outlines the interest rate. This could be a fixed rate, which remains constant throughout the life of the loan, or a variable rate, which can fluctuate based on market conditions. Make sure you understand how your interest rate is calculated and whether there are any caps or floors on rate changes.

Next, review the payment schedule section of your loan agreement. This will detail the frequency of your payments (e.g., monthly, bi-weekly), the amount of each payment, and the due dates. It's important to note any prepayment penalties or fees associated with paying off the loan early, as these can impact your overall interest paid.

In addition to your loan agreement, you may also want to review your mortgage statement, which is typically sent to you monthly or quarterly by your lender. This statement will show your current loan balance, the amount of your last payment, and the breakdown of your payment into principal and interest. By reviewing your statements regularly, you can track your progress in paying down your mortgage and identify any discrepancies or errors.

If you're having trouble finding your loan documents or understanding the information they contain, don't hesitate to reach out to your lender for assistance. They can provide you with copies of your documents and help you understand the terms of your loan. Additionally, there are many online resources and calculators available that can help you estimate your mortgage interest paid based on your loan terms and payment history.

Unlocking Opportunities: A Guide to Finding Assumable Mortgages

You may want to see also

Explore related products

![]()

Using Online Calculators: Utilize online tools to estimate your mortgage interest payments

To accurately estimate your mortgage interest payments, you can leverage the power of online calculators. These tools are designed to simplify complex financial calculations, providing you with a clear understanding of your potential interest expenses. Start by searching for reputable mortgage interest calculators on financial websites or banking portals. Look for calculators that allow you to input specific details such as loan amount, interest rate, and loan term.

Once you've found a suitable calculator, begin by entering the principal amount of your mortgage. This is the total sum you've borrowed from the lender. Next, input the annual interest rate, which is typically expressed as a percentage. Be sure to use the correct rate, as even a slight variation can significantly impact your interest payments. The loan term, usually measured in years, is another crucial piece of information. Enter this value to determine the duration over which you'll be paying interest.

After inputting these details, the calculator will generate an estimate of your monthly interest payments. Some calculators may also provide a breakdown of your total interest expenses over the life of the loan. Review these results carefully, taking note of any additional fees or charges that may be included. It's essential to understand that these estimates are based on the information you've provided and may not reflect your actual interest payments, which could be influenced by factors such as payment frequency and amortization schedules.

To get a more comprehensive understanding of your mortgage interest, consider using multiple calculators and comparing the results. This can help you identify any discrepancies and ensure that you're getting an accurate estimate. Additionally, don't hesitate to consult with a financial advisor or mortgage specialist if you have any questions or concerns about your interest payments. They can provide personalized guidance and help you make informed decisions about your mortgage.

Uncovering Your Home's Financial History: A Guide to Finding Mortgage Records

You may want to see also

Explore related products

![]()

Contacting Your Lender: Reach out to your lender for a detailed breakdown of your mortgage interest

To obtain a detailed breakdown of your mortgage interest, the most direct approach is to contact your lender. This can be done through various channels, such as phone, email, or in-person at a local branch. When reaching out, it's essential to have your account information handy, including your loan number and personal identification details. This will help the lender quickly locate your account and provide the specific information you're seeking.

During your communication with the lender, be sure to ask for a clear and detailed explanation of how your mortgage interest is calculated. This should include information on the interest rate, the principal balance, and any additional fees or charges that may apply. Additionally, inquire about the amortization schedule of your loan, which will outline how your payments are allocated between principal and interest over the life of the loan.

It's also important to ask about any prepayment penalties or options for making extra payments towards the principal. This can help you understand how to potentially save on interest payments in the long run. Furthermore, if you're experiencing financial difficulties, don't hesitate to discuss potential hardship programs or loan modification options that may be available to you.

When communicating with your lender, it's crucial to take notes and ask for written confirmation of any information provided. This will ensure that you have a clear and accurate record of your mortgage interest details. Additionally, consider using online resources or mortgage calculators to verify the information provided by your lender and to explore different scenarios for managing your mortgage payments.

In conclusion, contacting your lender is a crucial step in understanding your mortgage interest. By asking the right questions and obtaining detailed information, you can make informed decisions about your mortgage and potentially save money on interest payments over time.

Uncovering Your Past: A Guide to Finding Old Mortgage Account Numbers

You may want to see also

Explore related products

![]()

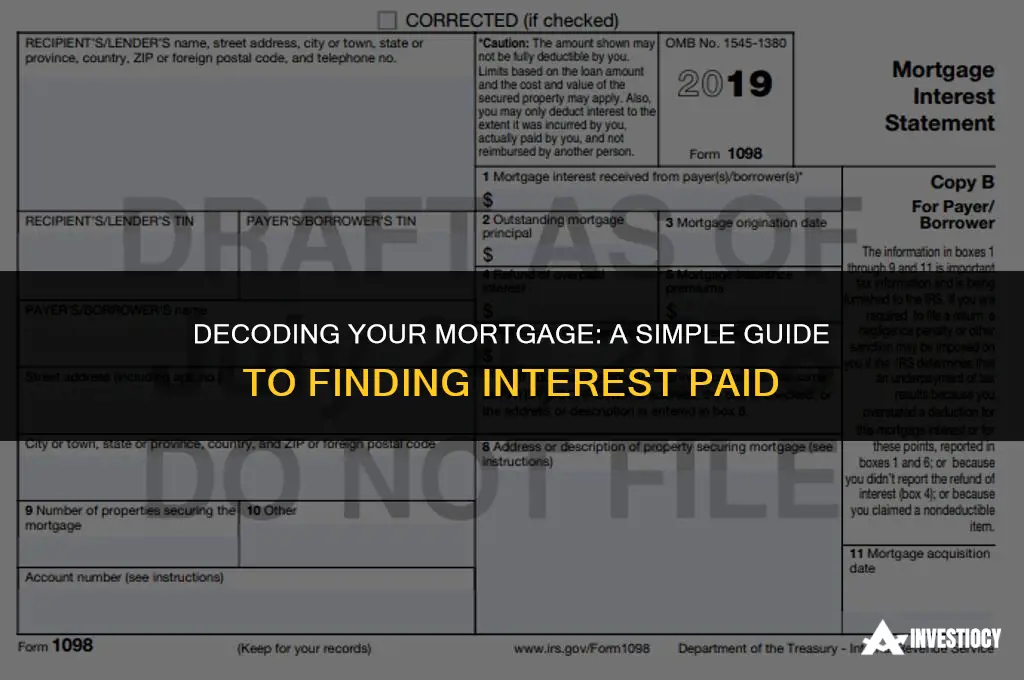

Tax Implications: Understand how mortgage interest can impact your tax situation and potential deductions

Understanding the tax implications of mortgage interest is crucial for homeowners looking to optimize their financial situation. Mortgage interest can significantly impact your tax liability, and being aware of the potential deductions and credits available can lead to substantial savings. Here's a detailed breakdown of how mortgage interest affects your taxes and the steps you can take to maximize your benefits.

First, it's essential to know that mortgage interest is generally tax-deductible. This means that the interest you pay on your mortgage throughout the year can be subtracted from your taxable income, reducing the amount of tax you owe. To claim this deduction, you'll need to itemize your deductions on Schedule A of your tax return. Keep in mind that there are limits to how much mortgage interest you can deduct, especially if your mortgage balance exceeds certain thresholds.

In addition to the mortgage interest deduction, homeowners may also be eligible for other tax benefits related to their mortgage. For example, if you took out a mortgage after 2007, you might qualify for the Mortgage Interest Credit, which allows you to claim a credit of up to $2,000 on your tax return. This credit is designed to help low- to moderate-income homeowners afford their mortgage payments.

To maximize your tax benefits, it's important to keep accurate records of your mortgage interest payments throughout the year. Your lender should provide you with a Form 1098 at the end of each year, which will show the total amount of interest you paid. Make sure to review this form carefully and include the correct amount on your tax return.

Another strategy to consider is making extra mortgage payments. By paying more than your required monthly payment, you can reduce the principal balance of your mortgage, which in turn will lower the amount of interest you pay over time. This can lead to significant tax savings in the long run, as well as help you pay off your mortgage faster.

Finally, it's always a good idea to consult with a tax professional or financial advisor to ensure you're taking full advantage of all the tax benefits available to you. They can help you navigate the complexities of mortgage interest deductions and credits, and provide personalized advice based on your unique financial situation.

Uncover Homeowner Mortgage Secrets: A Property Research Guide

You may want to see also

Frequently asked questions

To determine the amount of mortgage interest you've paid, you can review your mortgage statements or contact your lender directly. Your annual mortgage statement typically includes a breakdown of the interest paid over the past year.

Many lenders provide online platforms or mobile apps where you can access your mortgage information, including interest paid. Log in to your lender's website or app to find this information.

Yes, you can use the formula: Total Interest Paid = (Monthly Payment - Principal Payment) x Number of Payments Made. This calculation assumes a fixed-rate mortgage and that you've been making regular payments.

It's a good practice to review your mortgage interest payments annually, especially when you receive your yearly mortgage statement. This helps you track your progress and ensure the accuracy of the interest charged.

Several factors can influence your mortgage interest payments, including the loan amount, interest rate, loan term, payment frequency, and whether you have an adjustable-rate or fixed-rate mortgage. Making extra payments or refinancing your mortgage can also impact the total interest paid.

![NMLS Study Guide 2026-2027 - 5 Full-Length Practice Tests, SAFE MLO Exam Prep Secrets Book for the Mortgage Loan Originator Exam: [4th Edition]](https://m.media-amazon.com/images/I/717iHac5CwL._AC_UL320_.jpg)