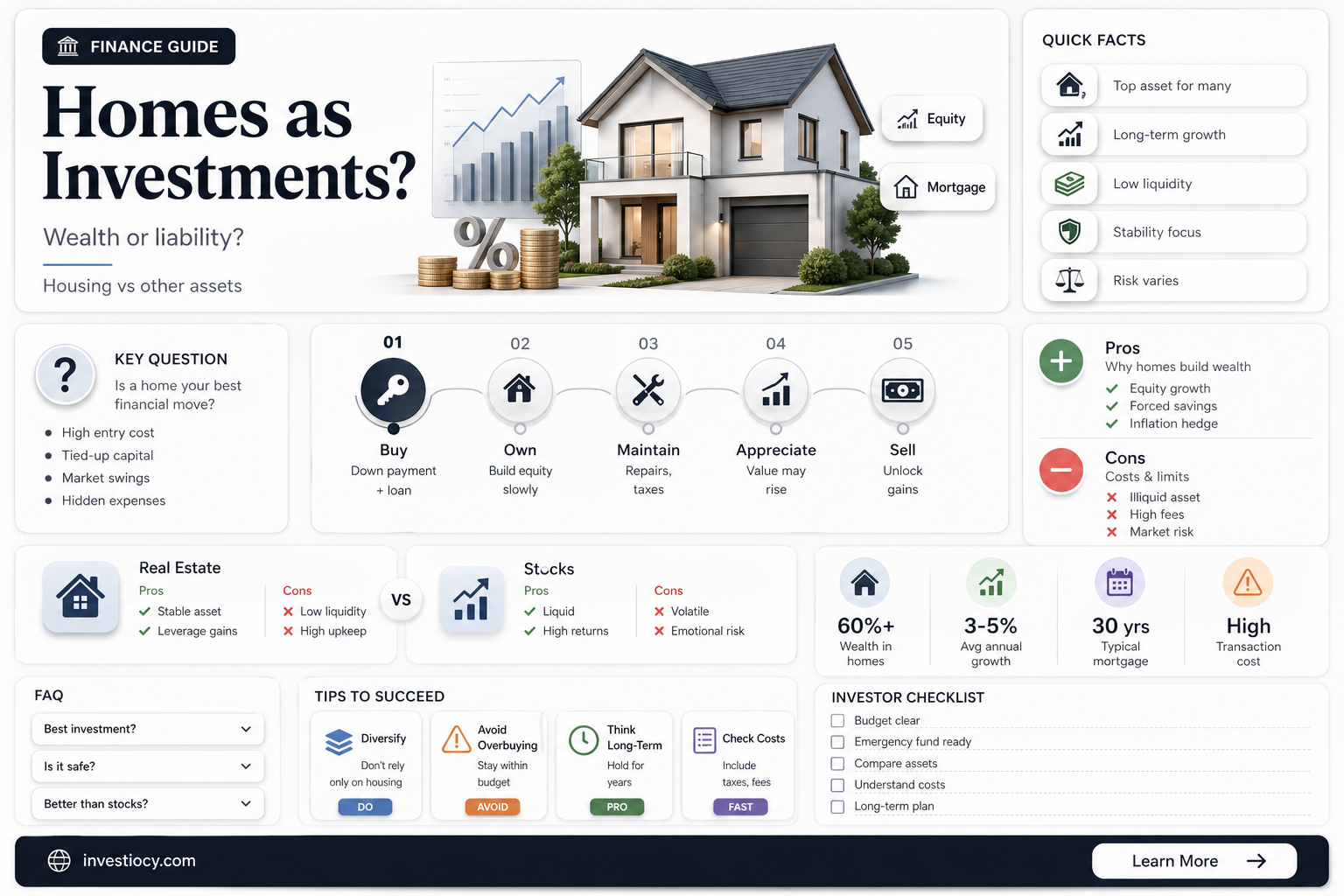

Homes are often considered one of the most significant investments people make in their lifetimes. This notion is rooted in the fact that purchasing a home typically involves a substantial financial commitment, often requiring years of saving and planning. Beyond the monetary aspect, homes also represent a long-term commitment to a particular location and lifestyle. They serve as a foundation for building personal wealth and stability, as well as providing a sense of security and belonging. However, the idea that homes are always the best investment is subject to debate, as various factors such as market conditions, personal financial goals, and lifestyle preferences can influence the wisdom of investing in real estate.

Explore related products

What You'll Learn

- Home Equity: Building wealth through property appreciation and mortgage payments

- Financial Security: Homeownership provides stability and a sense of financial security

- Personalization: Owning a home allows for customization and personal expression

- Tax Benefits: Homeowners may enjoy tax deductions on mortgage interest and property taxes

- Retirement Planning: Using home equity as a retirement fund or downsizing for financial flexibility

![]()

Home Equity: Building wealth through property appreciation and mortgage payments

Home equity is a powerful tool for building wealth, often overlooked by many homeowners. As you pay down your mortgage, you're not just reducing your debt; you're also increasing your equity in the property. This equity can be a significant asset, especially if property values in your area are appreciating. For instance, if you bought a home for $300,000 and have paid down $50,000 of your mortgage, and the property value has increased to $350,000, your equity would be $100,000. This increase in equity can be leveraged for various financial benefits, such as securing loans or lines of credit, which can be used for investments, home improvements, or other significant expenses.

One of the most effective strategies for building home equity is making extra mortgage payments. By paying more than the minimum required each month, you can significantly reduce the time it takes to pay off your mortgage and increase your equity faster. For example, if you have a $200,000 mortgage at a 4% interest rate with a 30-year term, paying an extra $100 per month could save you over $20,000 in interest and pay off your mortgage 7 years earlier. This not only frees up more of your income but also allows you to build equity more rapidly, which can be particularly beneficial in a rising real estate market.

Another way to build home equity is through home improvements and renovations. By investing in upgrades that increase your home's value, such as a new kitchen, bathroom, or energy-efficient systems, you can boost your equity without necessarily increasing your mortgage debt. It's important to choose improvements that are likely to appreciate in value and appeal to potential buyers if you decide to sell your home in the future. Consulting with a real estate professional or appraiser can help you determine which improvements will yield the best return on investment.

However, it's crucial to be mindful of the risks associated with using home equity. Tapping into your equity through loans or lines of credit can be tempting, but it's essential to use this financial resource responsibly. Borrowing against your home equity can put your property at risk if you're unable to repay the debt, and it can also reduce your financial flexibility in the future. It's advisable to consult with a financial advisor to discuss the potential risks and benefits of using home equity as part of your overall financial strategy.

In conclusion, home equity can be a valuable asset for building wealth, but it requires careful management and strategic planning. By making extra mortgage payments, investing in home improvements, and using equity responsibly, homeowners can harness the power of their property to achieve their financial goals. Remember, your home is not just a place to live; it's also a significant investment that can help you build a more secure financial future.

Smart Investments: Unveiling the Secrets of Wealthy Portfolios

You may want to see also

Explore related products

![]()

Financial Security: Homeownership provides stability and a sense of financial security

Homeownership is often viewed as a cornerstone of financial stability, providing individuals and families with a tangible asset that can appreciate over time. This perception of security stems from several key factors. Firstly, owning a home eliminates the need for monthly rent payments, which can be a significant financial burden. Instead, homeowners pay a mortgage, which, while still a substantial expense, offers the benefit of building equity. This equity can be leveraged in various ways, such as through home equity loans or lines of credit, providing homeowners with access to funds for emergencies, renovations, or other major expenses.

Moreover, homeownership can offer tax advantages, such as the ability to deduct mortgage interest and property taxes from taxable income. These deductions can result in significant savings, particularly in the early years of homeownership when mortgage interest payments are higher. Additionally, as property values increase, homeowners may benefit from capital gains, which can further enhance their financial security.

Another aspect of financial security tied to homeownership is the sense of stability it provides. Renters may face the uncertainty of lease renewals, rent increases, or the possibility of being asked to vacate the property. In contrast, homeowners have a permanent residence, which can be especially important for families with children or individuals who desire a long-term connection to their community.

Furthermore, homeownership can foster a sense of pride and accomplishment, which can have positive psychological effects. This emotional investment in one's home can lead to better maintenance and upkeep, potentially increasing the property's value over time. Additionally, owning a home can provide a sense of belonging and rootedness, which can contribute to overall well-being and life satisfaction.

In conclusion, homeownership offers numerous benefits that contribute to financial security, including the elimination of rent payments, the ability to build equity, tax advantages, and a sense of stability and pride. While purchasing a home is a significant financial decision, it can provide long-term benefits that enhance an individual's or family's overall financial well-being.

Unlocking Financial Freedom: The Power of Smart Investments

You may want to see also

Explore related products

![]()

Personalization: Owning a home allows for customization and personal expression

Owning a home is more than just a financial investment; it's a canvas for personal expression. The ability to customize one's living space is a significant advantage that comes with homeownership. This personalization can range from minor cosmetic changes to major renovations, all of which contribute to making a house feel like a home. For many, this freedom to modify and adapt their environment to their tastes and needs is a key part of the American dream.

One of the primary ways homeowners personalize their space is through interior design. This can include choosing paint colors, selecting furniture, and adding decorative elements that reflect their personality and style. For instance, a homeowner might opt for a minimalist aesthetic with neutral tones and clean lines, or they might prefer a more eclectic look with bold colors and a mix of patterns and textures. These choices not only make the space more visually appealing but also create an environment that is more comfortable and enjoyable to live in.

Exterior modifications are another popular way for homeowners to express their individuality. This can involve landscaping, adding outdoor living spaces, or making architectural changes to the house itself. For example, a homeowner might install a patio or deck to create an outdoor entertaining area, or they might plant a garden to bring a touch of nature to their property. These enhancements not only improve the curb appeal of the home but also increase its functionality and enjoyment.

Personalization can also extend to more practical aspects of the home, such as organization and storage solutions. Homeowners might install custom shelving or cabinetry to maximize storage space and keep their belongings organized. They might also invest in smart home technology to make their living space more convenient and efficient. For instance, installing a smart thermostat can help regulate the temperature and save on energy costs, while a home security system can provide peace of mind and added safety.

In conclusion, the ability to personalize a home is a significant benefit of ownership. It allows individuals to create a living space that is not only functional but also reflective of their personal style and preferences. Whether through interior design, exterior modifications, or practical upgrades, personalization can transform a house into a home that is uniquely suited to its inhabitants.

Diversifying Dreams: Exploring the Many Faces of Modern Investment

You may want to see also

Explore related products

![]()

Tax Benefits: Homeowners may enjoy tax deductions on mortgage interest and property taxes

Homeownership comes with various financial benefits, one of the most significant being tax deductions. These deductions can substantially reduce a homeowner's taxable income, leading to lower tax liabilities. Specifically, homeowners can deduct the interest paid on their mortgage and the property taxes they pay annually.

The mortgage interest deduction is particularly valuable in the early years of homeownership when the majority of mortgage payments go towards interest. This deduction can be claimed on both primary residences and second homes, although there are limits to the amount of interest that can be deducted. For instance, if a homeowner has a mortgage with an interest rate of 4% on a $300,000 loan, they could potentially deduct thousands of dollars in interest payments each year.

Property tax deductions are also a significant benefit. Property taxes are typically assessed based on the value of the property and can vary widely depending on the location. Homeowners can deduct the full amount of property taxes paid, which can be a substantial sum in areas with high property values. For example, in a region where the average property tax rate is 1.5%, a homeowner with a property valued at $500,000 could deduct $7,500 in property taxes annually.

To maximize these tax benefits, homeowners should ensure they are keeping accurate records of their mortgage interest and property tax payments. This includes maintaining copies of mortgage statements and property tax bills. Additionally, homeowners should be aware of any changes to tax laws that could impact these deductions, as tax policies can and do change over time.

In conclusion, the tax benefits associated with homeownership can provide significant financial savings. By understanding and leveraging these deductions, homeowners can reduce their tax burden and potentially increase their overall wealth over time.

Exploring the Psychology Behind Investment Decisions

You may want to see also

Explore related products

![]()

Retirement Planning: Using home equity as a retirement fund or downsizing for financial flexibility

As people approach retirement age, they often find themselves facing a significant financial challenge: how to maintain their standard of living without a regular paycheck. For many, their home represents their largest asset, and leveraging this equity can be a viable strategy for funding retirement. One option is to use a reverse mortgage, which allows homeowners to borrow against the value of their property without having to make monthly payments. This can provide a steady stream of income to supplement retirement savings.

Another strategy is to downsize to a smaller, more affordable home. This can free up cash from the sale of the larger property, which can then be used to fund retirement or invested for future growth. Downsizing can also reduce ongoing expenses such as property taxes, maintenance, and utilities, freeing up more money for other purposes.

However, it's important to carefully consider the implications of using home equity for retirement funding. Borrowing against the value of a home can reduce the amount of equity available for future needs, such as long-term care or unexpected expenses. Additionally, downsizing may not be feasible for everyone, particularly those with limited mobility or who have strong emotional attachments to their current home.

To make the most of using home equity for retirement planning, it's essential to consult with a financial advisor who can help assess the individual's unique situation and develop a personalized strategy. This may involve considering factors such as the current housing market, the homeowner's age and health, and their overall financial goals and needs.

In conclusion, using home equity as a retirement fund or downsizing for financial flexibility can be a valuable strategy for some individuals. However, it's important to carefully weigh the potential benefits and drawbacks and to seek professional advice to ensure that this approach aligns with one's overall financial goals and needs.

Is Robinhood Still Relevant? A Look at Its Current Status

You may want to see also

Frequently asked questions

Yes, for many individuals, purchasing a home is one of the largest financial investments they will make in their lifetime. It often involves a significant amount of money and can have long-term implications for one's financial stability and wealth accumulation.

A home is considered a valuable investment for several reasons. Firstly, real estate tends to appreciate in value over time, meaning that the home can be sold for a higher price than it was originally purchased. Additionally, a home provides a place to live, which can save on rental costs and provide a sense of security and stability. Finally, a home can also be used as a source of income through renting or selling.

Yes, there are several risks associated with investing in a home. One risk is that the value of the home may decrease over time, resulting in a loss of investment. Another risk is that the home may require significant maintenance and repairs, which can be costly. Finally, there is also the risk of being unable to sell the home quickly or at a desirable price, which can impact one's financial flexibility.

![Pacific Mailer Padfolio Portfolio Leather Binder, Interview Legal Document Organizer, Business Card Holder Included Letter Sized Writing Pad [Piano Noir Faux Leather Matte Finish]](https://m.media-amazon.com/images/I/71iIFjfC9dL._AC_UL320_.jpg)