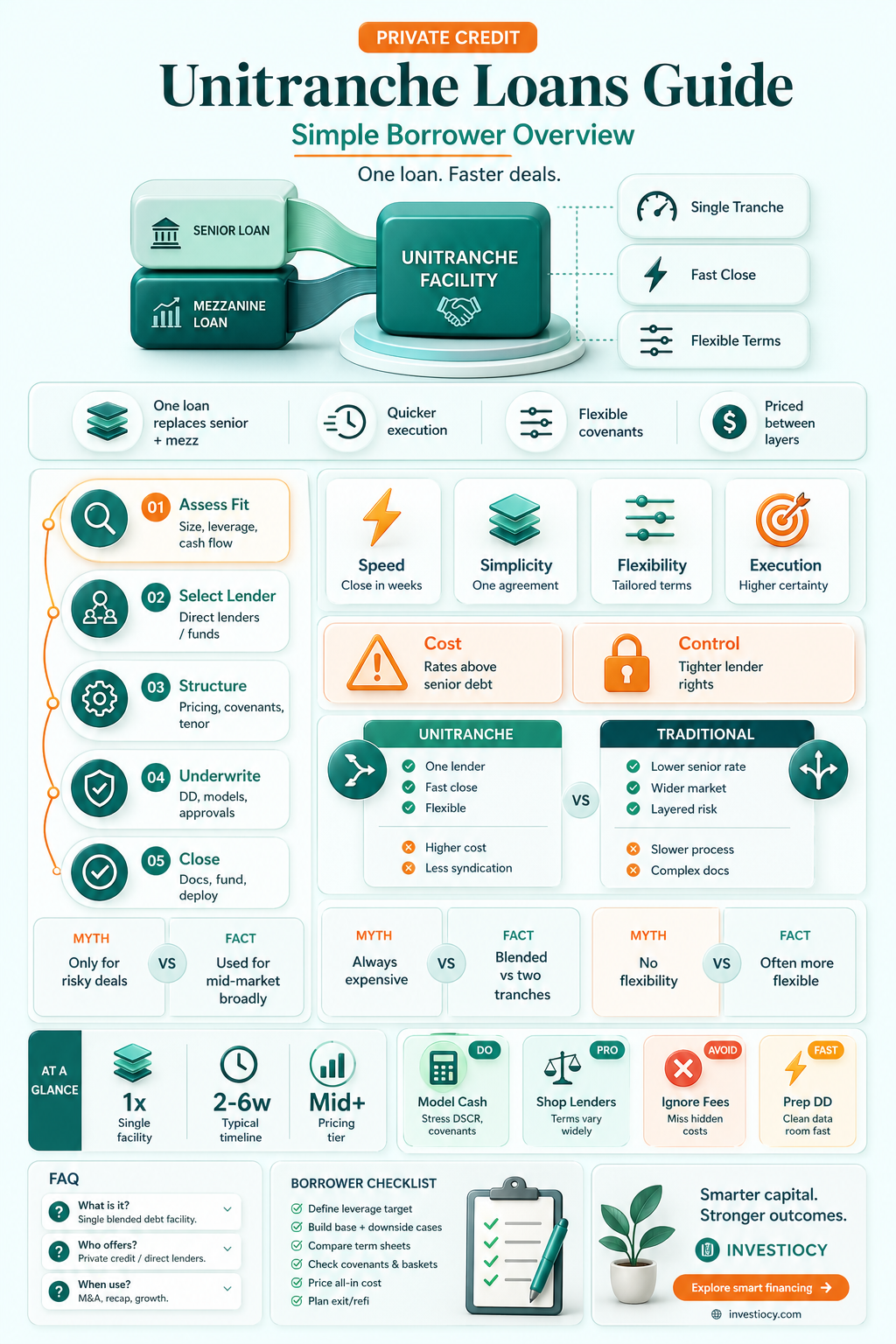

A unitranche loan is a type of financing that combines the features of both senior and mezzanine debt into a single tranche. This hybrid structure allows borrowers to access capital at a lower cost than traditional mezzanine financing while providing lenders with a higher level of security than unsecured debt. Unitranche loans are typically used to fund acquisitions, recapitalizations, or growth initiatives, and they offer a flexible solution for companies that may not qualify for traditional bank financing. With a unitranche loan, the borrower receives a single lump sum of capital, which is then repaid in installments over a predetermined period. The interest rate on a unitranche loan is usually fixed, and the loan is often secured by the borrower's assets, such as property, equipment, or intellectual property.

Explore related products

What You'll Learn

- Definition: A unitranche loan is a type of loan that combines features of both secured and unsecured loans

- Structure: It involves a single tranche of debt, meaning there's only one class of lenders with equal rights

- Collateral: Unitranche loans are typically secured by assets, such as property or equipment, but may also include unsecured portions

- Interest Rates: These loans often have variable interest rates, which can change based on market conditions or borrower performance

- Usage: Unitranche loans are commonly used in corporate finance, real estate, and project financing due to their flexible structure

![]()

Definition: A unitranche loan is a type of loan that combines features of both secured and unsecured loans

A unitranche loan is a hybrid financial instrument that merges the characteristics of secured and unsecured loans. This type of loan is structured to provide the lender with a security interest in the borrower's assets, similar to a secured loan, while also offering the borrower the flexibility typically associated with unsecured loans. The term "unitranche" is derived from the combination of "unit" and "tranche," indicating a single tranche of debt that is divided into different portions with varying levels of security.

In a unitranche loan agreement, the lender typically has a claim on the borrower's assets as collateral, but the assets are not pledged exclusively to secure the loan. This means that the lender has a degree of protection in the event of default, as they can pursue the collateral to recover their losses. However, the borrower retains some control over the assets and may be able to use them for other purposes, subject to the terms of the loan agreement.

One of the key benefits of a unitranche loan is its flexibility. Borrowers can access funds without having to pledge all of their assets as collateral, which can be particularly advantageous for businesses that need to maintain liquidity or for individuals who do not have significant assets to offer as security. Additionally, unitranche loans can be tailored to meet the specific needs of the borrower, with varying interest rates, repayment terms, and levels of security.

Despite the advantages, unitranche loans also carry certain risks. Lenders may face a higher risk of default if the borrower is unable to repay the loan, as the collateral may not be sufficient to cover the entire amount owed. Borrowers, on the other hand, may be subject to higher interest rates and fees compared to traditional secured loans, as the lender is taking on additional risk.

In conclusion, a unitranche loan is a versatile financial tool that combines the security of a secured loan with the flexibility of an unsecured loan. It offers borrowers access to funds without requiring them to pledge all of their assets as collateral, while providing lenders with some level of protection in the event of default. However, it is essential for both borrowers and lenders to carefully consider the risks and benefits associated with unitranche loans before entering into such an agreement.

Unlocking Opportunities: Your Guide to Becoming a Loan Signing Agent in Florida

You may want to see also

Explore related products

![]()

Structure: It involves a single tranche of debt, meaning there's only one class of lenders with equal rights

A unitranche loan is characterized by its unique structure, which involves a single tranche of debt. This means that there is only one class of lenders, all of whom have equal rights and claims on the borrowed funds. This structure simplifies the loan agreement and can make it more attractive to borrowers who want to avoid the complexity of multiple tranches with different terms and conditions.

One of the key benefits of a unitranche loan is that it can provide borrowers with greater flexibility in terms of how they use the borrowed funds. Because there is only one tranche, borrowers do not have to worry about allocating funds to specific tranches or meeting the requirements of different lenders. This can be particularly advantageous for borrowers who need to use the funds for a variety of purposes or who want to have the ability to adjust their repayment schedule as needed.

Another advantage of a unitranche loan is that it can often result in lower interest rates and fees. Because there is only one class of lenders, the loan agreement can be more straightforward and less expensive to administer. This can lead to cost savings for borrowers, which can be particularly important for businesses or individuals who are looking to minimize their financing costs.

However, it is important to note that a unitranche loan may not be suitable for all borrowers. For example, borrowers who need to raise a large amount of capital may find that a unitranche loan is not sufficient to meet their needs. Additionally, borrowers who have a poor credit history or who are considered high-risk may have difficulty qualifying for a unitranche loan.

In conclusion, a unitranche loan can be a valuable financing option for borrowers who are looking for a simple, flexible, and cost-effective way to raise capital. By understanding the unique structure and benefits of a unitranche loan, borrowers can make informed decisions about whether this type of loan is right for them.

Explore related products

![]()

Collateral: Unitranche loans are typically secured by assets, such as property or equipment, but may also include unsecured portions

Unitranche loans, a hybrid financing solution, often require collateral to secure the lender's interest. This collateral can take various forms, such as property, equipment, or other tangible assets. However, what sets unitranche loans apart is their flexibility in also incorporating unsecured portions. This unique feature allows borrowers to access funding without having to pledge additional assets, which can be particularly beneficial for companies with limited collateral or those seeking to preserve their asset base.

The inclusion of unsecured portions in unitranche loans introduces a higher level of risk for lenders, which is typically mitigated by charging higher interest rates or fees. Borrowers must carefully consider the trade-offs between the benefits of accessing capital without additional collateral and the potential costs associated with unsecured debt. Furthermore, the structure of unitranche loans, which combines elements of both secured and unsecured debt, requires a nuanced understanding of the legal and financial implications.

In practice, the collateral provided for unitranche loans is often appraised to determine its value and the loan-to-value ratio. This ratio is crucial in assessing the lender's risk and determining the loan terms. Borrowers should be prepared to provide detailed information about their assets and financial position to support the lender's due diligence process. Additionally, it is essential for borrowers to understand the potential consequences of defaulting on a unitranche loan, as the lender may have the right to seize the pledged collateral and pursue other legal remedies.

Overall, the collateral aspect of unitranche loans is a critical component that borrowers must carefully navigate. By understanding the intricacies of collateral requirements and the implications of unsecured portions, borrowers can make informed decisions about their financing options and effectively manage their financial risk.

![]()

Interest Rates: These loans often have variable interest rates, which can change based on market conditions or borrower performance

Unitranche loans, characterized by their blended features of term loans and revolving credit facilities, often come with variable interest rates. These rates are not fixed and can fluctuate based on several factors, primarily market conditions and the borrower's performance. Market conditions, such as changes in the prime rate or other benchmark interest rates, can directly influence the interest rate on a unitranche loan. Additionally, the borrower's creditworthiness, payment history, and overall financial health can also impact the rate, as lenders may adjust the interest rate to reflect the perceived risk of lending to a particular borrower.

The variability of interest rates on unitranche loans can have significant implications for borrowers. For instance, if market conditions lead to an increase in interest rates, the borrower's cost of borrowing will rise, potentially affecting their cash flow and profitability. Conversely, if interest rates decrease, the borrower may benefit from lower borrowing costs. Borrowers need to be aware of these fluctuations and plan accordingly to manage their financial obligations effectively.

Lenders offering unitranche loans may also include covenants or conditions that allow them to adjust the interest rate based on specific triggers, such as changes in the borrower's debt-to-equity ratio or EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization). These triggers can serve as early warning signs of potential financial distress, prompting the lender to increase the interest rate to mitigate risk.

To navigate the complexities of variable interest rates on unitranche loans, borrowers should carefully review the loan agreement and understand the factors that can influence rate changes. They should also consider hedging strategies, such as interest rate swaps or caps, to protect against potential rate increases. By being proactive and informed, borrowers can better manage the risks associated with variable interest rates and ensure that their unitranche loan remains a beneficial financial tool.

![]()

Usage: Unitranche loans are commonly used in corporate finance, real estate, and project financing due to their flexible structure

Unitranche loans have become a popular financing option in various sectors due to their unique structure that combines the features of both senior and mezzanine debt. In corporate finance, these loans are often used to fund acquisitions, recapitalizations, or growth initiatives. The flexible nature of unitranche loans allows companies to tailor the financing to their specific needs, with the ability to adjust the loan terms and conditions to align with their financial goals and risk tolerance.

In the real estate sector, unitranche loans are commonly used to finance property acquisitions, renovations, or construction projects. These loans provide developers and investors with the necessary capital to undertake large-scale projects, while also offering a more streamlined and efficient financing process compared to traditional bank loans. The ability to customize the loan structure to fit the unique aspects of each project is a significant advantage in the fast-paced and dynamic real estate market.

Project financing is another area where unitranche loans have gained traction. These loans are particularly well-suited for funding infrastructure projects, such as transportation systems, energy facilities, or public-private partnerships. The long-term nature of unitranche loans, combined with their flexible repayment schedules, makes them an attractive option for financing projects with extended timelines and complex cash flow profiles. Additionally, the ability to incorporate various tranches within a single loan facility allows project sponsors to manage their financing needs more effectively and mitigate risks associated with funding large-scale initiatives.

Overall, the usage of unitranche loans across different sectors highlights their versatility and adaptability to various financing needs. As a result, these loans have become an essential tool for companies, developers, and project sponsors seeking innovative and flexible financing solutions.

Frequently asked questions

A unitranche loan is a type of financing that combines the features of both secured and unsecured loans. It is typically used by businesses to fund working capital, equipment purchases, or other operational needs.

In a unitranche loan, the lender provides a single tranche of capital that is secured by a lien on the borrower's assets. This lien gives the lender priority over other creditors in the event of default. The loan is repaid over time, usually with interest, until the principal amount is fully paid off.

Unitranche loans offer several benefits, including:

- They provide quick access to capital, often within a few days.

- They can be used for a variety of business purposes.

- They offer a lower interest rate than unsecured loans.

- They do not require the borrower to put up personal assets as collateral.

Unitranche loans also have some drawbacks, including:

- They require the borrower to have a good credit score.

- They can be more expensive than traditional bank loans.

- They may have prepayment penalties.

- They can be difficult to qualify for if the borrower does not have sufficient assets to secure the loan.