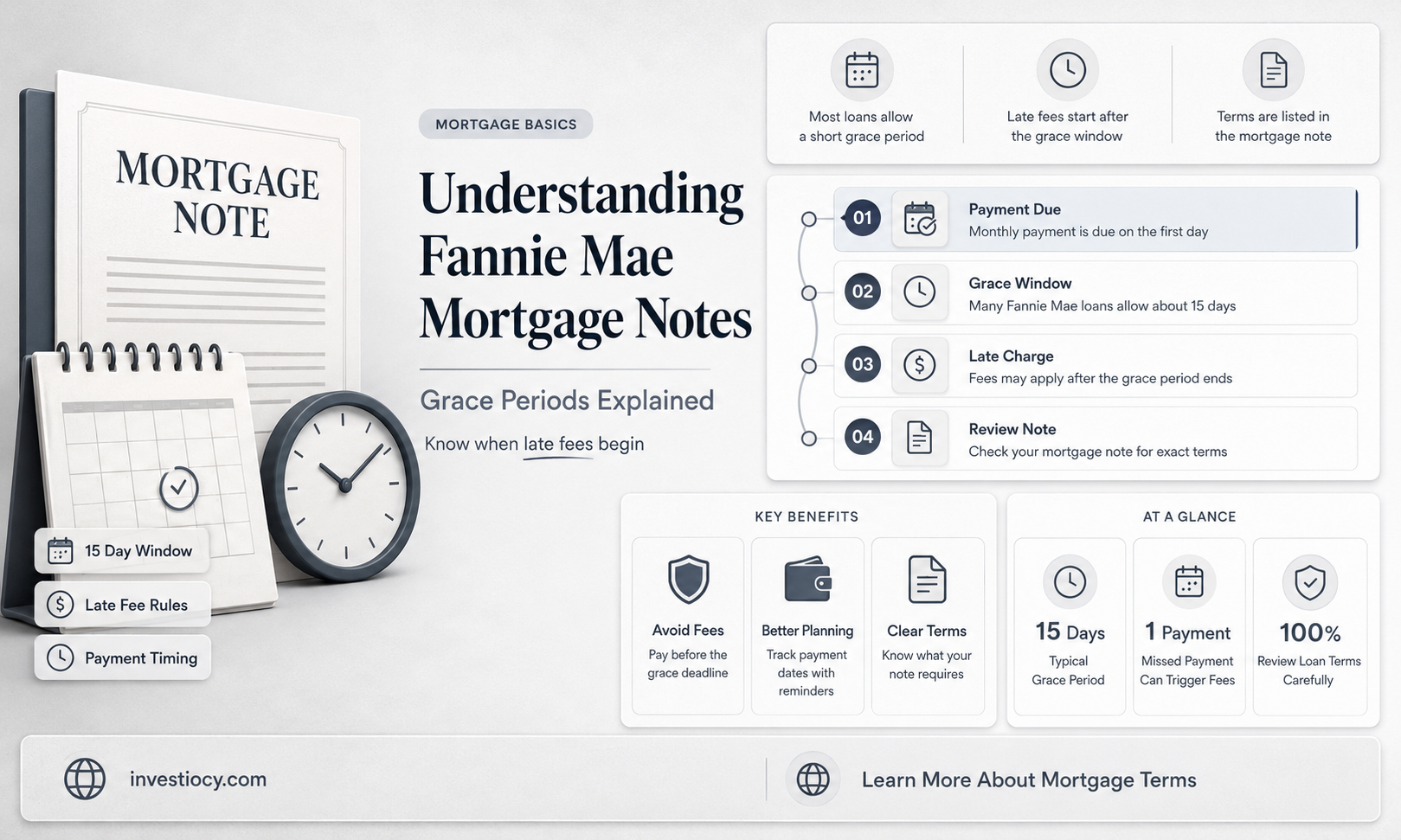

A Fannie Mae mortgage note typically includes a grace period, which is a specified timeframe during which a borrower can make their monthly mortgage payment without incurring a late fee. This grace period is designed to provide flexibility for borrowers who may need a few extra days to make their payment. Understanding the specifics of this grace period is crucial for homeowners to manage their finances effectively and avoid unnecessary penalties.

Explore related products

What You'll Learn

- Definition of a Fannie Mae mortgage note and its standard terms

- Typical grace period duration for Fannie Mae mortgages

- Consequences of missing payments within the grace period

- How the grace period affects credit scores and financial standing?

- Options available to borrowers if they cannot make payments within the grace period

![]()

Definition of a Fannie Mae mortgage note and its standard terms

A Fannie Mae mortgage note is a legal document that outlines the terms and conditions of a loan secured by real property. It is a standardized form used by Fannie Mae, a government-sponsored enterprise that purchases and securitizes mortgages to make them available to lenders. The note specifies the borrower's promise to repay the loan amount, plus interest, over a set period. Standard terms typically include the loan amount, interest rate, payment schedule, and penalties for late payments or prepayment.

One unique aspect of Fannie Mae mortgage notes is the inclusion of a grace period. This is a specified timeframe during which the borrower can make their monthly payment without incurring a late fee. The grace period is designed to provide flexibility for borrowers who may experience temporary financial difficulties. It is important to note that while the grace period allows for late payments without penalty, interest may still accrue on the unpaid balance.

The length of the grace period can vary depending on the specific loan program and lender. However, Fannie Mae typically allows for a grace period of up to 15 days. This means that if a borrower's payment is due on the 1st of the month, they have until the 16th to make the payment without incurring a late fee. Borrowers should always review their loan documents to confirm the exact terms of their grace period.

It is also important for borrowers to understand that the grace period does not affect their credit score. Late payments made within the grace period are not reported to credit bureaus as late. However, if a borrower consistently makes payments after the grace period has expired, it may negatively impact their credit score.

In conclusion, a Fannie Mae mortgage note is a standardized legal document that outlines the terms of a loan, including the grace period. The grace period provides borrowers with a temporary extension to make their monthly payments without incurring a late fee. While the grace period can be a helpful feature, it is essential for borrowers to understand its terms and limitations to avoid potential negative consequences.

Understanding Deeds and Mortgages: What Does a Deed Show?

You may want to see also

Explore related products

![]()

Typical grace period duration for Fannie Mae mortgages

Fannie Mae mortgages typically include a grace period, which is a specified timeframe during which borrowers can make their monthly payments without incurring late fees or penalties. This grace period is designed to provide flexibility for borrowers who may experience temporary financial difficulties or delays in payment processing.

The duration of the grace period for Fannie Mae mortgages can vary depending on the specific loan program and servicer policies. However, it is common for Fannie Mae loans to have a grace period of up to 15 days. This means that borrowers generally have until the 15th day of the month to make their payment without facing any late charges.

It's important to note that while the grace period provides some leeway, it does not excuse borrowers from making their payments. Borrowers should always aim to make their payments on time to avoid any potential negative impacts on their credit score or loan standing. Additionally, servicers may have different policies regarding grace periods, so it's essential for borrowers to review their loan documents and contact their servicer if they have any questions or concerns.

In some cases, borrowers may be able to request an extension of the grace period if they are experiencing severe financial hardship. This would typically require documentation of the hardship and approval from the servicer. However, such extensions are not guaranteed and should not be relied upon as a regular means of avoiding timely payments.

Overall, the grace period on Fannie Mae mortgages serves as a helpful tool for borrowers to manage their payments and avoid unnecessary fees. By understanding the typical duration and policies surrounding the grace period, borrowers can better plan their finances and ensure they remain in good standing with their mortgage obligations.

Understanding Cosigner Rights in a Mortgage Agreement

You may want to see also

Explore related products

![]()

Consequences of missing payments within the grace period

Missing payments within the grace period of a Fannie Mae mortgage note can have several serious consequences. One of the most immediate impacts is the accumulation of late fees, which can add up quickly and increase the overall cost of the mortgage. Additionally, consistent late payments can lead to a negative impact on the borrower's credit score, making it more difficult to secure future loans or credit at favorable rates.

Beyond the financial penalties, missing payments within the grace period can also jeopardize the borrower's relationship with the lender. This can result in a loss of trust and potentially lead to more stringent terms or conditions on future loans. Furthermore, if the borrower continues to miss payments, they may eventually face foreclosure, which can have long-lasting consequences on their financial stability and ability to secure housing in the future.

It's important for borrowers to understand the terms of their mortgage note, including the grace period and the consequences of missing payments. By staying informed and making timely payments, borrowers can avoid these negative outcomes and maintain a positive relationship with their lender.

Securing Your Dream Home: Does a Down Payment Guarantee a Mortgage?

You may want to see also

Explore related products

![]()

How the grace period affects credit scores and financial standing

A grace period on a mortgage note, such as one from Fannie Mae, can have significant implications for a borrower's credit score and overall financial standing. During this period, borrowers are typically allowed to make payments within a certain timeframe without incurring late fees or penalties. However, it's crucial to understand that this grace period does not mean payments can be skipped altogether.

One of the primary ways a grace period affects credit scores is by providing a buffer against late payments. Late payments can have a detrimental impact on credit scores, often resulting in a drop of several points. By allowing borrowers some flexibility in their payment schedule, a grace period can help prevent these negative marks on their credit report. This, in turn, can help maintain or even improve their credit score over time.

From a financial standing perspective, a grace period can offer temporary relief to borrowers who may be experiencing cash flow issues. This can be particularly beneficial for those who are facing unexpected expenses or financial emergencies. By avoiding late fees and penalties during this period, borrowers can allocate their funds more effectively, potentially preventing further financial strain.

However, it's important to note that relying too heavily on a grace period can lead to poor financial habits. Borrowers should always aim to make their mortgage payments on time and in full, using the grace period only when absolutely necessary. Additionally, borrowers should be aware that interest may still accrue during the grace period, so it's essential to understand the terms and conditions of their mortgage note.

In conclusion, a grace period on a Fannie Mae mortgage note can provide valuable benefits to borrowers, including protection for their credit score and temporary financial relief. However, it's crucial to use this period responsibly and maintain good financial habits to ensure long-term financial stability.

Navigating Divorce and Mortgages: Understanding the Legal Override

You may want to see also

Explore related products

![]()

Options available to borrowers if they cannot make payments within the grace period

If a borrower finds themselves unable to make payments within the grace period of a Fannie Mae mortgage note, several options are available to help mitigate potential financial distress. One such option is to reach out to the lender or loan servicer to discuss possible repayment plans or loan modifications. These arrangements can sometimes include extending the repayment period, reducing the interest rate, or even temporarily suspending payments. It's crucial for borrowers to communicate proactively with their lenders to explore these possibilities before the grace period expires.

Another avenue for borrowers is to seek assistance from housing counseling agencies approved by the U.S. Department of Housing and Urban Development (HUD). These agencies provide free or low-cost counseling services and can help borrowers understand their options, develop a budget, and negotiate with lenders. They may also be able to provide information on government programs or non-profit organizations that offer financial assistance or other forms of support to struggling homeowners.

In some cases, borrowers may be able to refinance their mortgage to a more manageable loan with different terms. This could involve switching from an adjustable-rate mortgage to a fixed-rate mortgage or extending the loan term to reduce monthly payments. However, refinancing may come with additional costs and fees, so borrowers should carefully weigh the benefits against the expenses before proceeding.

For borrowers who are facing severe financial hardship, a short sale or deed-in-lieu of foreclosure may be viable options. A short sale involves selling the property for less than the outstanding mortgage balance, with the lender agreeing to accept the proceeds as full payment. A deed-in-lieu of foreclosure, on the other hand, involves transferring the property's deed to the lender, effectively giving up ownership in exchange for the lender agreeing not to pursue foreclosure. Both options can help borrowers avoid the negative consequences of foreclosure, but they may also have tax implications and should be thoroughly explored with the guidance of a qualified professional.

Lastly, borrowers should be aware of potential scams targeting those who are struggling to make mortgage payments. Some unscrupulous companies may offer false promises of loan modifications or other forms of assistance in exchange for upfront fees. Borrowers should always verify the legitimacy of any organization offering help and should never provide personal or financial information to unsolicited parties. By being vigilant and proactive, borrowers can protect themselves from these fraudulent schemes and find genuine assistance in navigating their financial challenges.

Boosting Your Mortgage Approval Odds: The Power of a Cosigner

You may want to see also

Frequently asked questions

Yes, Fannie Mae mortgage notes typically include a grace period. This period allows borrowers a certain amount of time after the due date to make their mortgage payment without incurring late fees or penalties.

The grace period for a Fannie Mae mortgage is usually 15 days. This means that if your mortgage payment is due on the 1st of the month, you generally have until the 16th to make the payment without facing any late charges.

If you make your Fannie Mae mortgage payment after the grace period, you may be subject to late fees or penalties. These charges can vary depending on the specific terms of your mortgage note and the lender's policies. It's important to make your payments on time to avoid these additional costs and to maintain a good credit standing.