Prepaying your mortgage can be a strategic financial move that allows you to save on interest and potentially pay off your home loan faster. In this guide, we'll explore the various methods and considerations involved in prepaying your mortgage. From understanding the benefits and potential drawbacks to calculating the optimal prepayment amount and frequency, we'll provide you with the information you need to make an informed decision. Additionally, we'll discuss how prepaying your mortgage fits into broader financial planning strategies and how it might impact your overall financial health.

Explore related products

What You'll Learn

- Benefits of Prepaying: Explore the advantages of prepaying your mortgage, such as saving on interest and reducing loan term

- Prepayment Strategies: Discover effective methods to prepay your mortgage, including bi-weekly payments and lump sum payments

- Calculating Prepayment Savings: Learn how to calculate the savings from prepaying your mortgage using online calculators or spreadsheets

- Understanding Prepayment Penalties: Be aware of potential penalties for prepaying your mortgage and how to avoid them

- Impact on Credit Score: Find out how prepaying your mortgage can affect your credit score and overall financial health

![]()

Benefits of Prepaying: Explore the advantages of prepaying your mortgage, such as saving on interest and reducing loan term

Prepaying your mortgage can significantly reduce the total interest paid over the life of the loan. By making extra payments towards the principal, you can lower the outstanding balance, which in turn decreases the amount of interest accrued each month. This can lead to substantial savings, especially in the early years of the mortgage when interest rates are typically higher.

Another advantage of prepaying is the potential to shorten the loan term. By reducing the principal balance, you can effectively compress the repayment period, allowing you to pay off your mortgage sooner than originally planned. This not only saves on interest but also frees up funds that would have otherwise been tied up in mortgage payments, giving you greater financial flexibility.

Prepaying can also provide a sense of security and peace of mind. By reducing your debt burden, you can better weather financial storms, such as job loss or unexpected expenses. Additionally, prepaying can help you build equity in your home more quickly, which can be beneficial if you plan to sell or refinance in the future.

However, it's important to note that prepaying may not always be the best strategy. If you have high-interest debt elsewhere, such as credit card debt, it may be more beneficial to focus on paying off those debts first. Additionally, prepaying may result in penalties or fees, depending on your mortgage terms, so it's essential to review your contract carefully before making extra payments.

In conclusion, prepaying your mortgage can offer several benefits, including saving on interest, reducing the loan term, and providing financial security. However, it's crucial to weigh these advantages against any potential drawbacks and consult with a financial advisor to determine the best approach for your individual situation.

Strategic Steps to Pay Off Your Chase Mortgage Faster

You may want to see also

Explore related products

$21.99 $24.99

![]()

Prepayment Strategies: Discover effective methods to prepay your mortgage, including bi-weekly payments and lump sum payments

One effective prepayment strategy is to make bi-weekly payments instead of the traditional monthly payments. This approach can significantly reduce the total interest paid over the life of the mortgage. By paying half of the monthly payment every two weeks, you end up making 26 payments per year, which is equivalent to 13 full monthly payments. This extra payment can shave years off your mortgage term and save you thousands in interest.

Another strategy is to make lump sum payments whenever possible. This could be from a tax refund, a work bonus, or any other unexpected windfall. Making a large payment all at once can have a dramatic impact on reducing your principal balance, which in turn lowers the amount of interest you pay each month. It’s important to check with your lender to ensure there are no prepayment penalties and to confirm how the payment will be applied to your account.

Consider setting up an automatic payment plan that increases your monthly payment by a fixed amount each year. This strategy, known as an amortization schedule, allows you to gradually increase your payments as your income grows. For example, you could start by paying an extra $50 per month and then increase this amount by $50 each year. Over time, these incremental increases can add up to significant savings on interest and a shorter mortgage term.

If you’re looking for a more aggressive prepayment strategy, you might consider refinancing your mortgage to a shorter term, such as a 15-year fixed-rate mortgage. While this will increase your monthly payments, it can also result in substantial interest savings over the life of the loan. Additionally, refinancing to a lower interest rate can further reduce your monthly payments and total interest paid.

Before implementing any prepayment strategy, it’s crucial to review your financial situation and goals. Ensure that you have an emergency fund in place and that you’re not neglecting other important financial obligations, such as retirement savings or high-interest debt. It’s also a good idea to consult with a financial advisor or mortgage professional to determine the best prepayment strategy for your specific circumstances.

Strategic Steps to Pay Off Your Mortgage Faster

You may want to see also

Explore related products

![]()

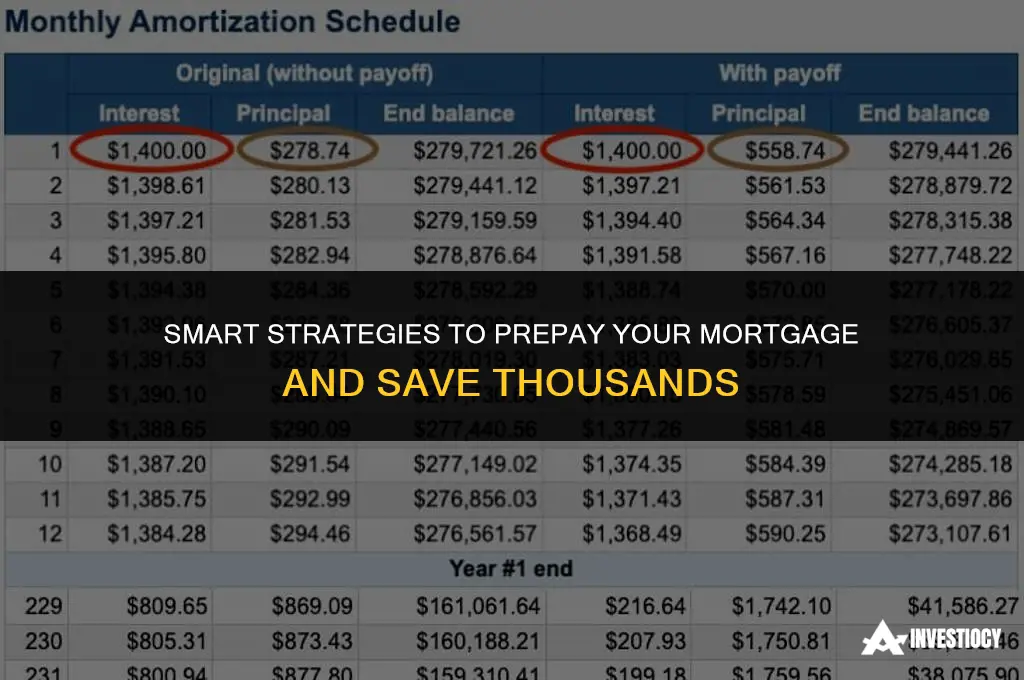

Calculating Prepayment Savings: Learn how to calculate the savings from prepaying your mortgage using online calculators or spreadsheets

To calculate the savings from prepaying your mortgage, you can leverage the power of online calculators or spreadsheets. These tools simplify the complex financial calculations involved, allowing you to make informed decisions about your prepayment strategy. Start by gathering key information about your mortgage, including the principal balance, interest rate, loan term, and monthly payment. With this data in hand, you're ready to begin your calculations.

One popular online resource for mortgage prepayment calculations is the Mortgage Prepayment Calculator provided by NerdWallet. This tool allows you to input your mortgage details and prepayment amount, then instantly displays the potential savings in interest and the new payoff date. For those who prefer a more hands-on approach, creating a spreadsheet in Microsoft Excel or Google Sheets can provide a customizable solution. You can set up formulas to calculate the interest savings and new loan balance based on different prepayment scenarios.

When using a spreadsheet, it's essential to understand the basic principles of mortgage amortization. This involves calculating the portion of each payment that goes towards interest and principal, then adjusting these amounts based on your prepayment. A helpful formula to know is the PMT function in Excel, which calculates the payment for a loan based on constant payments and a constant interest rate. By modifying this formula, you can determine the impact of prepayments on your loan balance and interest payments.

As you explore prepayment strategies, consider the concept of opportunity cost. While prepaying your mortgage can save you money on interest, it may also tie up funds that could be used for other investments or expenses. Calculate the potential returns on alternative investments, such as stocks or bonds, to determine if prepaying your mortgage is the most effective use of your money. Additionally, factor in any prepayment penalties that may apply to your mortgage, as these can offset some of the interest savings.

In conclusion, calculating the savings from prepaying your mortgage requires careful consideration of various financial factors. By utilizing online calculators or spreadsheets, you can make accurate calculations and informed decisions about your prepayment strategy. Remember to consider the opportunity cost of prepayment and any potential penalties, and always consult with a financial advisor before making significant changes to your mortgage plan.

Securing Your Dream Home: A Beginner's Guide to Mortgages

You may want to see also

Explore related products

![NMLS Study Guide 2026-2027 - 5 Full-Length Practice Tests, SAFE MLO Exam Prep Secrets Book for the Mortgage Loan Originator Exam: [4th Edition]](https://m.media-amazon.com/images/I/717iHac5CwL._AC_UL320_.jpg)

![]()

Understanding Prepayment Penalties: Be aware of potential penalties for prepaying your mortgage and how to avoid them

Prepayment penalties are fees charged by lenders when a borrower pays off their mortgage ahead of schedule. These penalties can significantly impact the cost-effectiveness of prepaying your mortgage. To avoid them, it's crucial to understand the terms of your mortgage agreement and the types of prepayment penalties that may apply.

There are typically two types of prepayment penalties: soft and hard. Soft prepayment penalties are based on a percentage of the remaining loan balance, while hard prepayment penalties are a fixed amount. Some mortgages may also have a declining prepayment penalty, which decreases over time. Review your mortgage contract to determine which type of penalty, if any, applies to your loan.

To avoid prepayment penalties, consider the following strategies:

- Wait until the penalty period expires: Many mortgages have a prepayment penalty that only applies during the initial years of the loan. If you can wait until this period ends, you may be able to prepay your mortgage without incurring a penalty.

- Make extra payments strategically: Instead of making a large lump sum payment, consider making smaller extra payments throughout the year. This can help you pay down your mortgage faster without triggering a prepayment penalty.

- Refinance your mortgage: If you're looking to prepay your mortgage and avoid penalties, refinancing to a new loan with more favorable terms may be an option. However, be sure to weigh the costs of refinancing against the potential savings from prepaying your mortgage.

- Negotiate with your lender: In some cases, you may be able to negotiate with your lender to waive or reduce the prepayment penalty. This is more likely to be successful if you have a strong payment history and a good relationship with your lender.

By understanding the terms of your mortgage and the potential prepayment penalties, you can make informed decisions about how to prepay your mortgage while minimizing additional costs.

Navigating the Process: How to Successfully Port Your Mortgage

You may want to see also

Explore related products

![]()

Impact on Credit Score: Find out how prepaying your mortgage can affect your credit score and overall financial health

Prepaying your mortgage can have a significant impact on your credit score, which is a crucial aspect of your overall financial health. When you make extra payments towards your mortgage principal, it demonstrates to lenders that you are a responsible borrower who is capable of managing debt effectively. This behavior can lead to an increase in your credit score over time, as it shows a pattern of timely payments and a commitment to reducing your debt burden.

One of the key factors that influence your credit score is your debt-to-income ratio. By prepaying your mortgage, you can lower this ratio, which can further improve your creditworthiness. A lower debt-to-income ratio indicates that you have more disposable income to cover your monthly expenses and other financial obligations, making you a more attractive borrower in the eyes of lenders.

However, it's important to note that prepaying your mortgage may not always result in an immediate boost to your credit score. Credit scoring models take into account various factors, including the length of your credit history, the types of credit you have, and your payment history. While prepaying your mortgage can positively impact your payment history and debt-to-income ratio, it may not significantly affect other factors such as credit history length or credit mix.

To maximize the impact of prepaying your mortgage on your credit score, it's essential to maintain a consistent payment schedule and avoid missing any payments. Additionally, consider diversifying your credit mix by having a combination of different types of credit, such as credit cards, loans, and mortgages. This can help improve your overall credit profile and increase your credit score.

In conclusion, prepaying your mortgage can have a positive impact on your credit score and overall financial health. By demonstrating responsible borrowing behavior, lowering your debt-to-income ratio, and maintaining a consistent payment schedule, you can improve your creditworthiness and increase your chances of obtaining favorable loan terms in the future.

Accelerate Your Mortgage Payoff: Proven Strategies for Financial Freedom

You may want to see also

Frequently asked questions

Prepaying your mortgage can help you save on interest, reduce your monthly payments, and potentially pay off your loan faster. It can also increase your home equity and provide financial flexibility.

It depends on your lender and the terms of your loan. Some mortgages have prepayment penalties, especially in the early years of the loan. It's important to review your loan agreement or contact your lender to understand any potential penalties.

Even small extra payments can make a difference over time. For example, adding $100 to your monthly payment can save you thousands in interest and help you pay off your loan faster. However, the exact amount depends on your individual situation and financial goals.

The decision to prepay your mortgage or invest elsewhere depends on your financial goals, risk tolerance, and the interest rates on your mortgage and potential investments. Generally, if you have a high-interest mortgage, prepaying may be a good option. If you have a low-interest mortgage and can earn a higher return on your investments, investing elsewhere might be more beneficial.

Prepaying your mortgage can have a positive impact on your credit score, as it demonstrates responsible financial behavior and reduces your debt-to-income ratio. However, the effect on your credit score may vary depending on your individual financial situation and credit history.